Irrational exuberance and neural crash warning signals during endogenous experimental market bubbles

- PMID: 25002476

- PMCID: PMC4115519

- DOI: 10.1073/pnas.1318416111

Irrational exuberance and neural crash warning signals during endogenous experimental market bubbles

Abstract

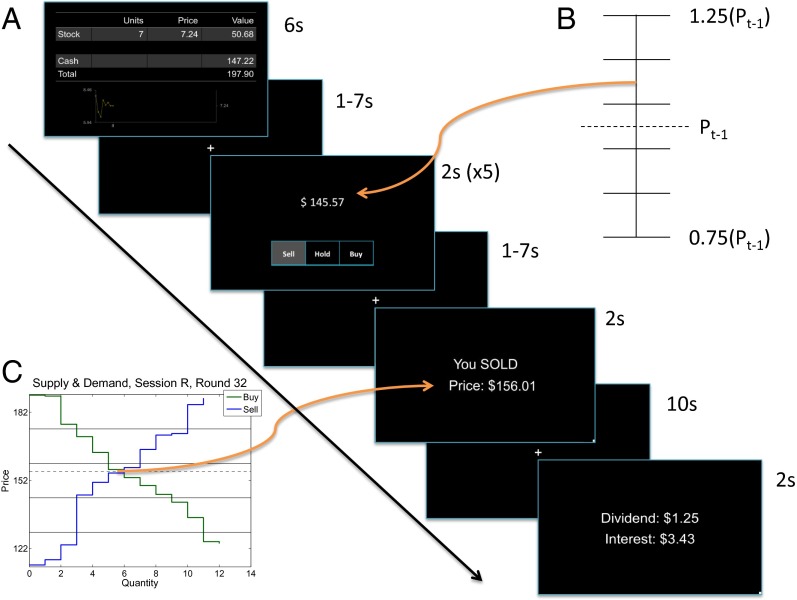

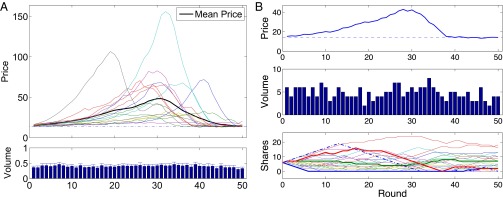

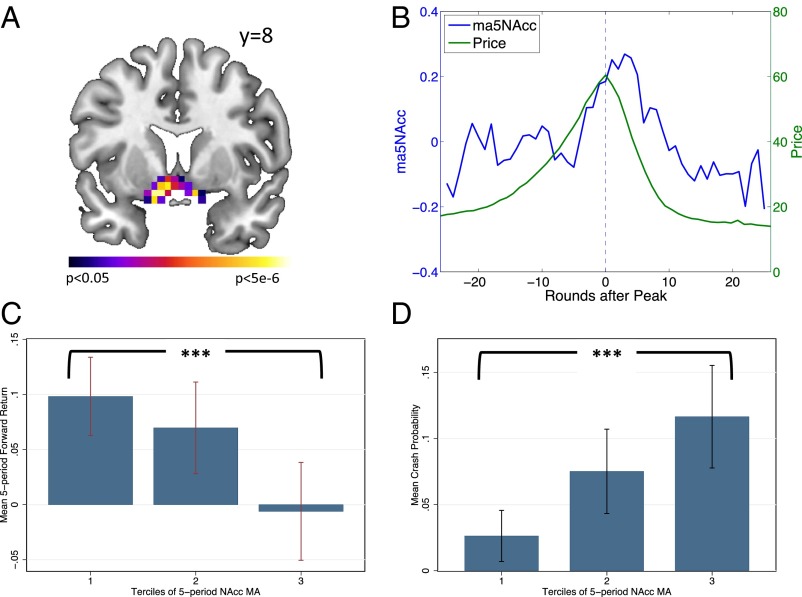

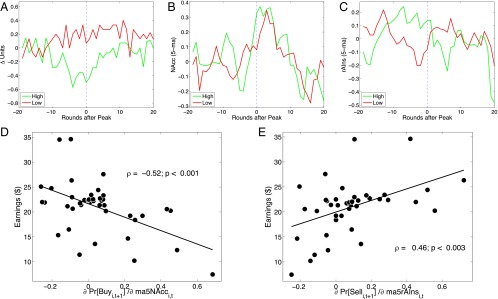

Groups of humans routinely misassign value to complex future events, especially in settings involving the exchange of resources. If properly structured, experimental markets can act as excellent probes of human group-level valuation mechanisms during pathological overvaluations--price bubbles. The connection between the behavioral and neural underpinnings of such phenomena has been absent, in part due to a lack of enabling technology. We used a multisubject functional MRI paradigm to measure neural activity in human subjects participating in experimental asset markets in which endogenous price bubbles formed and crashed. Although many ideas exist about how and why such bubbles may form and how to identify them, our experiment provided a window on the connection between neural responses and behavioral acts (buying and selling) that created the bubbles. We show that aggregate neural activity in the nucleus accumbens (NAcc) tracks the price bubble and that NAcc activity aggregated within a market predicts future price changes and crashes. Furthermore, the lowest-earning subjects express a stronger tendency to buy as a function of measured NAcc activity. Conversely, we report a signal in the anterior insular cortex in the highest earners that precedes the impending price peak, is associated with a higher propensity to sell in high earners, and that may represent a neural early warning signal in these subjects. Such markets could be a model system to understand neural and behavior mechanisms in other settings where emergent group-level activity exhibits mistaken belief or valuation.

Keywords: asset bubbles; hyperscanning; neuroeconomics.

Conflict of interest statement

The authors declare no conflict of interest.

Figures

References

-

- Flood RP, Garber PM. Market fundamentals versus price-level bubbles: The first tests. J Polit Econ. 1980;88(4):745–770.

-

- Kindleberger CP, Aliber RZ. Manias, Panics, and Crashes: A History of Financial Crises. Hoboken, NJ: Wiley; 2005.

-

- Shiller R. Irrational Exuberance. 2nd Ed. New York: Broadway Books; 2005.

-

- Ofek E, Richardson M. Dotcom mania: The rise and fall of internet stock prices. J Finance. 2003;58(3):1113–1138.

-

- Akerlof G, Shiller R. Animal Spirits: How Human Psychology Drives the Economy, and Why It Matters for Global Capitalism. Princeton: Princeton Univ Press; 2009.

Publication types

MeSH terms

Grants and funding

LinkOut - more resources

Full Text Sources

Other Literature Sources

Miscellaneous