Dominating clasp of the financial sector revealed by partial correlation analysis of the stock market

- PMID: 21188140

- PMCID: PMC3004792

- DOI: 10.1371/journal.pone.0015032

Dominating clasp of the financial sector revealed by partial correlation analysis of the stock market

Abstract

What are the dominant stocks which drive the correlations present among stocks traded in a stock market? Can a correlation analysis provide an answer to this question? In the past, correlation based networks have been proposed as a tool to uncover the underlying backbone of the market. Correlation based networks represent the stocks and their relationships, which are then investigated using different network theory methodologies. Here we introduce a new concept to tackle the above question--the partial correlation network. Partial correlation is a measure of how the correlation between two variables, e.g., stock returns, is affected by a third variable. By using it we define a proxy of stock influence, which is then used to construct partial correlation networks. The empirical part of this study is performed on a specific financial system, namely the set of 300 highly capitalized stocks traded at the New York Stock Exchange, in the time period 2001-2003. By constructing the partial correlation network, unlike the case of standard correlation based networks, we find that stocks belonging to the financial sector and, in particular, to the investment services sub-sector, are the most influential stocks affecting the correlation profile of the system. Using a moving window analysis, we find that the strong influence of the financial stocks is conserved across time for the investigated trading period. Our findings shed a new light on the underlying mechanisms and driving forces controlling the correlation profile observed in a financial market.

Conflict of interest statement

Figures

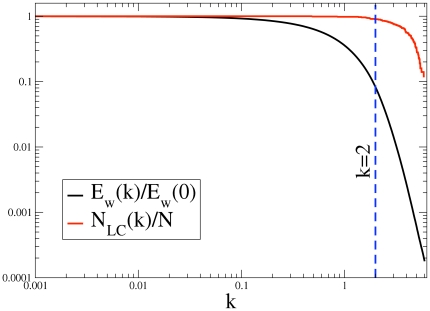

is the one used in the paper.

is the one used in the paper.

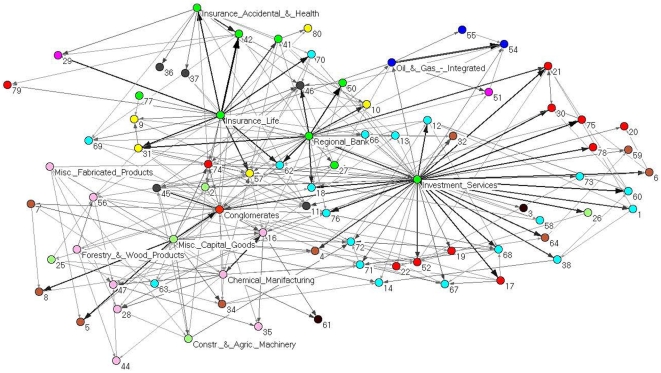

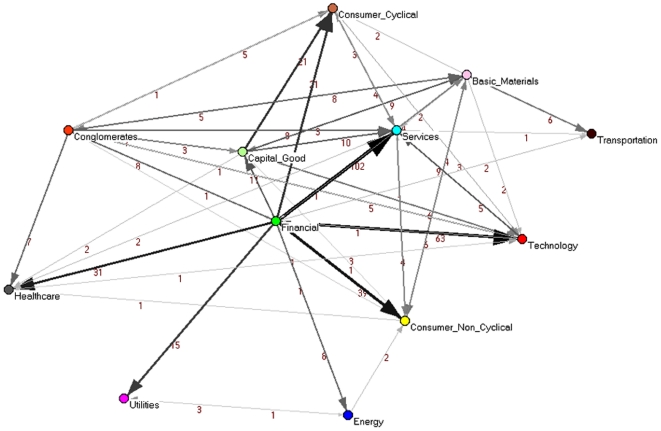

according to Eq.(5) are labeled in the figure. Sub-sectors labeled with numbers are listed in Table S2. We find two main hubs in the network - the investment services and the insurance life sub-sectors. The thickness and gray level of links is proportional to the logarithm of the weight of the link.

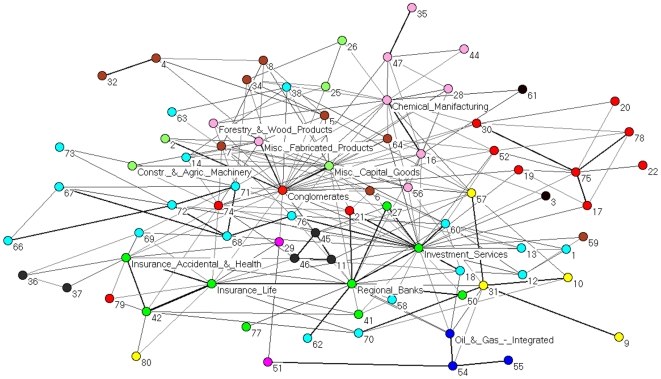

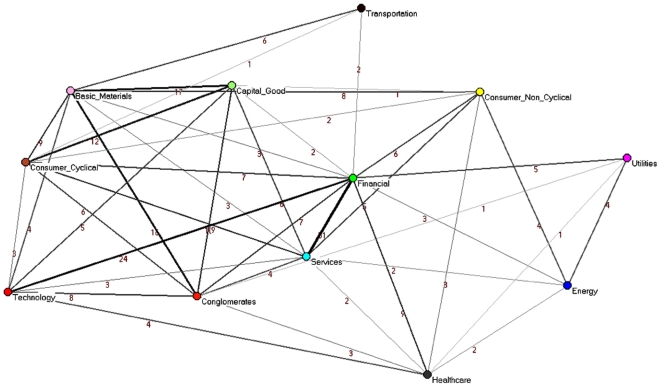

according to Eq.(5) are labeled in the figure. Sub-sectors labeled with numbers are listed in Table S2. We find two main hubs in the network - the investment services and the insurance life sub-sectors. The thickness and gray level of links is proportional to the logarithm of the weight of the link.

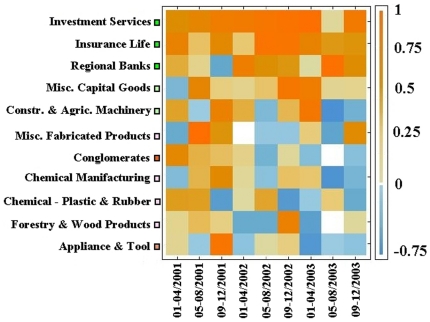

of each economic sub-sector. Here we present the results about

of each economic sub-sector. Here we present the results about  just for the 11 sub-sectors of activity that show a positive relative influence in at least one time window.

just for the 11 sub-sectors of activity that show a positive relative influence in at least one time window.References

-

- Schweitzer F, Fagiolo G, Sornette D, Vega-Redondo F, Vespignani A, et al. Economic Networks: The New Challenges. Science. 2009;325(5939):422. - PubMed

-

- Laloux L, Cizeau P, Bouchaud J-P, Potters M. Noise Dressing of Financial Correlation Matrices. Phys Rev Lett. 1999;83:1467–1470.

-

- Plerou V, Gopikrishnan P, Rosenow B, Amaral LAN, Stanley HE. Universal and Nonuniversal Properties of Cross Correlations in Financial Time Series. Phys Rev Lett. 1999;83:1471–1474.

-

- Mantegna RN. Hierarchical structure in financial markets. Eur Phys J B. 1999;11(1):193–197.

-

- Mantegna RN, Stanley HE. An Introduction to Econophysics: Correlation and Complexity in Finance. Cambridge, UK: Cambridge University Press; 2000.

Publication types

MeSH terms

LinkOut - more resources

Full Text Sources

Miscellaneous