Impact of tax and subsidy framed messages on high- and lower-sugar beverages sold in vending machines: a randomized crossover trial

- PMID: 30103793

- PMCID: PMC6090625

- DOI: 10.1186/s12966-018-0711-3

Impact of tax and subsidy framed messages on high- and lower-sugar beverages sold in vending machines: a randomized crossover trial

Abstract

Objective: Framing of fiscal incentives has been suggested to be important in influencing purchase decisions. We aimed to examine the effect of framing a modest price difference between high- and lower-sugar beverages as a tax or a subsidy respectively, using messages placed on vending machines to influence beverage purchases.

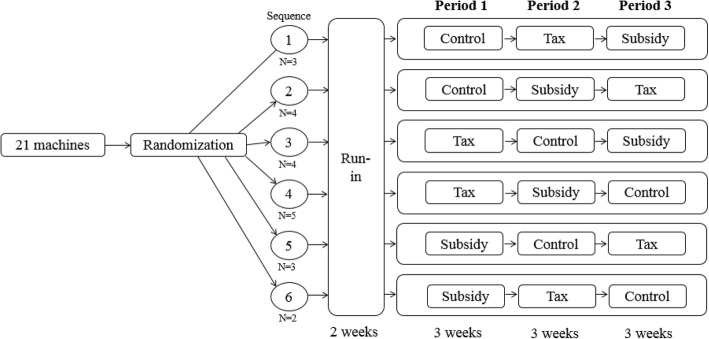

Design/setting: This is an 11-week randomized crossover trial conducted between August and November 2015, with a two-week run-in period before intervention, targeted at students, staff and faculty of a university campus in Singapore. Twenty-one beverage vending machines were used to implement the intervention involving 'tax message', 'subsidy message' and 'no message (control)'. The former two messages suggest 'a tax for high sugar beverages' or 'a subsidy for lower sugar beverages' respectively. Prices of the beverages offered were fixed at baseline and remained the same in all three experimental conditions: lower-sugar beverage options were priced ~ 10% lower than the corresponding high-sugar option. The machines were randomized to one of the 6 sequences of intervention. Each message intervention period was 3 weeks. The effect of messages was assessed by comparing average weekly units of beverages sold between interventions using mixed effects model.

Results: The average weekly units of high and lower-sugar beverages sold per vending machine were 115 and 98 respectively in the control condition. The percentage of high-sugar beverages sold was 54% in the control, 53% in the tax, and 54% in the subsidy message condition. There was no difference in the weekly units of high-sugar beverages sold for the tax message (- 2, 95% CI -8 to 5, p = 0.61) or the subsidy message (0, 95% CI -10 to 10, p = 0.96) conditions as compared with the control condition. Similarly, there was no difference in the weekly units of lower-sugar beverages sold for the tax message (4, 95% CI -4 to 13, p = 0.32) or the subsidy message (7, 95% CI -4 to 18, p = 0.18) conditions as compared with the control condition.

Conclusions: The use of tax and subsidy messages to highlight modest price differences did not substantially reduce high-sugar beverage sales in vending machines on an Asian university campus.

Keywords: Crossover trial; Health Behaviours; Message framing; Sugar sweetened beverages; Vending machines.

Conflict of interest statement

The trial was not submitted to any ethics committee as the National University of Singapore IRB exempts studies of this nature from the requirement of IRB approval: we did not approach any human subjects or collect any information from individuals. In addition, the changes in the vending machines were modest changes in price, beverage offerings or messages that would not present any risk to consumers of the machines, and does not affect their rights and welfare.

Not applicable.

The authors declare that they have no competing interests.

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Figures

References

Publication types

MeSH terms

Substances

Grants and funding

LinkOut - more resources

Full Text Sources

Other Literature Sources