Price regulation, new entry, and information shock on pharmaceutical market in Taiwan: a nationwide data-based study from 2001 to 2004

- PMID: 20653979

- PMCID: PMC2918598

- DOI: 10.1186/1472-6963-10-218

Price regulation, new entry, and information shock on pharmaceutical market in Taiwan: a nationwide data-based study from 2001 to 2004

Abstract

Background: Using non-steroidal anti-inflammatory drugs (NSAIDs) as a case, we used Taiwan's National Health Insurance (NHI) database, to empirically explore the association between policy interventions (price regulation, new drug entry, and an information shock) and drug expenditures, utilization, and market structure between 2001 and 2004.

Methods: All NSAIDs prescribed in ambulatory visits in the NHI system during our study period were included and aggregated quarterly. Segmented regression analysis for interrupted time series was used to examine the associations between two price regulations, two new drug entries (cyclooxygennase-2 inhibitors) and the rofecoxib safety signal and expenditures and utilization of all NSAIDs. Herfindahl index (HHI) was applied to further examine the association between these interventions and market structure of NSAIDs.

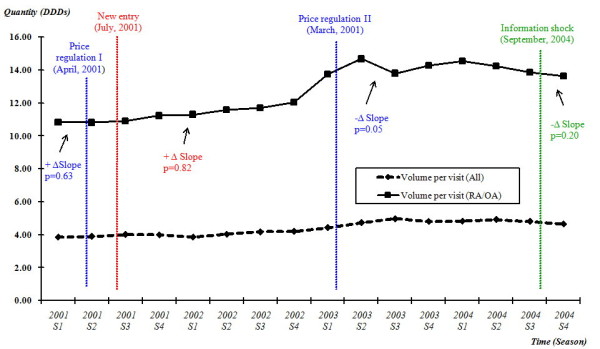

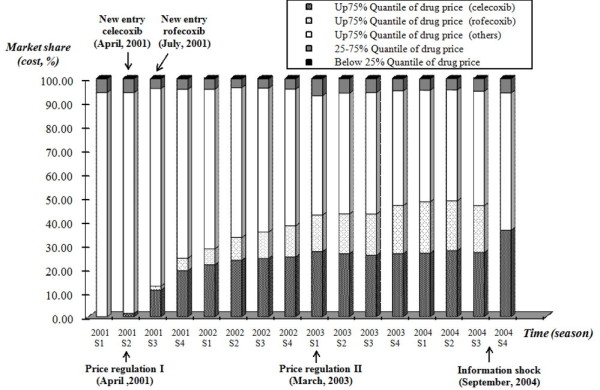

Results: New entry was the only variable that was significantly correlated with changes of expenditures (positive change, p = 0.02) and market structure of the NSAIDs market in the NHI system. The correlation between price regulation (first price regulation, p = 0.62; second price regulation, p = 0.26) and information shock (p = 0.31) and drug expenditure were not statistically significant. There was no significant change in the prescribing volume of NSAIDs per rheumatoid arthritis (RA) or osteoarthritis (OA) ambulatory visit during the observational period. The market share of NSAIDs had also been largely substituted by these new drugs up to 50%, in a three-year period and resulted in a more concentrated market structure (HHI 0.17).

Conclusions: Our empirical study found that new drug entry was the main driving force behind escalating drug spending, especially by altering the market share.

Figures

References

-

- OECD. Health at a Glance: OECD Indicators 2005. OECD; 2005.

Publication types

MeSH terms

Substances

LinkOut - more resources

Full Text Sources