Segmentation of time series in up- and down-trends using the epsilon-tau procedure with application to USD/JPY foreign exchange market data

- PMID: 32946503

- PMCID: PMC7500655

- DOI: 10.1371/journal.pone.0239494

Segmentation of time series in up- and down-trends using the epsilon-tau procedure with application to USD/JPY foreign exchange market data

Abstract

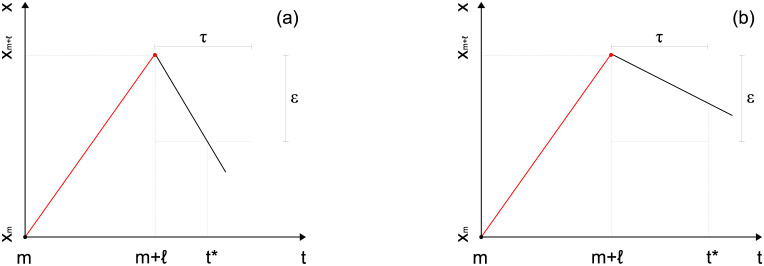

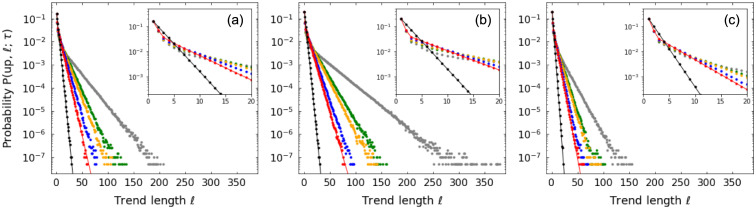

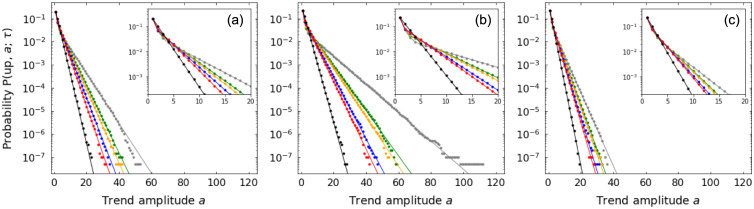

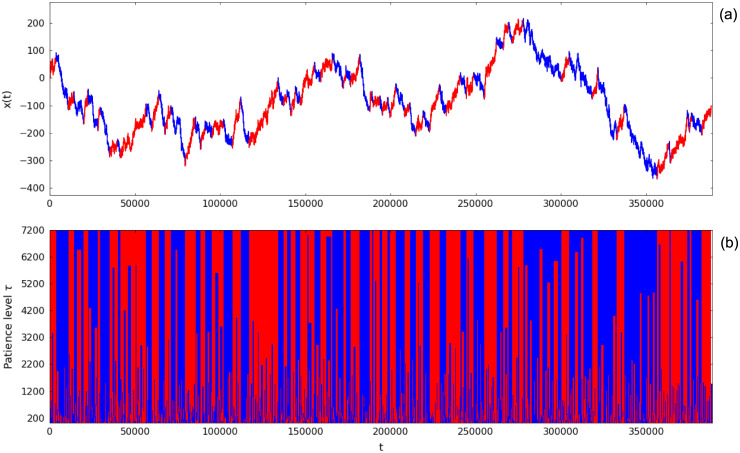

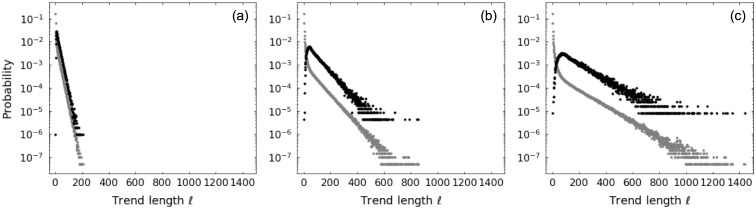

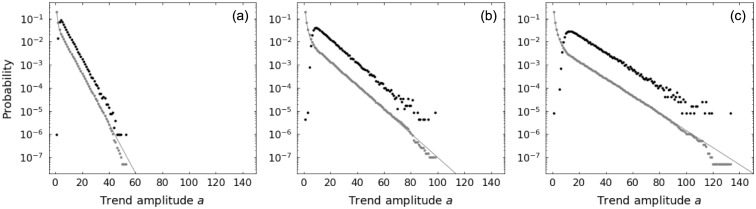

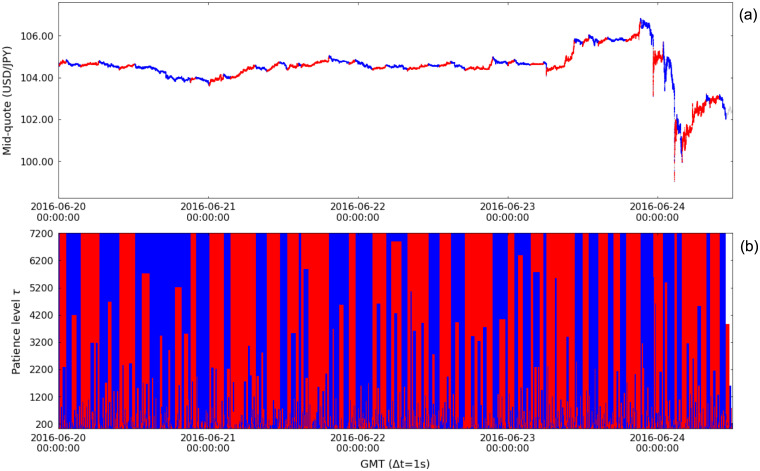

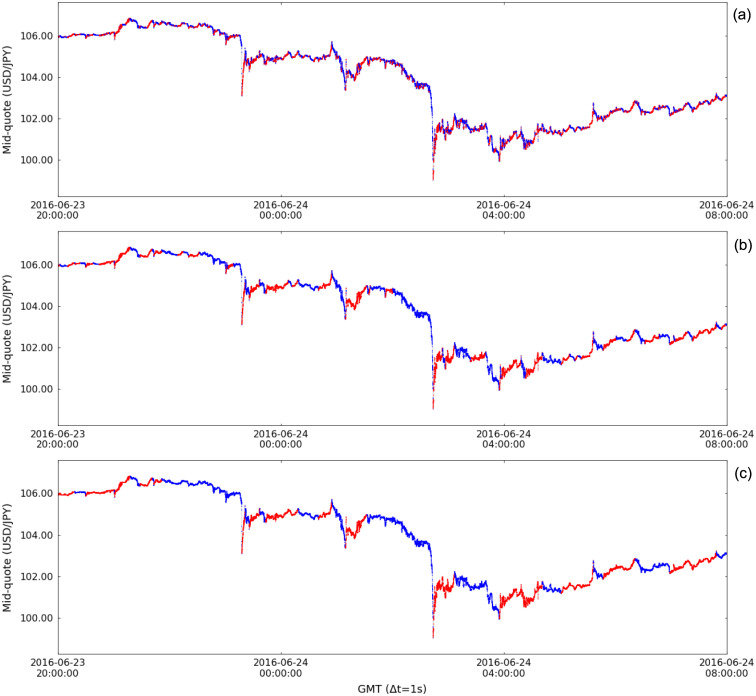

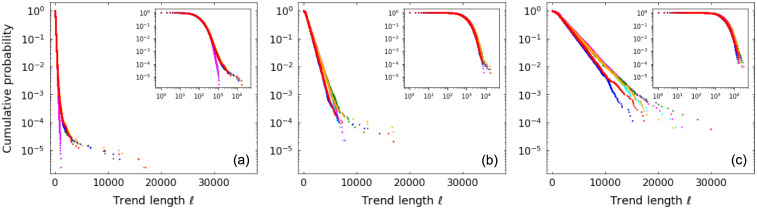

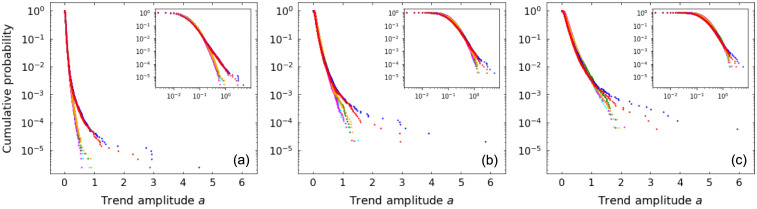

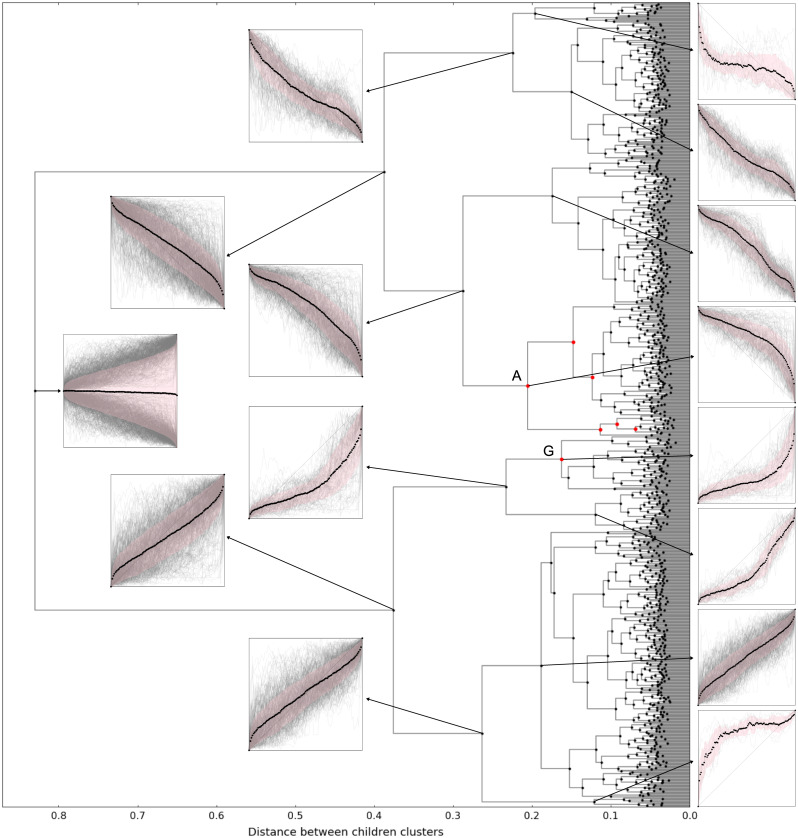

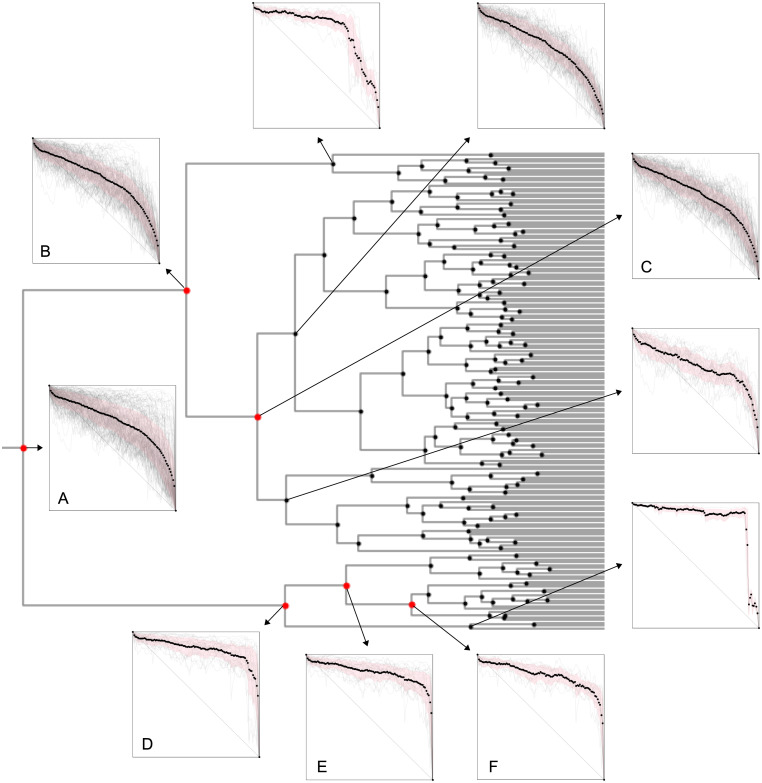

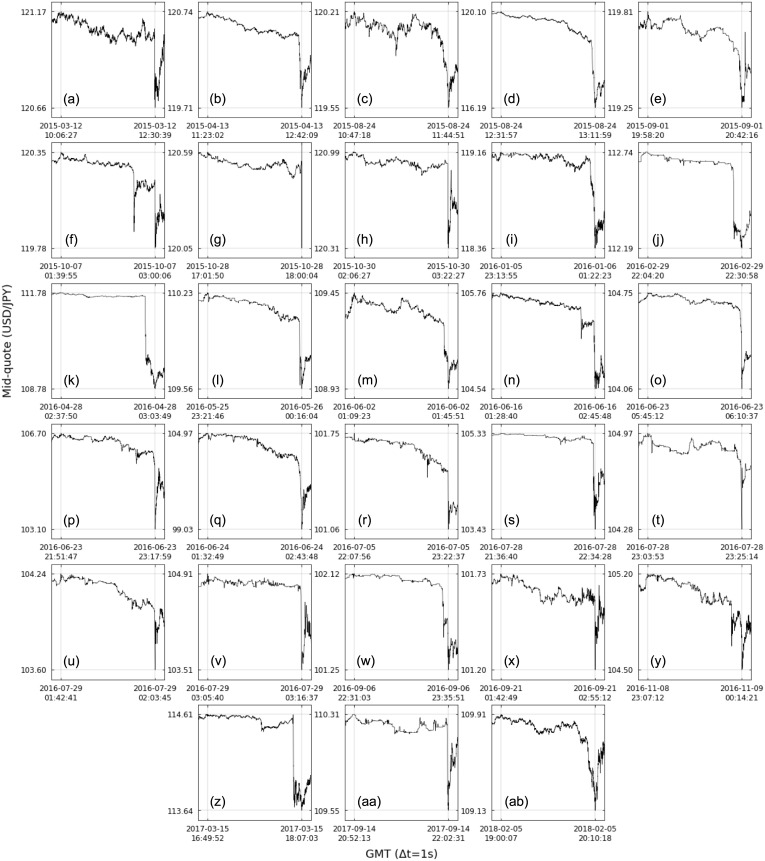

We propose the epsilon-tau procedure to determine up- and down-trends in a time series, working as a tool for its segmentation. The method denomination reflects the use of a tolerance level ε for the series values and a patience level τ in the time axis to delimit the trends. We first illustrate the procedure in discrete random walks, deriving the exact probability distributions of trend lengths and trend amplitudes, and then apply it to segment and analyze the trends of U.S. dollar (USD)/Japanese yen (JPY) market time series from 2015 to 2018. Besides studying the statistics of trend lengths and amplitudes, we investigate the internal structure of the trends by grouping trends with similar shapes and selecting clusters of shapes that rarely occur in the randomized data. Particularly, we identify a set of down-trends presenting similar sharp appreciation of the yen that are associated with exceptional events such as the Brexit Referendum in 2016.

Conflict of interest statement

The authors of this manuscript have the following competing interests: MT receives research funding (the Joint Collaborative Research Laboratory for MUFG AI Financial Market Analysis) from a commercial source (Mitsubishi UFJ financial group) as consultancy of AI trading strategies; HT is employed by Sony Computer Science Laboratories, Inc. There are no patents, products in development or marketed products to declare. This does not alter our adherence to all the PLOS ONE policies on sharing data and materials, as detailed online in the guide for authors.

Figures

Similar articles

-

Evolvement of uniformity and volatility in the stressed global financial village.PLoS One. 2012;7(2):e31144. doi: 10.1371/journal.pone.0031144. Epub 2012 Feb 8. PLoS One. 2012. PMID: 22347444 Free PMC article.

-

Detection of statistical asymmetries in non-stationary sign time series: Analysis of foreign exchange data.PLoS One. 2017 May 18;12(5):e0177652. doi: 10.1371/journal.pone.0177652. eCollection 2017. PLoS One. 2017. PMID: 28542208 Free PMC article.

-

Some comments on Bitcoin market (in)efficiency.PLoS One. 2019 Jul 8;14(7):e0219243. doi: 10.1371/journal.pone.0219243. eCollection 2019. PLoS One. 2019. PMID: 31283773 Free PMC article.

-

The role of foreign direct investment in the nutrition transition.Public Health Nutr. 2005 Jun;8(4):357-65. doi: 10.1079/phn2004706. Public Health Nutr. 2005. PMID: 15975180 Review.

-

[Drug Vial Optimization(DVO)for Anti-Cancer Drugs].Gan To Kagaku Ryoho. 2017 May;44(5):353-356. Gan To Kagaku Ryoho. 2017. PMID: 28536326 Review. Japanese.

Cited by

-

A Forecast Model for COVID-19 Spread Trends Using Blog and GPS Data from Smartphones.Entropy (Basel). 2025 Jun 26;27(7):686. doi: 10.3390/e27070686. Entropy (Basel). 2025. PMID: 40724403 Free PMC article.

References

-

- Fu TC. A review on time series data mining. Eng Appl Artif Intell. 2011;24(1):164–81. 10.1016/j.engappai.2010.09.007 - DOI

-

- Keogh E, Chu S, Hart D, Pazzani M. Segmenting time series: A survey and novel approach In: Last M, Abraham K, Horst B, editors. Data mining in time series databases. Singapore: World scientific; 2004. p. 1–21.

-

- Ducré-Robitaille JF, Vincent LA, Boulet G. Comparison of techniques for detection of discontinuities in temperature series. Int J Climatol. 2003;23(9):1087–101. 10.1002/joc.924 - DOI

-

- Reeves J, Chen J, Wang XL, Lund R, Lu QQ. A review and comparison of changepoint detection techniques for climate data. J Appl Meteorol Climatol. 2007;46(6):900–15. 10.1175/JAM2493.1 - DOI

Publication types

MeSH terms

LinkOut - more resources

Full Text Sources