The distribution of cigarette prices under different tax structures: findings from the International Tobacco Control Policy Evaluation (ITC) Project

- PMID: 23792324

- PMCID: PMC4009360

- DOI: 10.1136/tobaccocontrol-2013-050966

The distribution of cigarette prices under different tax structures: findings from the International Tobacco Control Policy Evaluation (ITC) Project

Abstract

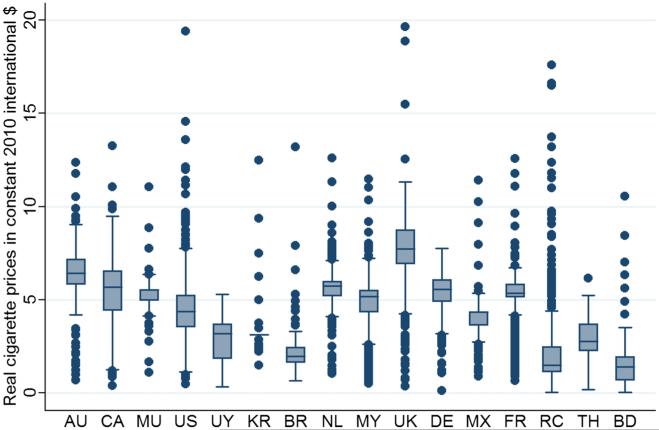

Background: The distribution of cigarette prices has rarely been studied and compared under different tax structures. Descriptive evidence on price distributions by countries can shed light on opportunities for tax avoidance and brand switching under different tobacco tax structures, which could impact the effectiveness of increased taxation in reducing smoking.

Objective: This paper aims to describe the distribution of cigarette prices by countries and to compare these distributions based on the tobacco tax structure in these countries.

Methods: We employed data for 16 countries taken from the International Tobacco Control Policy Evaluation Project to construct survey-derived cigarette prices for each country. Self-reported prices were weighted by cigarette consumption and described using a comprehensive set of statistics. We then compared these statistics for cigarette prices under different tax structures. In particular, countries of similar income levels and countries that impose similar total excise taxes using different tax structures were paired and compared in mean and variance using a two-sample comparison test.

Findings: Our investigation illustrates that, compared with specific uniform taxation, other tax structures, such as ad valorem uniform taxation, mixed (a tax system using ad valorem and specific taxes) uniform taxation, and tiered tax structures of specific, ad valorem and mixed taxation tend to have price distributions with greater variability. Countries that rely heavily on ad valorem and tiered taxes also tend to have greater price variability around the median. Among mixed taxation systems, countries that rely more heavily on the ad valorem component tend to have greater price variability than countries that rely more heavily on the specific component. In countries with tiered tax systems, cigarette prices are skewed more towards lower prices than are prices under uniform tax systems. The analyses presented here demonstrate that more opportunities exist for tax avoidance and brand switching when the tax structure departs from a uniform specific tax.

Keywords: Economics; Price; Taxation.

Figures

Similar articles

-

The association between tax structure and cigarette price variability: findings from the ITC Project.Tob Control. 2015 Jul;24 Suppl 3(0 3):iii88-iii93. doi: 10.1136/tobaccocontrol-2014-051771. Epub 2015 Apr 8. Tob Control. 2015. PMID: 25855641 Free PMC article.

-

Cigarette excise tax structure and cigarette prices in nine sub-Saharan African countries: evidence from the Global Adult Tobacco Survey.Tob Control. 2024 Feb 20;33(2):208-214. doi: 10.1136/tc-2022-057414. Tob Control. 2024. PMID: 38378207 Free PMC article.

-

Income and cigarette price responsiveness: evidence from Vietnam.Tob Control. 2022 Sep;31(Suppl 2):s152-s157. doi: 10.1136/tc-2022-057584. Epub 2022 Aug 17. Tob Control. 2022. PMID: 35977821

-

Understanding tobacco industry pricing strategy and whether it undermines tobacco tax policy: the example of the UK cigarette market.Addiction. 2013 Jul;108(7):1317-26. doi: 10.1111/add.12159. Epub 2013 Apr 16. Addiction. 2013. PMID: 23445255 Free PMC article. Review.

-

Impact of tobacco tax increases and industry pricing on smoking behaviours and inequalities: a mixed-methods study.Southampton (UK): NIHR Journals Library; 2020 Apr. Southampton (UK): NIHR Journals Library; 2020 Apr. PMID: 32271515 Free Books & Documents. Review.

Cited by

-

The association between tax structure and cigarette price variability: findings from the ITC Project.Tob Control. 2015 Jul;24 Suppl 3(0 3):iii88-iii93. doi: 10.1136/tobaccocontrol-2014-051771. Epub 2015 Apr 8. Tob Control. 2015. PMID: 25855641 Free PMC article.

-

Price, tax and tobacco product substitution in Zambia: findings from the ITC Zambia Surveys.Tob Control. 2019 May;28(Suppl 1):s45-s52. doi: 10.1136/tobaccocontrol-2017-054037. Epub 2018 Mar 24. Tob Control. 2019. PMID: 29574449 Free PMC article.

-

The use of legal, illegal and roll-your-own cigarettes to increasing tobacco excise taxes and comprehensive tobacco control policies: findings from the ITC Uruguay Survey.Tob Control. 2015 Jul;24 Suppl 3(0 3):iii17-iii24. doi: 10.1136/tobaccocontrol-2014-051890. Epub 2015 Mar 4. Tob Control. 2015. PMID: 25740084 Free PMC article.

-

Tobacco taxation, illegal cigarette supply and geography: findings from the ITC Uruguay Surveys.Tob Control. 2019 May;28(Suppl 1):s53-s60. doi: 10.1136/tobaccocontrol-2017-054218. Epub 2018 Oct 5. Tob Control. 2019. PMID: 30291202 Free PMC article.

-

Do Budget Cigarettes Emit More Particles? An Aerosol Spectrometric Comparison of Particulate Matter Concentrations between Private-Label Cigarettes and More Expensive Brand-Name Cigarettes.Int J Environ Res Public Health. 2022 May 13;19(10):5920. doi: 10.3390/ijerph19105920. Int J Environ Res Public Health. 2022. PMID: 35627457 Free PMC article.

References

-

- IARC . Handbooks of cancer prevention in tobacco control. Vol. 14. International Agency for Research on Cancer; 2011.

-

- WHO . WHO technical manual on tobacco tax administration. WHO; 2010.

-

- Cnossen S. Tobacco taxation in the European Union. 2006. CESifo working paper, No. 1718.

-

- WHO . Increasing tobacco taxation revenue in Egypt. WHO; 2010.

-

- Lance PM, Akin JS, Dow WH, et al. Is cigarette smoking in poorer nations highly sensitive to price? Evidence from Russia and China. J Health Econ. 2004;23:173–89. - PubMed

Publication types

MeSH terms

Grants and funding

LinkOut - more resources

Full Text Sources

Other Literature Sources