Quantifying the relationship between financial news and the stock market

- PMID: 24356666

- PMCID: PMC3868958

- DOI: 10.1038/srep03578

Quantifying the relationship between financial news and the stock market

Abstract

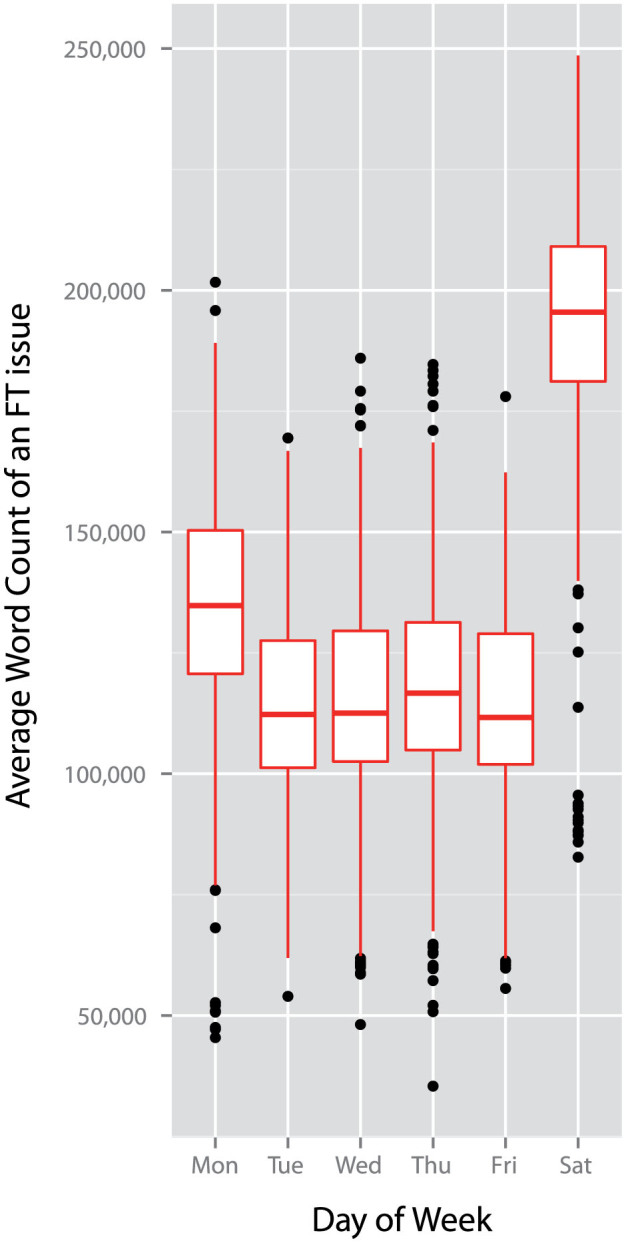

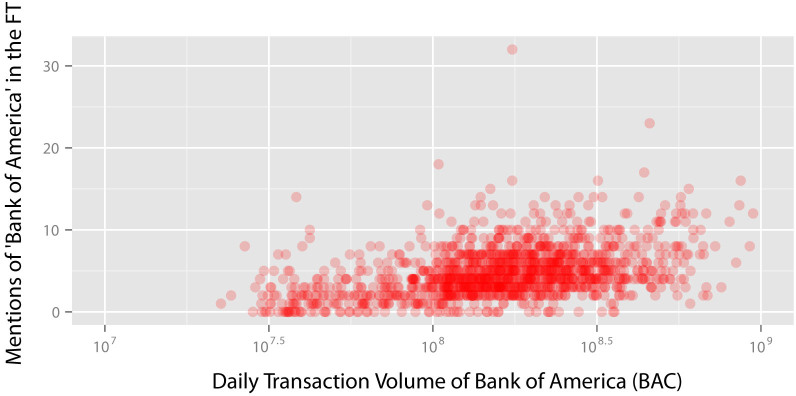

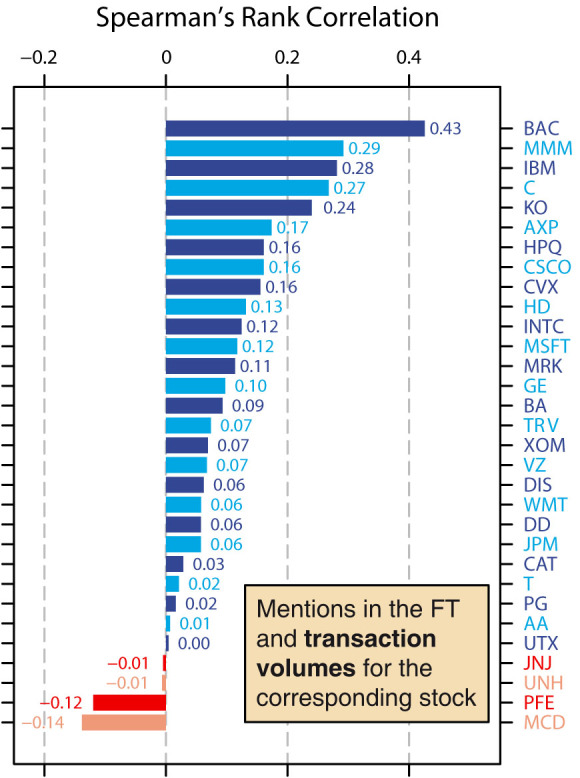

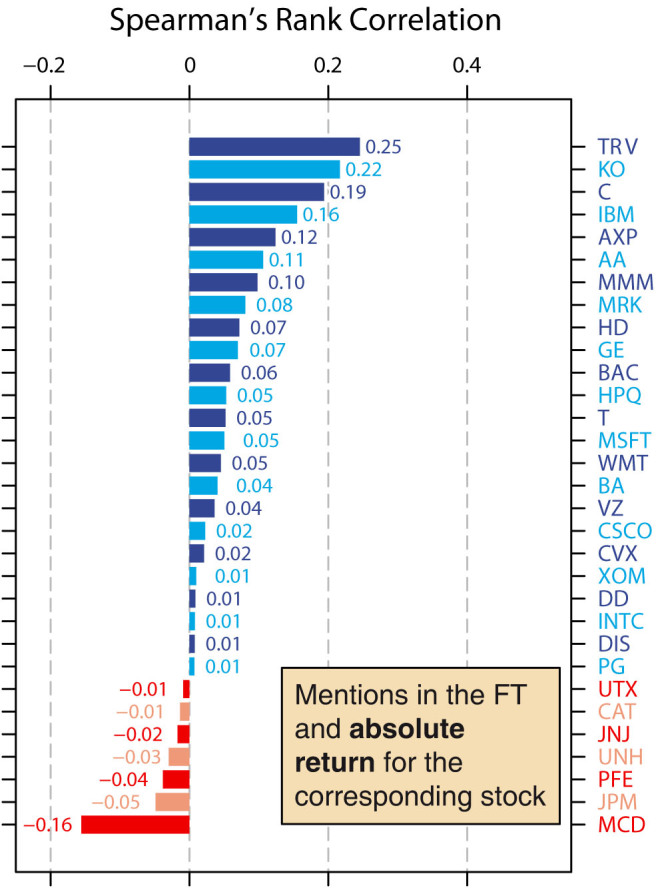

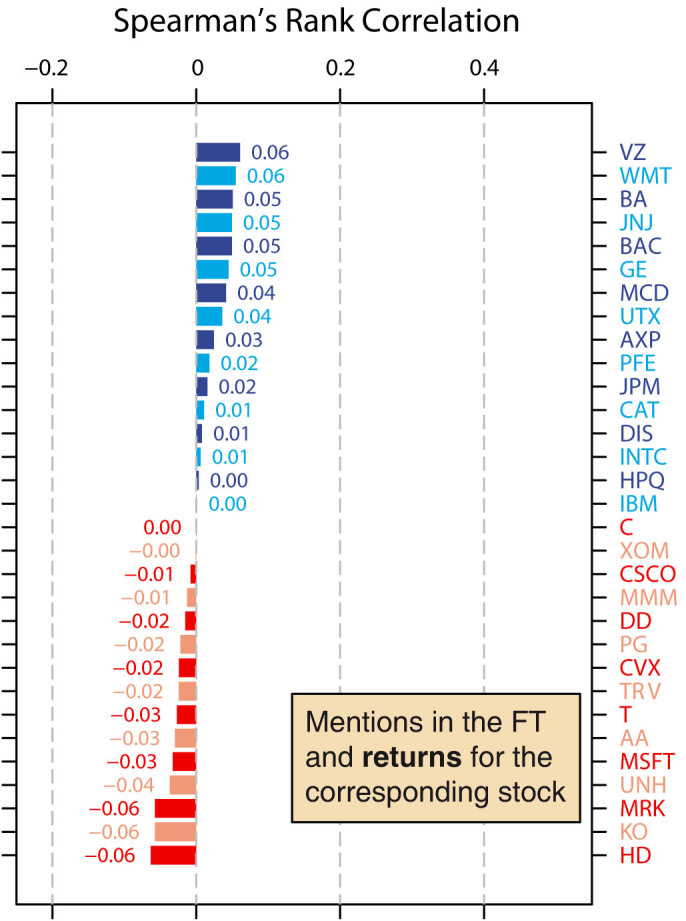

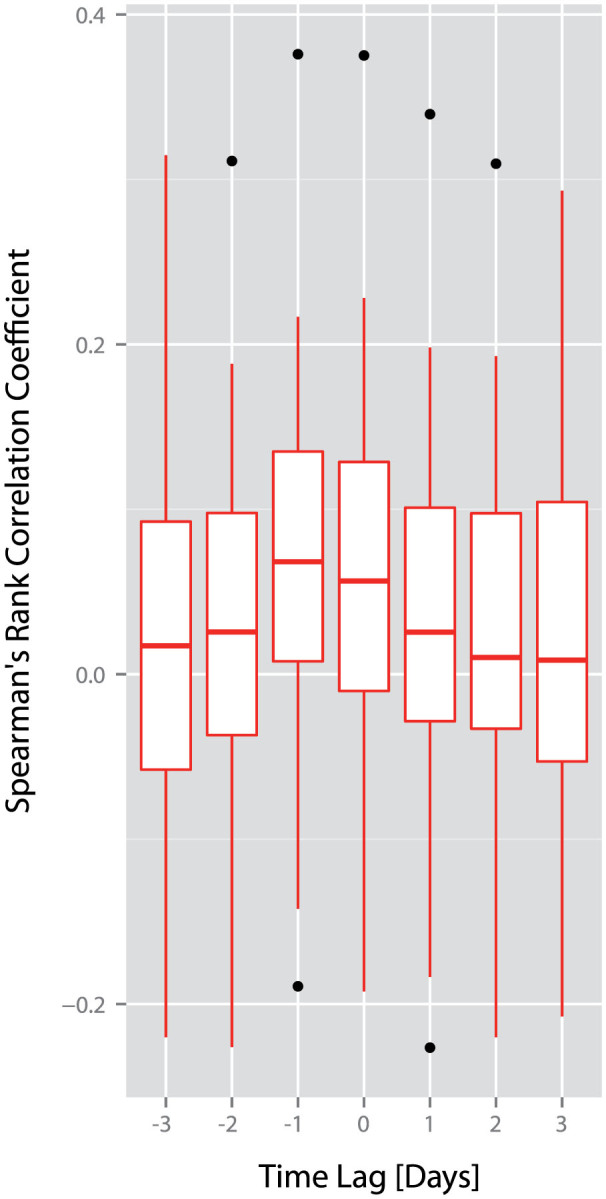

The complex behavior of financial markets emerges from decisions made by many traders. Here, we exploit a large corpus of daily print issues of the Financial Times from 2(nd) January 2007 until 31(st) December 2012 to quantify the relationship between decisions taken in financial markets and developments in financial news. We find a positive correlation between the daily number of mentions of a company in the Financial Times and the daily transaction volume of a company's stock both on the day before the news is released, and on the same day as the news is released. Our results provide quantitative support for the suggestion that movements in financial markets and movements in financial news are intrinsically interlinked.

Figures

References

Publication types

LinkOut - more resources

Full Text Sources

Other Literature Sources