A behavioral economics perspective on tobacco taxation

- PMID: 20220113

- PMCID: PMC2836334

- DOI: 10.2105/AJPH.2009.160838

A behavioral economics perspective on tobacco taxation

Abstract

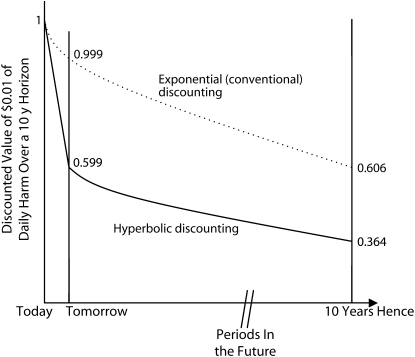

Economic studies of taxation typically estimate external costs of tobacco use to be low and refrain from recommending large tobacco taxes. Behavioral economics suggests that a rational decision-making process by individuals fully aware of tobacco's hazards might still lead to overconsumption through the psychological tendency to favor immediate gratification over future harm. Taxes can serve as a self-control device to help reduce tobacco use and enable successful quit attempts. Whether taxes are appropriately high depends on how excessively people underrate the harm from tobacco use and varies with a country's circumstances. Such taxes are likely to be more equitable for poorer subgroups than traditional economic analysis suggests, which would strengthen the case for increased tobacco taxation globally.

Figures

References

-

- WHO Report on the Global Tobacco Epidemic, 2008: The MPOWER Package Geneva, Switzerland: World Health Organization; 2008

-

- How to save a billion lives. Economist February 7, 2008:67

-

- Sunley EM, Yurekli A, Chaloupka FJ. The design, administration, and potential revenue of tobacco excises. : Jha P, Chaloupka FJ, Tobacco Control in Developing Countries Oxford, UK: Oxford University Press; 2000:409–426

-

- Mullainathan S, Thaler RH. Behavioral economics. : Smelser NJ, Baltes PB, International Encyclopedia of the Social and Behavioral Sciences New York, NY: Pergamon Press; 2001:1094–1100

Publication types

MeSH terms

LinkOut - more resources

Full Text Sources

Medical