Cortisol shifts financial risk preferences

- PMID: 24550472

- PMCID: PMC3948282

- DOI: 10.1073/pnas.1317908111

Cortisol shifts financial risk preferences

Abstract

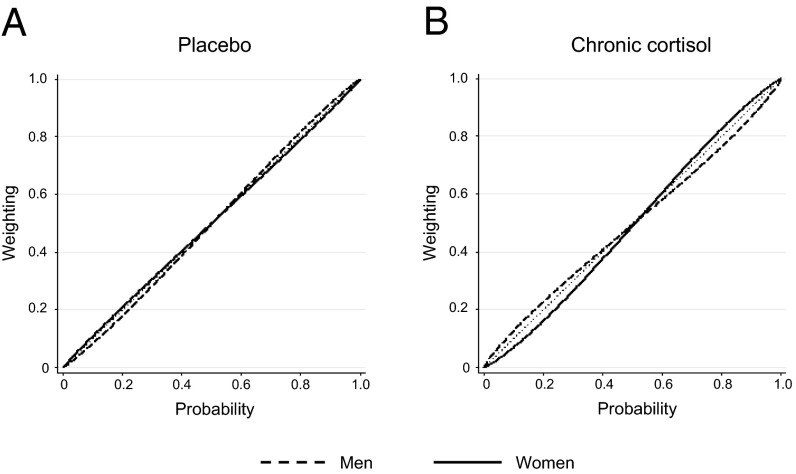

Risk taking is central to human activity. Consequently, it lies at the focal point of behavioral sciences such as neuroscience, economics, and finance. Many influential models from these sciences assume that financial risk preferences form a stable trait. Is this assumption justified and, if not, what causes the appetite for risk to fluctuate? We have previously found that traders experience a sustained increase in the stress hormone cortisol when the amount of uncertainty, in the form of market volatility, increases. Here we ask whether these elevated cortisol levels shift risk preferences. Using a double-blind, placebo-controlled, cross-over protocol we raised cortisol levels in volunteers over 8 d to the same extent previously observed in traders. We then tested for the utility and probability weighting functions underlying their risk taking and found that participants became more risk-averse. We also observed that the weighting of probabilities became more distorted among men relative to women. These results suggest that risk preferences are highly dynamic. Specifically, the stress response calibrates risk taking to our circumstances, reducing it in times of prolonged uncertainty, such as a financial crisis. Physiology-induced shifts in risk preferences may thus be an underappreciated cause of market instability.

Conflict of interest statement

The authors declare no conflict of interest.

Figures

References

-

- Luigino B, Sugden R. The road not taken: How psychology was removed from economics, and how it might be brought back. Econ J. 2007;117(516):146–173.

-

- Gai P, Vause N. Measuring investors' risk appetite. Int J Cent Bank. 2006;2:167–188.

-

- European Central Bank (2007) Measuring investors' risk appetite. Financial Stability Review, June: 166–171.

-

- Samuelson L. Evolutionary Games and Equilibrium Selection. Vol 1. Cambridge, MA: MIT Press; 1998.

-

- Guiso L, Sapienza P, Zingales L. 2013. Time varying risk aversion. NBER Working Paper No. 19284 (National Bureau of Economic Research, Cambridge, MA)

Publication types

MeSH terms

Substances

Grants and funding

LinkOut - more resources

Full Text Sources

Other Literature Sources