THE PRICE AIN'T RIGHT? HOSPITAL PRICES AND HEALTH SPENDING ON THE PRIVATELY INSURED

- PMID: 32981974

- PMCID: PMC7517591

- DOI: 10.1093/qje/qjy020

THE PRICE AIN'T RIGHT? HOSPITAL PRICES AND HEALTH SPENDING ON THE PRIVATELY INSURED

Abstract

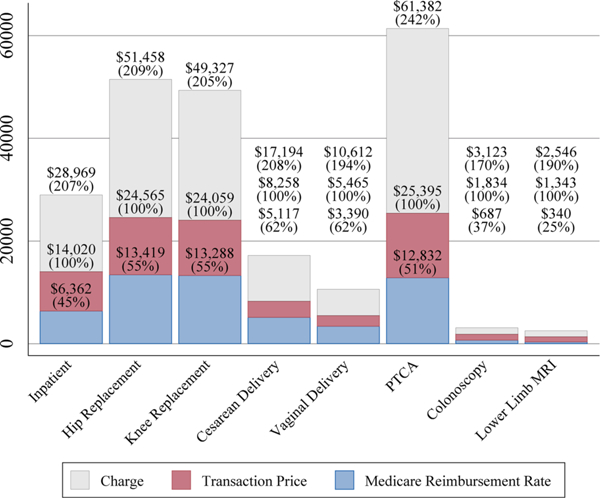

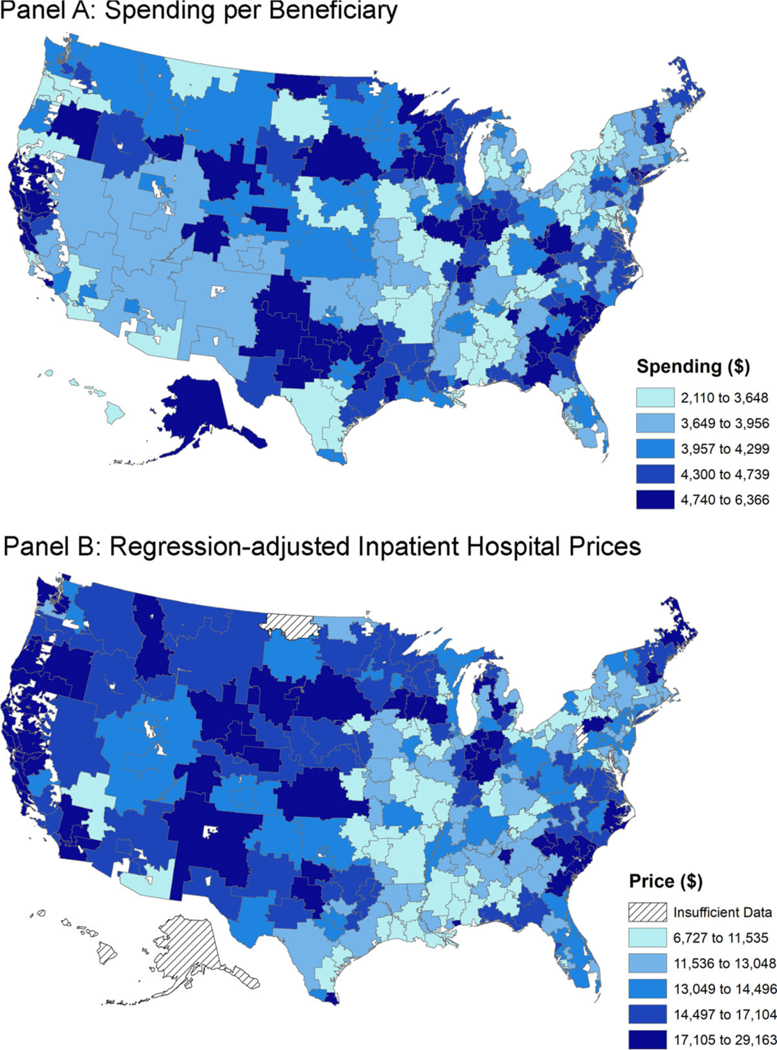

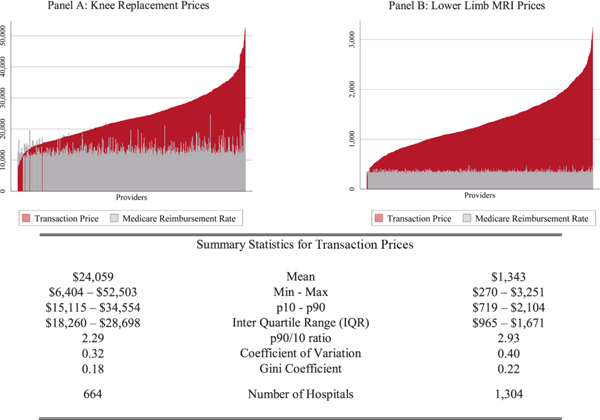

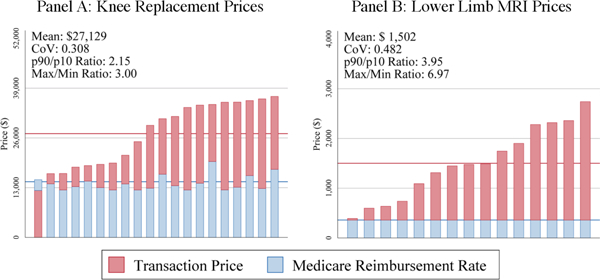

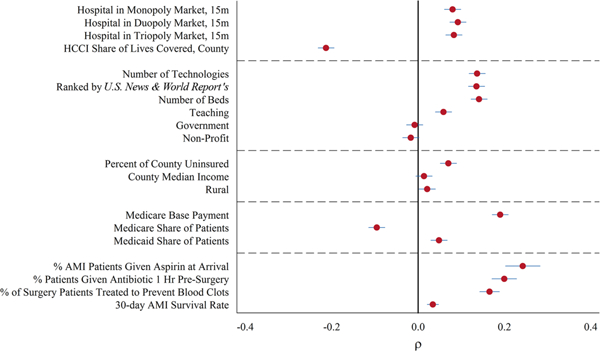

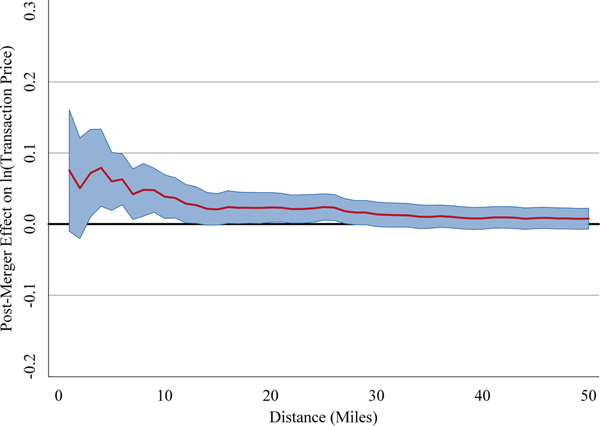

We use insurance claims data covering 28% of individuals with employer-sponsored health insurance in the United States to study the variation in health spending on the privately insured, examine the structure of insurer-hospital contracts, and analyze the variation in hospital prices across the nation. Health spending per privately insured beneficiary differs by a factor of three across geographic areas and has a very low correlation with Medicare spending. For the privately insured, half of the spending variation is driven by price variation across regions, and half is driven by quantity variation. Prices vary substantially across regions, across hospitals within regions, and even within hospitals. For example, even for a nearly homogeneous service such as lower-limb magnetic resonance imaging, about a fifth of the total case-level price variation occurs within a hospital in the cross section. Hospital market structure is strongly associated with price levels and contract structure. Prices at monopoly hospitals are 12% higher than those in markets with four or more rivals. Monopoly hospitals also have contracts that load more risk on insurers (e.g., they have more cases with prices set as a share of their charges). In concentrated insurer markets the opposite occurs-hospitals have lower prices and bear more financial risk. Examining the 366 mergers and acquisitions that occurred between 2007 and 2011, we find that prices increased by over 6% when the merging hospitals were geographically close (e.g., 5 miles or less apart), but not when the hospitals were geographically distant (e.g., over 25 miles apart).

Figures

References

-

- Ashenfelter Orley, Hosken Daniel, and Weinberg Matthew, “Did Robert Bork Understate the Competitive Impact of Mergers? Evidence from Consummated Mergers,” Journal of Law and Economics, 57 (2014), S67–S100.

-

- Bai Ge, and Anderson Gerard F., “Extreme Markup: The Fifty US Hospitals with the Highest Charge-To-Cost Ratios,” Health Affairs, 34 (2015), 922–928. - PubMed

-

- j/>Baker Laurence, M. Kate Bundorf, Aileen Devlin, and Daniel P. Kessler, “Why Don’t Commercial Health Plans Use Prospective Payment?,” NBER Working Paperseries No. 22709, 2016.

-

- Bloom Nick, Propper Carol, Seiler Stephan, and John Van Reenen, “The Impact of Competition on Management Quality: Evidence from Public Hospitals,” Review of Economic Studies, 82 (2015), 457–489.

-

- Bloom Nick, Lemos Renata, Raffaella sadun, and John Van Reenen, “Healthy Business? Managerial Education and Management in Healthcare,” Centre for Economic Performance Discussion Paper 1500, 2017.

Grants and funding

LinkOut - more resources

Full Text Sources