Forecasting stock prices with a feature fusion LSTM-CNN model using different representations of the same data

- PMID: 30768647

- PMCID: PMC6377125

- DOI: 10.1371/journal.pone.0212320

Forecasting stock prices with a feature fusion LSTM-CNN model using different representations of the same data

Abstract

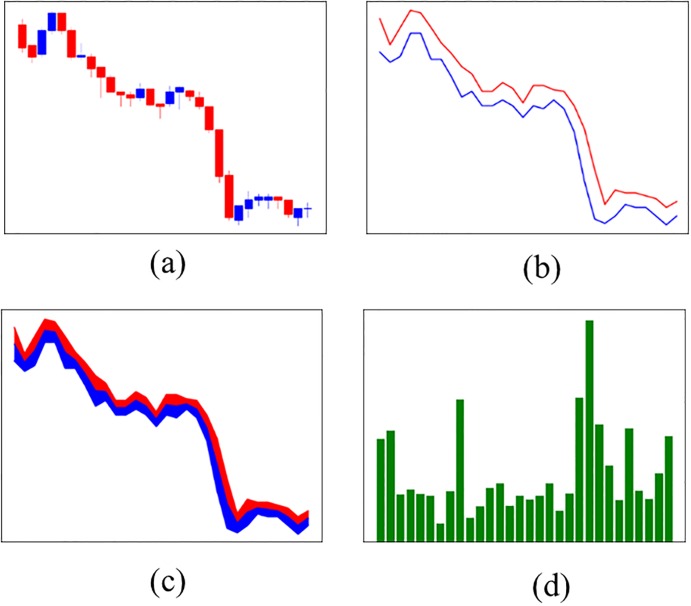

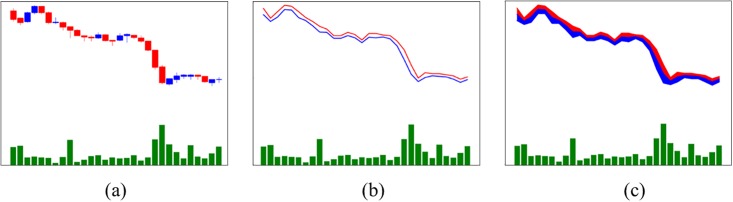

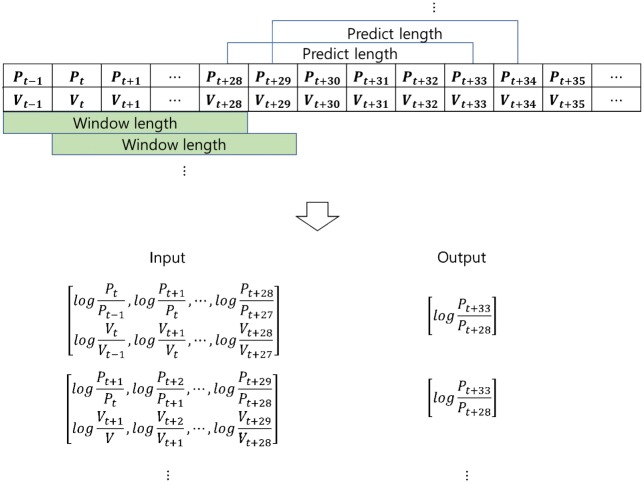

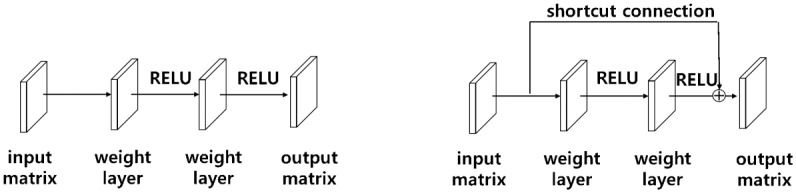

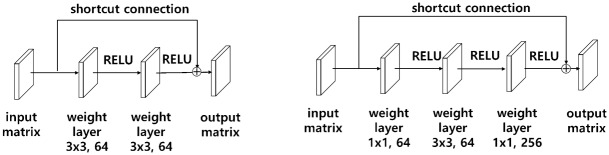

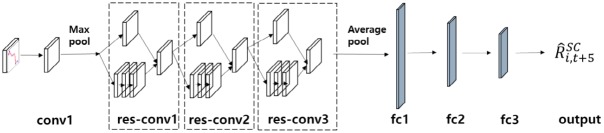

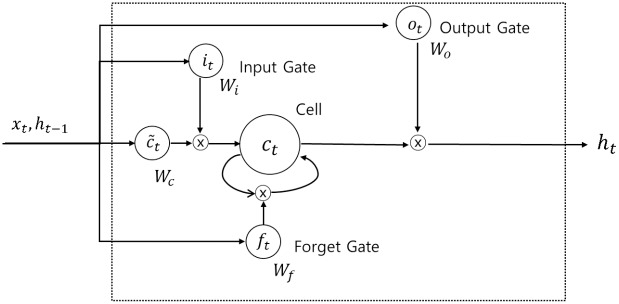

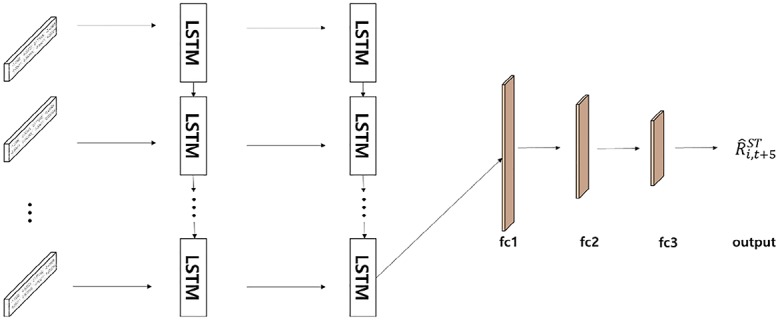

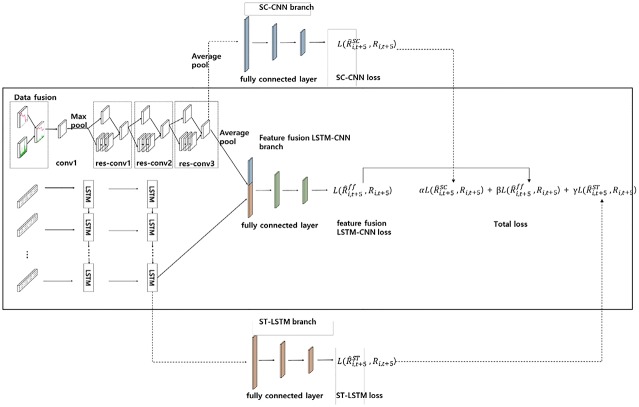

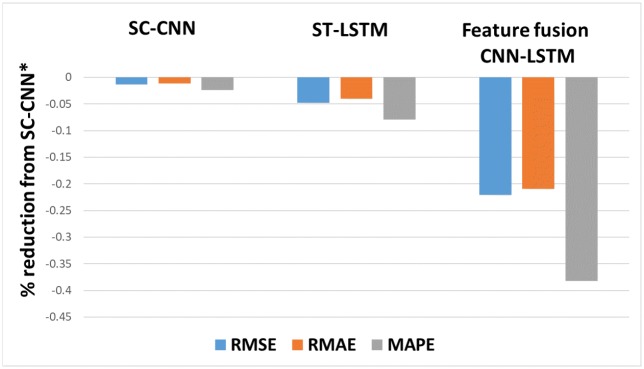

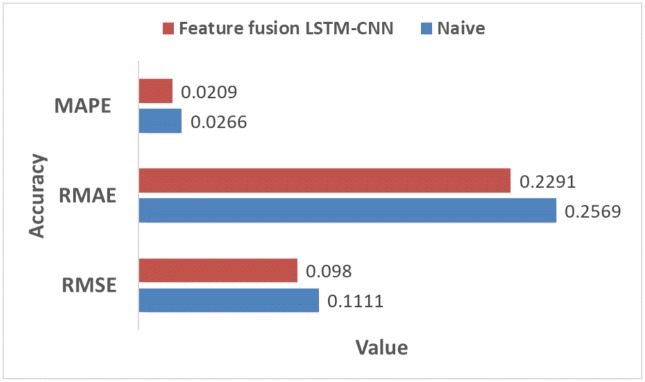

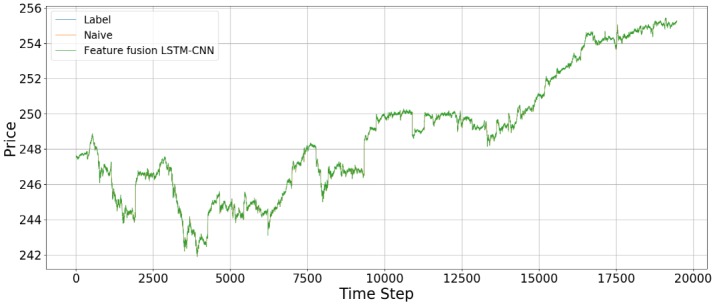

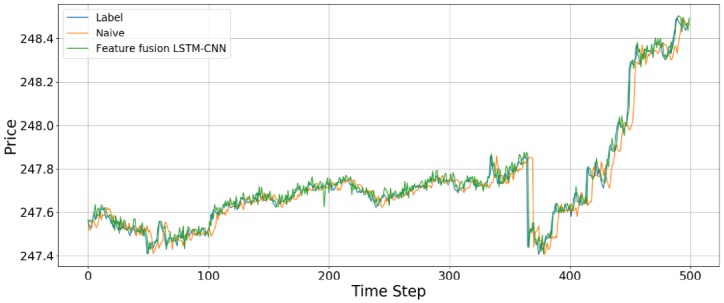

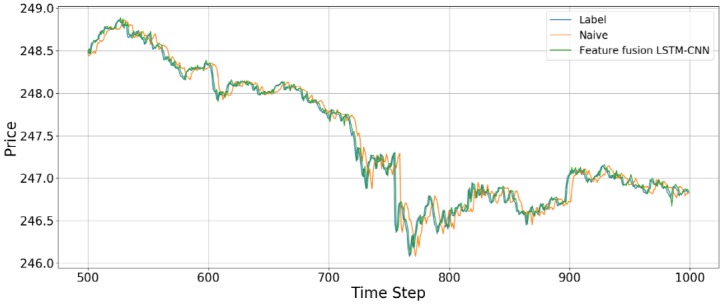

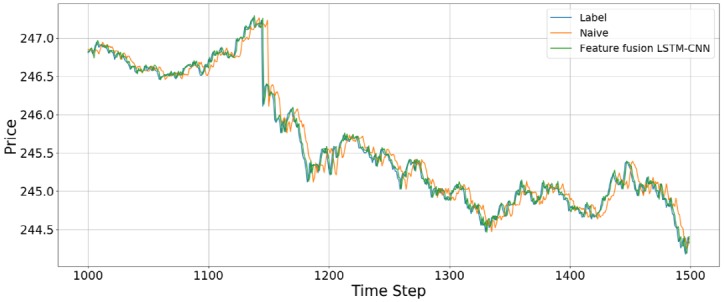

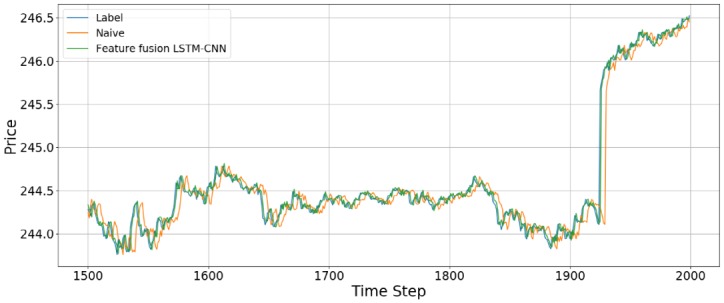

Forecasting stock prices plays an important role in setting a trading strategy or determining the appropriate timing for buying or selling a stock. We propose a model, called the feature fusion long short-term memory-convolutional neural network (LSTM-CNN) model, that combines features learned from different representations of the same data, namely, stock time series and stock chart images, to predict stock prices. The proposed model is composed of LSTM and a CNN, which are utilized for extracting temporal features and image features. We measure the performance of the proposed model relative to those of single models (CNN and LSTM) using SPDR S&P 500 ETF data. Our feature fusion LSTM-CNN model outperforms the single models in predicting stock prices. In addition, we discover that a candlestick chart is the most appropriate stock chart image to use to forecast stock prices. Thus, this study shows that prediction error can be efficiently reduced by using a combination of temporal and image features from the same data rather than using these features separately.

Conflict of interest statement

The authors have declared that no competing interests exist.

Figures

References

-

- Cowles A. Can Stock Market Forecasters Forecast? Econom. 1933;1:309.

-

- Fama EF. Efficient Capital Markets-A Review of Theory and Empirical Work. J Finance [Internet]. 1970;25(2):383–417. Available from: http://books.google.de/books?id=ox48PAAACAAJ&dq=intitle:Efficient+Capita...

-

- Tsang PM, Kwok P, Choy SO, Kwan R, Ng SC, Mak J, et al. Design and implementation of NN5 for Hong Kong stock price forecasting. Eng Appl Artif Intell [Internet]. 2007;20(4):453–61. Available from: http://linkinghub.elsevier.com/retrieve/pii/S095219760600162X

-

- Brooks C. Predicting stock index volatility: Can market volume help? J Forecast. 1998;17(1):59–80.

Publication types

MeSH terms

Associated data

LinkOut - more resources

Full Text Sources