A deep learning framework for financial time series using stacked autoencoders and long-short term memory

- PMID: 28708865

- PMCID: PMC5510866

- DOI: 10.1371/journal.pone.0180944

A deep learning framework for financial time series using stacked autoencoders and long-short term memory

Abstract

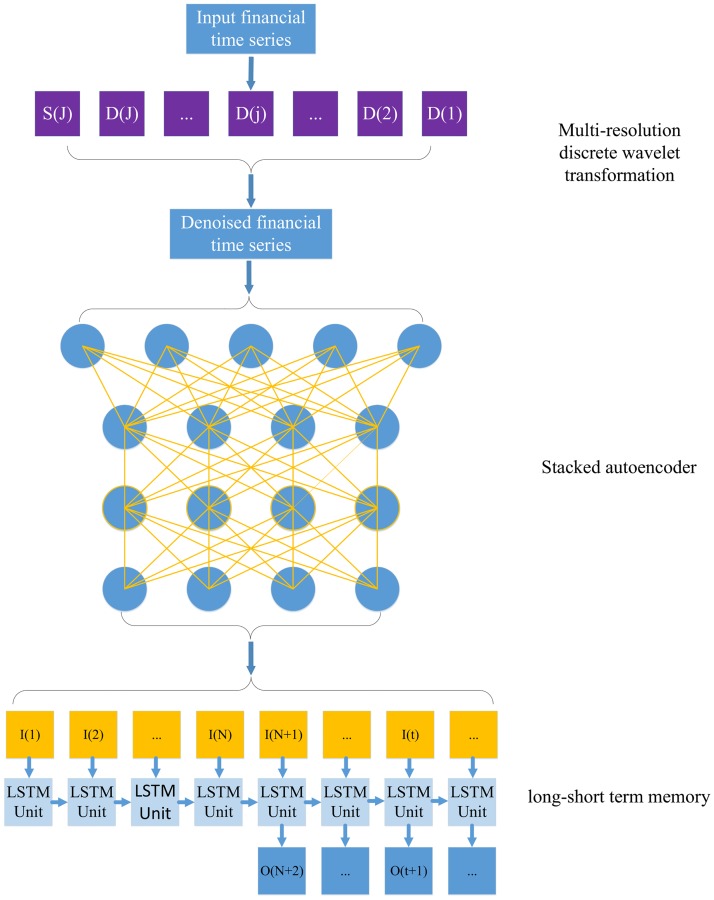

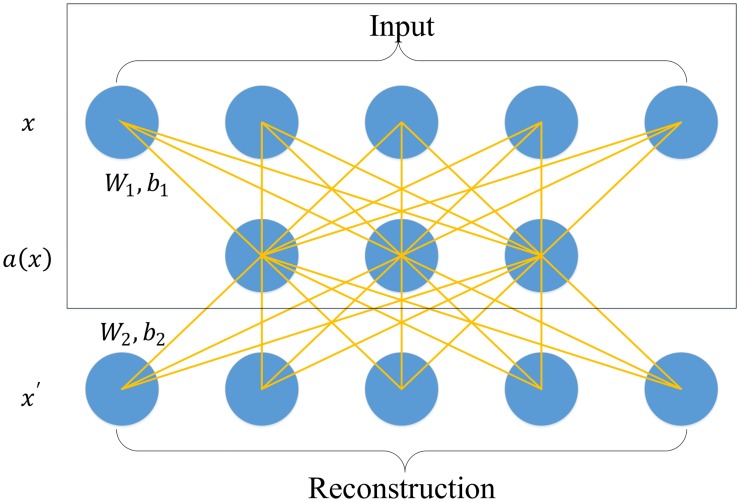

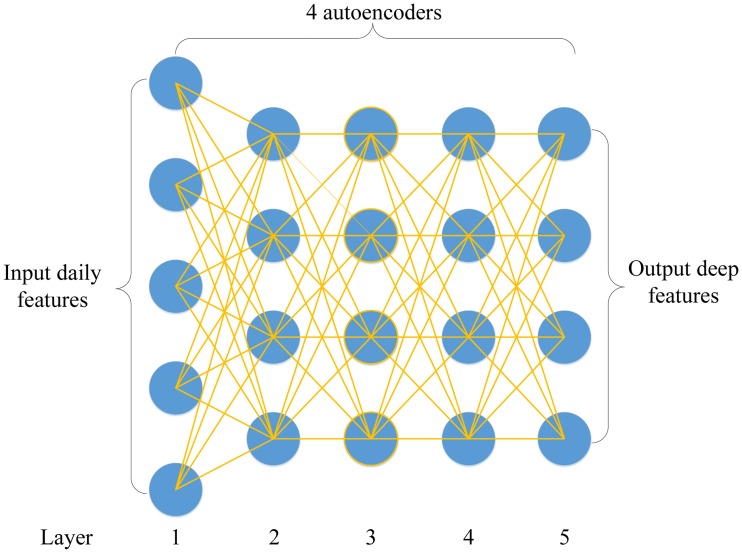

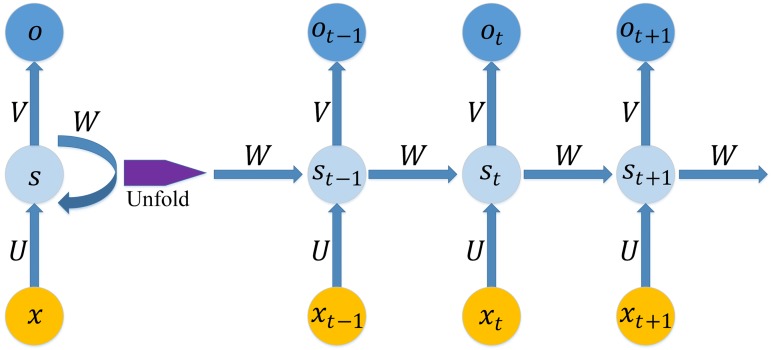

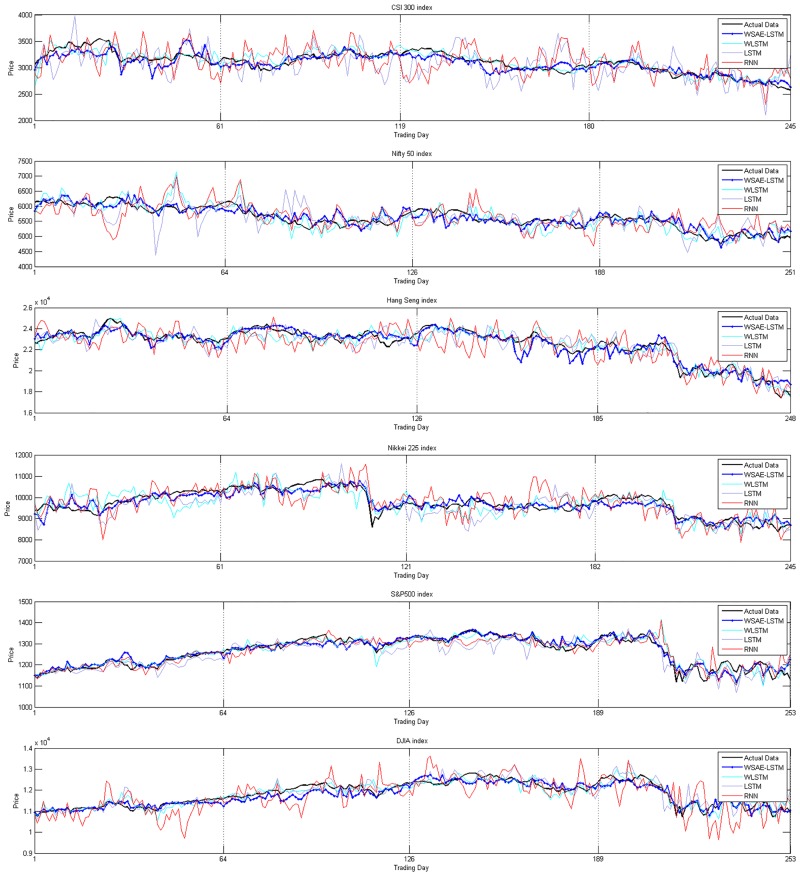

The application of deep learning approaches to finance has received a great deal of attention from both investors and researchers. This study presents a novel deep learning framework where wavelet transforms (WT), stacked autoencoders (SAEs) and long-short term memory (LSTM) are combined for stock price forecasting. The SAEs for hierarchically extracted deep features is introduced into stock price forecasting for the first time. The deep learning framework comprises three stages. First, the stock price time series is decomposed by WT to eliminate noise. Second, SAEs is applied to generate deep high-level features for predicting the stock price. Third, high-level denoising features are fed into LSTM to forecast the next day's closing price. Six market indices and their corresponding index futures are chosen to examine the performance of the proposed model. Results show that the proposed model outperforms other similar models in both predictive accuracy and profitability performance.

Conflict of interest statement

Figures

References

-

- Wang B, Huang H, Wang X. A novel text mining approach to financial time series forecasting. Neurocomputing. 2012;83(6):136–45.

-

- Cherkassky V. The nature of statistical learning theory: Springer; 1997. - PubMed

-

- Refenes AN, Zapranis A, Francis G. Stock performance modeling using neural networks: A comparative study with regression models. Neural Networks. 1994;7(2):375–88.

-

- Yoon Y, Margavio TM. A Comparison of Discriminant Analysis versus Artificial Neural Networks. Journal of the Operational Research Society. 1993;44(1):51–60.

MeSH terms

LinkOut - more resources

Full Text Sources

Other Literature Sources