Scalar utility theory and proportional processing: What does it actually imply?

- PMID: 27288541

- PMCID: PMC5683348

- DOI: 10.1016/j.jtbi.2016.06.003

Scalar utility theory and proportional processing: What does it actually imply?

Abstract

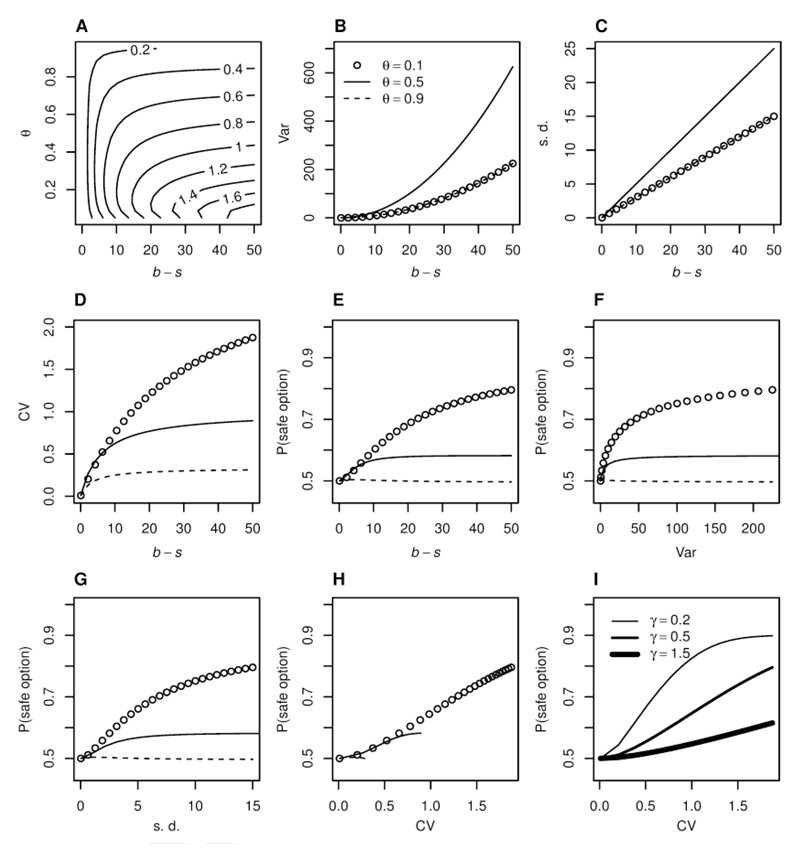

Scalar Utility Theory (SUT) is a model used to predict animal and human choice behaviour in the context of reward amount, delay to reward, and variability in these quantities (risk preferences). This article reviews and extends SUT, deriving novel predictions. We show that, contrary to what has been implied in the literature, (1) SUT can predict both risk averse and risk prone behaviour for both reward amounts and delays to reward depending on experimental parameters, (2) SUT implies violations of several concepts of rational behaviour (e.g. it violates strong stochastic transitivity and its equivalents, and leads to probability matching) and (3) SUT can predict, but does not always predict, a linear relationship between risk sensitivity in choices and coefficient of variation in the decision-making experiment. SUT derives from Scalar Expectancy Theory which models uncertainty in behavioural timing using a normal distribution. We show that the above conclusions also hold for other distributions, such as the inverse Gaussian distribution derived from drift-diffusion models. A straightforward way to test the key assumptions of SUT is suggested and possible extensions, future prospects and mechanistic underpinnings are discussed.

Keywords: Decision making; Risk preferences; Scalar expectancy theory; Scalar property; Weber's law.

Copyright © 2016 Elsevier Ltd. All rights reserved.

Conflict of interest statement

The authors declare no conflicting interests.

Figures

References

-

- Allan LG, Gibbon J. Human bisection at the geometric mean. Learning and Motivation. 1991;22(1–2):39–58. doi: 10.1016/0023-9690(91)90016-2. - DOI

-

- Barnard CJ, Brown CAJ, Houston AI, McNamara JM. Risk-sensitive foraging in common shrews: an interruption model and the effects of mean and variance in reward rate. Behavioral Ecology and Sociobiology. 1985;18(2):139–146.

-

- Bateson M, Kacelnik A. Accuracy of memory for amount in the foraging starling, Sturnus vulgaris. Animal Behaviour. 1995a;50(2):431–443. doi: 10.1006/anbe.1995.0257. - DOI

Publication types

MeSH terms

Grants and funding

LinkOut - more resources

Full Text Sources

Other Literature Sources