Minimum pricing of alcohol versus volumetric taxation: which policy will reduce heavy consumption without adversely affecting light and moderate consumers?

- PMID: 24465368

- PMCID: PMC3898955

- DOI: 10.1371/journal.pone.0080936

Minimum pricing of alcohol versus volumetric taxation: which policy will reduce heavy consumption without adversely affecting light and moderate consumers?

Abstract

Background: We estimate the effect on light, moderate and heavy consumers of alcohol from implementing a minimum unit price for alcohol (MUP) compared with a uniform volumetric tax.

Methods: We analyse scanner data from a panel survey of demographically representative households (n = 885) collected over a one-year period (24 Jan 2010-22 Jan 2011) in the state of Victoria, Australia, which includes detailed records of each household's off-trade alcohol purchasing.

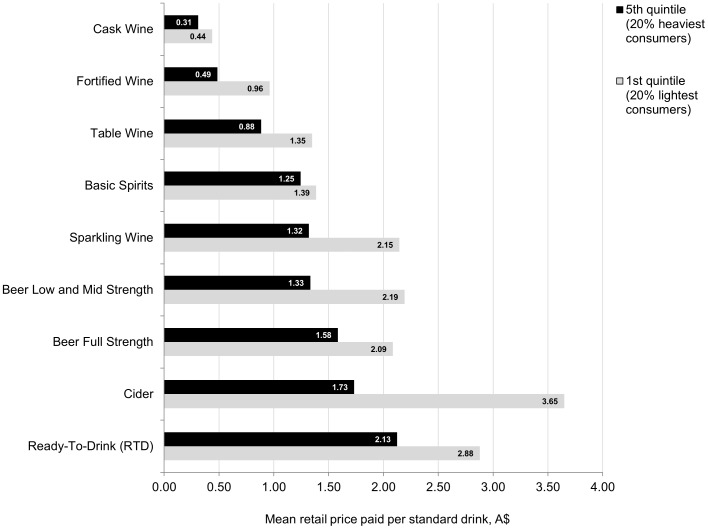

Findings: The heaviest consumers (3% of the sample) currently purchase 20% of the total litres of alcohol (LALs), are more likely to purchase cask wine and full strength beer, and pay significantly less on average per standard drink compared to the lightest consumers (A$1.31 [95% CI 1.20-1.41] compared to $2.21 [95% CI 2.10-2.31]). Applying a MUP of A$1 per standard drink has a greater effect on reducing the mean annual volume of alcohol purchased by the heaviest consumers of wine (15.78 LALs [95% CI 14.86-16.69]) and beer (1.85 LALs [95% CI 1.64-2.05]) compared to a uniform volumetric tax (9.56 LALs [95% CI 9.10-10.01] and 0.49 LALs [95% CI 0.46-0.41], respectively). A MUP results in smaller increases in the annual cost for the heaviest consumers of wine ($393.60 [95% CI 374.19-413.00]) and beer ($108.26 [95% CI 94.76-121.75]), compared to a uniform volumetric tax ($552.46 [95% CI 530.55-574.36] and $163.92 [95% CI 152.79-175.03], respectively). Both a MUP and uniform volumetric tax have little effect on changing the annual cost of wine and beer for light and moderate consumers, and likewise little effect upon their purchasing.

Conclusions: While both a MUP and a uniform volumetric tax have potential to reduce heavy consumption of wine and beer without adversely affecting light and moderate consumers, a MUP offers the potential to achieve greater reductions in heavy consumption at a lower overall annual cost to consumers.

Conflict of interest statement

Figures

Similar articles

-

Are Alcohol Taxation and Pricing Policies Regressive? Product-Level Effects of a Specific Tax and a Minimum Unit Price for Alcohol.Alcohol Alcohol. 2016 Jul;51(4):493-502. doi: 10.1093/alcalc/agv133. Epub 2015 Dec 30. Alcohol Alcohol. 2016. PMID: 26719379

-

Estimated Effects of Different Alcohol Taxation and Price Policies on Health Inequalities: A Mathematical Modelling Study.PLoS Med. 2016 Feb 23;13(2):e1001963. doi: 10.1371/journal.pmed.1001963. eCollection 2016 Feb. PLoS Med. 2016. PMID: 26905063 Free PMC article.

-

Cost-effectiveness of volumetric alcohol taxation in Australia.Med J Aust. 2010 Apr 19;192(8):439-43. doi: 10.5694/j.1326-5377.2010.tb03581.x. Med J Aust. 2010. PMID: 20402606

-

Potential effects of minimum unit pricing at local authority level on alcohol-attributed harms in North West and North East England: a modelling study.Southampton (UK): NIHR Journals Library; 2021 Mar. Southampton (UK): NIHR Journals Library; 2021 Mar. PMID: 33764725 Free Books & Documents. Review.

-

Pricing as a means of controlling alcohol consumption.Br Med Bull. 2017 Sep 1;123(1):149-158. doi: 10.1093/bmb/ldx020. Br Med Bull. 2017. PMID: 28910991 Review.

Cited by

-

Commentary on Kersbergen et al.: Same Price, same choices? Proportional pricing and the heaviest drinkers.Addiction. 2025 May;120(5):871-872. doi: 10.1111/add.70046. Epub 2025 Mar 25. Addiction. 2025. PMID: 40134213 Free PMC article. No abstract available.

-

Trends in alcohol-related injury admissions in adolescents in Western Australia and England: population-based cohort study.BMJ Open. 2017 May 29;7(5):e014913. doi: 10.1136/bmjopen-2016-014913. BMJ Open. 2017. PMID: 28554923 Free PMC article.

-

The effects of alcohol pricing policies on consumption, health, social and economic outcomes, and health inequality in Australia: a protocol of an epidemiological modelling study.BMJ Open. 2019 Jun 6;9(6):e029918. doi: 10.1136/bmjopen-2019-029918. BMJ Open. 2019. PMID: 31175201 Free PMC article.

-

Starmerella bombicola and Saccharomyces cerevisiae in Wine Sequential Fermentation in Aeration Condition: Evaluation of Ethanol Reduction and Analytical Profile.Foods. 2021 May 11;10(5):1047. doi: 10.3390/foods10051047. Foods. 2021. PMID: 34064665 Free PMC article.

-

A New Approach to the Reduction of Alcohol Content in Red Wines: The Use of High-Power Ultrasounds.Foods. 2020 Jun 2;9(6):726. doi: 10.3390/foods9060726. Foods. 2020. PMID: 32498461 Free PMC article.

References

-

- Lim SS, Vos T, Flaxman AD, Danaei G, Shibuya K, et al. (2012) A comparative risk assessment of burden of disease and injury attributable to 67 risk factors and risk factor clusters in 21 regions, 1990—2010: a systematic analysis for the Global Burden of Disease Study 2010. The Lancet 380 9859: 2224–2260. - PMC - PubMed

-

- Anderson P, Chisholm D, Fuhr DC (2009) Effectiveness and cost-effectiveness of policies and programmes to reduce the harm caused by alcohol. The Lancet 373: 2234–46. - PubMed

-

- Chikritzhs T, Stockwell T, Pascal R (2005) The impact of the Northern Territory's Living With Alcohol program, 1992–2002: revisiting the evaluation. Addiction 100: 1625–1636. - PubMed

-

- Carragher N, Chalmers J (2011) What are the options? Pricing and taxation policy reforms to reduce excessive alcohol consumption and related harms in Australia. Sydney: NSW Bureau of Crime Statistics and Research.

-

- Sornpaisarn B, Shield KD, Rehm J (2012) Alcohol taxation policy in Thailand: implications for other low- to middle-income countries. Addiction 107: 1372–1384. - PubMed

Publication types

MeSH terms

LinkOut - more resources

Full Text Sources

Other Literature Sources

Medical