The impact of COVID-19 on small business outcomes and expectations

- PMID: 32651281

- PMCID: PMC7395529

- DOI: 10.1073/pnas.2006991117

The impact of COVID-19 on small business outcomes and expectations

Abstract

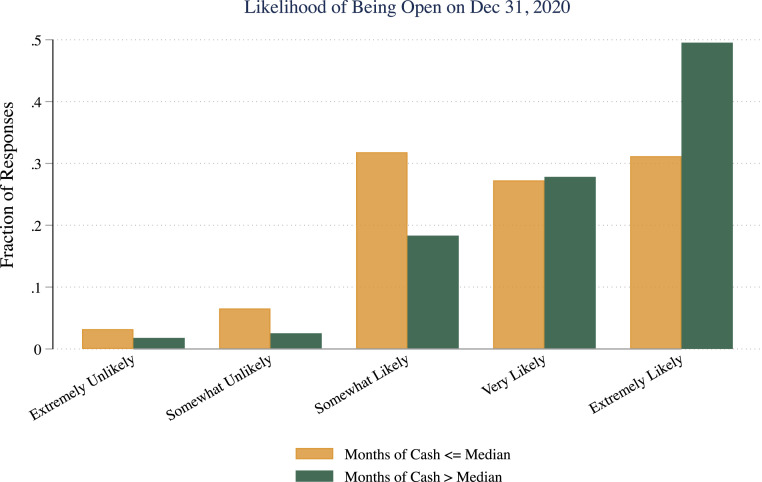

To explore the impact of coronavirus disease 2019 (COVID-19) on small businesses, we conducted a survey of more than 5,800 small businesses between March 28 and April 4, 2020. Several themes emerged. First, mass layoffs and closures had already occurred-just a few weeks into the crisis. Second, the risk of closure was negatively associated with the expected length of the crisis. Moreover, businesses had widely varying beliefs about the likely duration of COVID-related disruptions. Third, many small businesses are financially fragile: The median business with more than $10,000 in monthly expenses had only about 2 wk of cash on hand at the time of the survey. Fourth, the majority of businesses planned to seek funding through the Coronavirus Aid, Relief, and Economic Security (CARES) Act. However, many anticipated problems with accessing the program, such as bureaucratic hassles and difficulties establishing eligibility. Using experimental variation, we also assess take-up rates and business resilience effects for loans relative to grants-based programs.

Keywords: CARES Act; COVID-19; small businesses.

Copyright © 2020 the Author(s). Published by PNAS.

Conflict of interest statement

The authors declare no competing interest.

Figures

References

-

- Faulkender M. W., Cash holdings among small businesses. 10.2139/ssrn.305179 (2 April 2002). - DOI

-

- La Rocca M., Staglianò R., La Rocca T., Cariola A., Skatova E., Cash holdings and sme performance in Europe: The role of firm-specific and macroeconomic moderators. Small Bus. Econ. 53, 1051–1078 (2019).

-

- Goldfarb A., Xiao M., Who thinks about the competition? Managerial ability and strategic entry in US local telephone markets. Am. Econ. Rev. 101, 3130–3161 (2011).

-

- DellaVigna S., Gentzkow M., Uniform pricing in us retail chains. Q. J. Econ. 134, 2011–2084 (2019).

-

- Strulov-Shlain A. S., More than a Penny’s Worth: Left-Digit Bias and Firm Pricing (University of California, Berkeley, 2018).

MeSH terms

LinkOut - more resources

Full Text Sources

Miscellaneous