A quantitative easing experiment

- PMID: 32904555

- PMCID: PMC7455802

- DOI: 10.1016/j.jedc.2020.103978

A quantitative easing experiment

Abstract

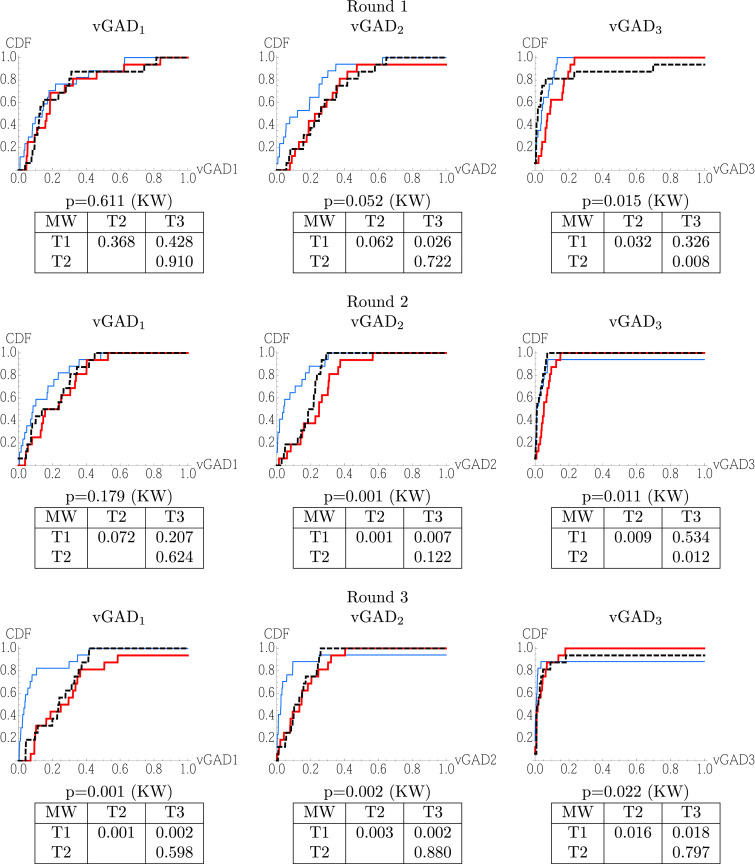

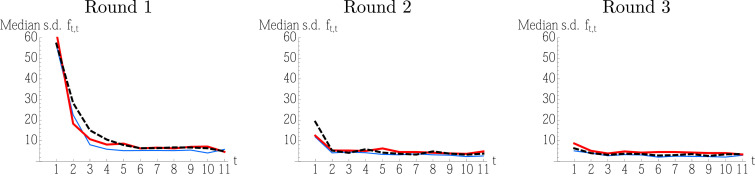

We experimentally investigate the effect of a central bank buying bonds for cash in a quantitative easing (QE) operation. In our experiment, the bonds are perfect substitutes for cash and have a constant fundamental value which is not affected by QE in the rational expectations equilibrium. We find that QE raises bond prices above those in the benchmark treatment without QE. Subjects in the benchmark treatment learned to trade the bonds at their fundamental value but those in treatments with QE became more convinced after repeated exposure to the same treatment that QE boosts bond prices. This suggests the possibility of a behavioural channel for the observed effects of actual QE operations on bond yields.

Keywords: Expectation dynamics; Experimental asset market; Quantitative easing.

© 2020 Elsevier B.V. All rights reserved.

Figures

References

-

- Abbink K., Brandts J., Pezanis-Christou P. Auctions for government securities: a laboratory comparison of uniform, discriminatory and spanish designs, Journal of Economic Behavior and Organization. 2006;61:284–303.

-

- Akiyama E., Hanaki N., Ishikawa R. How do experienced traders respond to inflows of inexperienced traders? an experimental analysis. Journal of Economic Dynamics and Control. 2014;45:1–18.

-

- Akiyama E., Hanaki N., Ishikawa R. It is not just confusion! strategic uncertainty in an experimental asset market, Economic Journal. 2017;127:F563–F580.

-

- Arrata W., Nguyen B. Working papers 623. Banque de France; 2017. Price impact of bond supply shocks: Evidence from the eurosystem’s asset purchase program,

-

- Asparouhova E., Bossaerts P., Roy N., Zame W. ‘Lucas’ in the laboratory. Journal of Finance. 2016;71:2727–2779.

Further reading

-

- Bosch-Rosa C., Meissner T., Bosch-Domènech A. Cognitive bubbles. Experimental Economics. 2018;21:132–153.

-

- Breaban A., Noussair C.N. Trader characteristics and fundamental value trajectories in an asset market experiment, J Behav Exp Finance. 2015;8:1–17.

-

- Janssen D., Füllbrunn S., Weitzel U. Individual speculative behavior and overpricing in experimental asset markets. Experimental Economics. 2019;22:653–675.

LinkOut - more resources

Full Text Sources