Sweetened beverage taxes and changes in beverage price, imports and manufacturing: interrupted time series analysis in a middle-income country

- PMID: 32646500

- PMCID: PMC7350205

- DOI: 10.1186/s12966-020-00980-1

Sweetened beverage taxes and changes in beverage price, imports and manufacturing: interrupted time series analysis in a middle-income country

Abstract

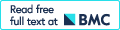

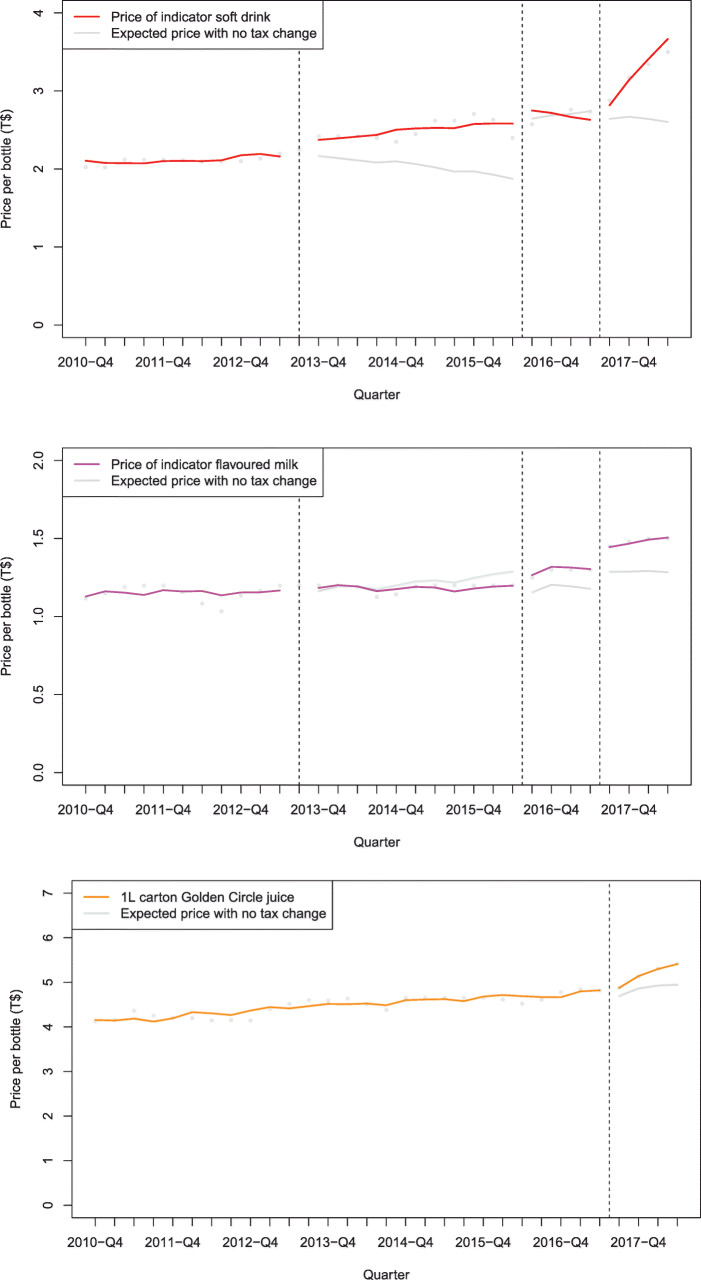

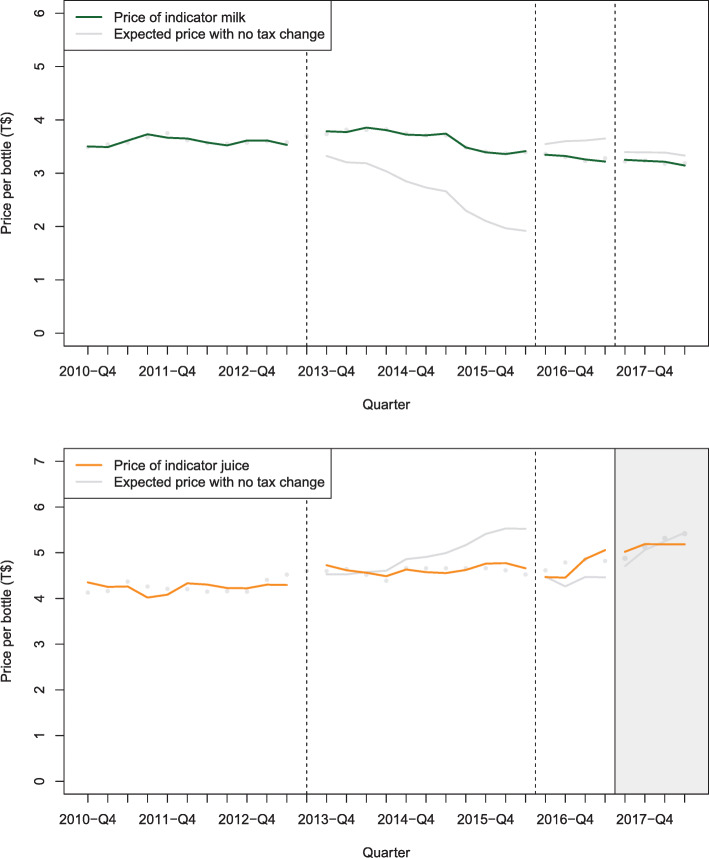

Background: The Pacific Island nation of Tonga (a middle-income country) introduced a sweetened beverage tax of T$0.50/L in 2013, with this increasing further in 2016 (to T$1.00/L), and in 2017 (T$1.50/L; US$0.02/oz). Given the potential importance of such types of fiscal intervention for preventing chronic disease, we aimed to evaluate the impact of these tax changes in Tonga.

Methods: Interrupted time series analysis was used to examine monthly import volumes and quarterly price and manufacturing 1 year after each tax change, compared with a counterfactual based on existing trends. Autocorrelation was adjusted for when present, and adjustments were made for changes in GDP per capita, visitor numbers, season and T$/US$ exchange rate.

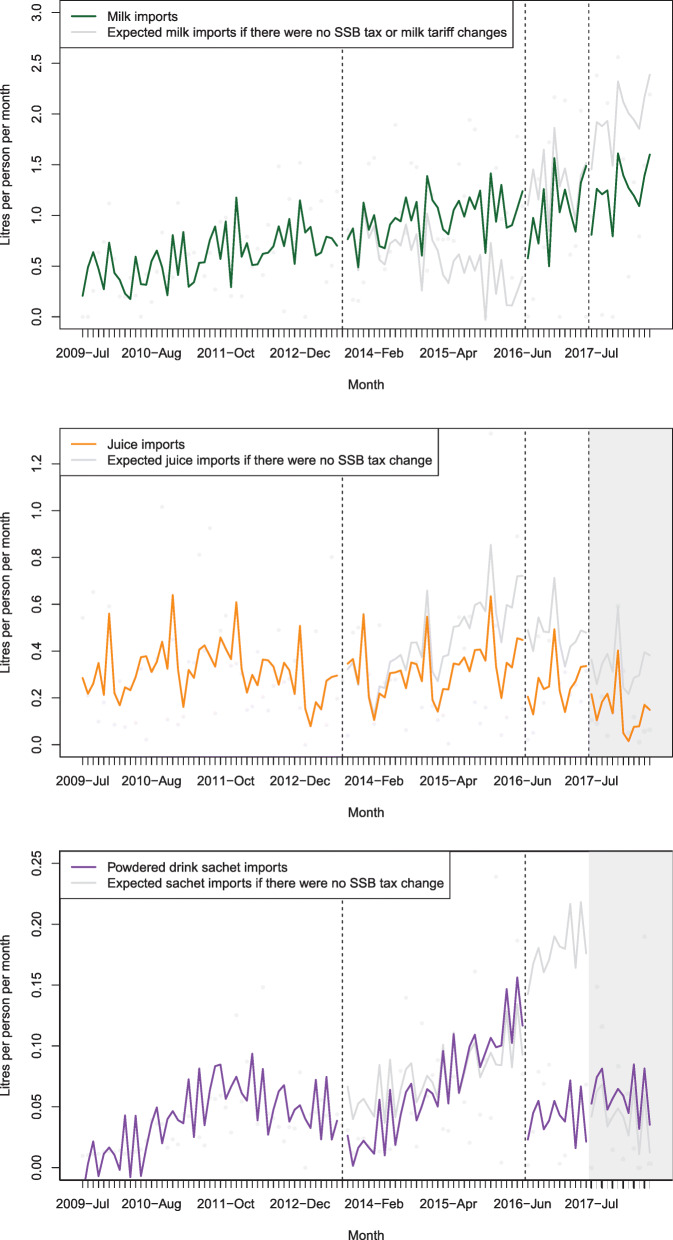

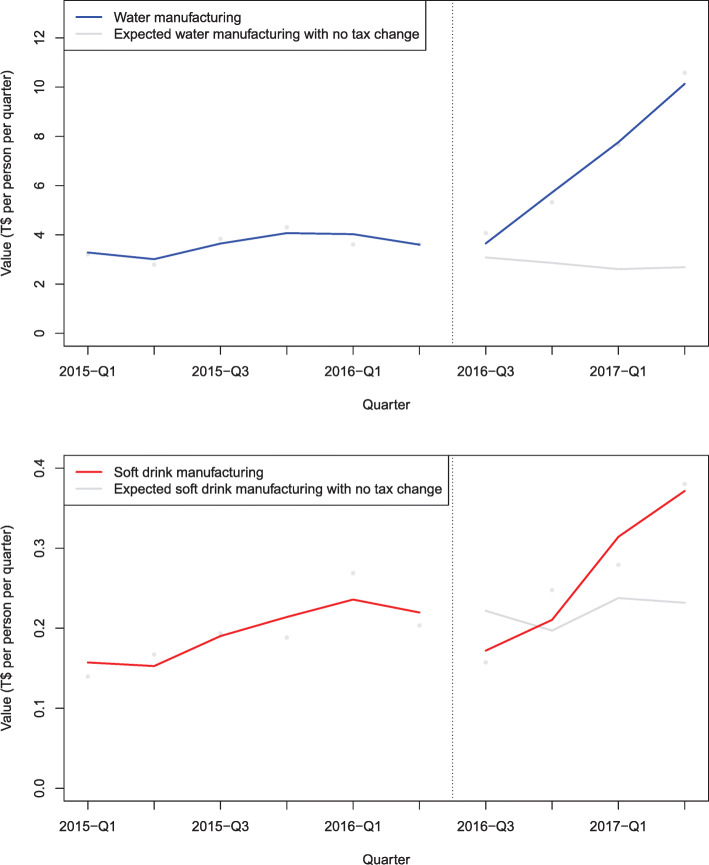

Results: In the year after the 2013, 2016 and 2017 tax increases, the price of an indicator soft drink increased by 16.8% (95%CI: 6.3 to 29.6), 3.7% (- 0.6 to 8.3) and 17.6% (6.0 to 32.0) respectively. Imports of sweetened beverages decreased with changes of - 10.4% (- 23.6 to 9.0), - 30.3% (- 38.8 to - 20.5) and - 62.5% (- 73.1 to - 43.4) respectively. Juice imports changed by - 54.2% (- 93.2 to - 1.1), and sachet drinks by - 15.5% (- 67.8 to 88.3) after the 2017 tax increase. Tonga water bottling (T$) increased in value by 143% (69 to 334) after the 2016 tax increase and soft drink manufacturing increased by 20% (2 to 46, albeit 5% market share).

Conclusions: Consistent with international evaluations of sugar-sweetened beverage taxes, the taxes in Tonga were associated with increased prices, decreased taxed beverages imports, and increased locally bottled water.

Keywords: Evaluation; Natural experiment; Pacific; Quasi experiment; Soft drink; Sugar-sweetened beverages; Sugary drinks; Taxes; Time-series; Tonga; Trade.

Conflict of interest statement

The authors declare that they have no competing interests.

Figures

References

-

- The Pacific Monitoring Alliance for Non-communicable disease Action (Pacific MANA) Coordination team, Pacific Community (SPC). Status of NCD policy and legislation in Pacific Island Countries and Territories, 2018. (The Pacific Monitoring Alliance for Non-communicable disease Action (Pacific MANA) ed. pp. 1–35). Noumea: Pacific Community; 2019. p. 1–35.

-

- World Bank, editor. Using taxation to address noncommunicable diseases lessons from Tonga. (World Bank ed. pp. 1–127) Washington DC: Food and Agriculture Organization of the United Nations, TongaHealth, Australian Aid, New Zealand Foreign Affairs and Trade Aid Programme, Government of Japan; 2019. pp. 1–127.

Publication types

MeSH terms

LinkOut - more resources

Full Text Sources