ADHD, financial distress, and suicide in adulthood: A population study

- PMID: 32998893

- PMCID: PMC7527218

- DOI: 10.1126/sciadv.aba1551

ADHD, financial distress, and suicide in adulthood: A population study

Abstract

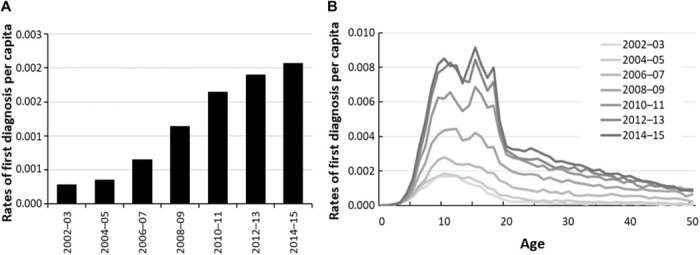

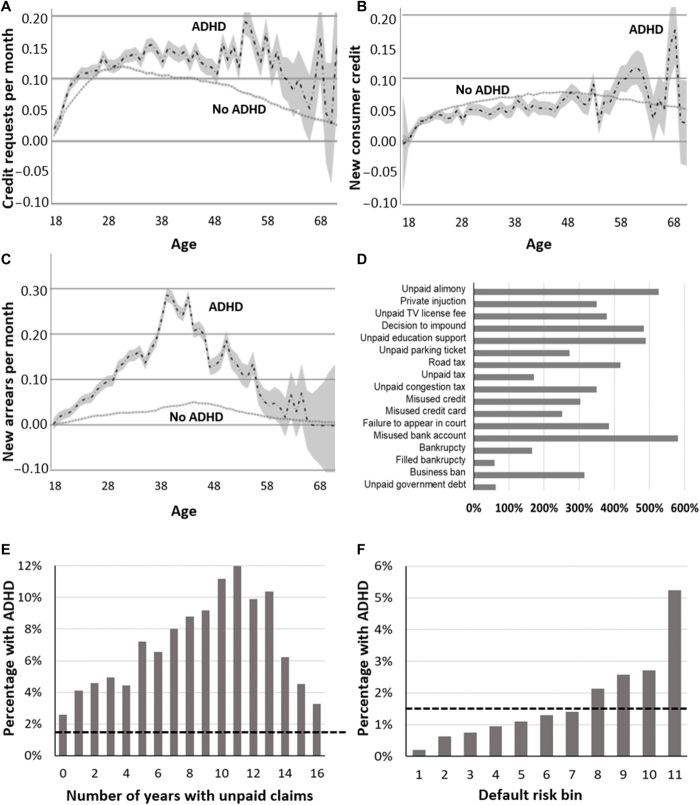

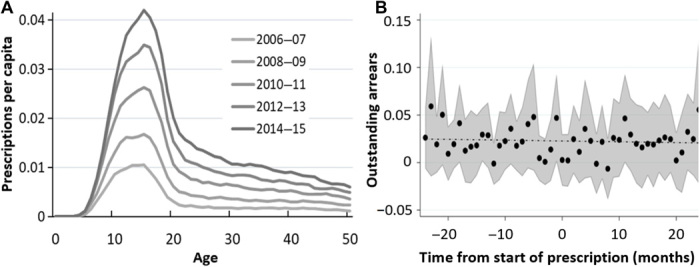

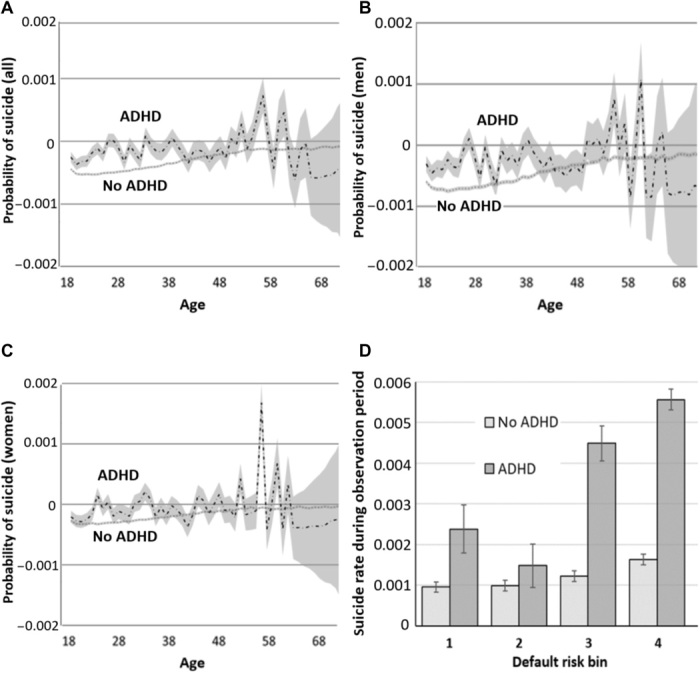

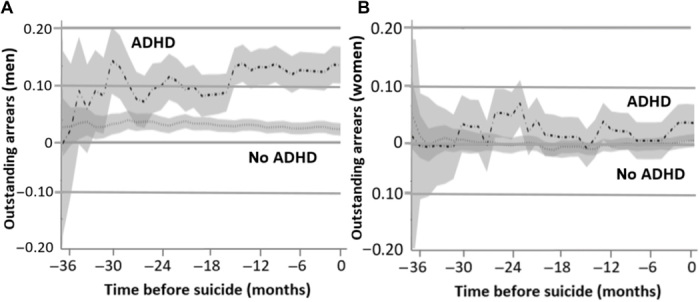

Attention-deficit/hyperactivity disorder (ADHD) exerts lifelong impairment, including difficulty sustaining employment, poor credit, and suicide risk. To date, however, studies have assessed selected samples, often via self-report. Using mental health data from the entire Swedish population (N = 11.55 million) and a random sample of credit data (N = 189,267), we provide the first study of objective financial outcomes among adults with ADHD, including associations with suicide. Controlling for psychiatric comorbidities, substance use, education, and income, those with ADHD start adulthood with normal credit demand and default rates. However, in middle age, their default rates grow exponentially, yielding poor credit scores and diminished credit access despite high demand. Sympathomimetic prescriptions are unassociated with improved financial behaviors. Last, financial distress is associated with fourfold higher risk of suicide among those with ADHD. For men but not women with ADHD who suicide, outstanding debt increases in the 3 years prior. No such pattern exists for others who suicide.

Copyright © 2020 The Authors, some rights reserved; exclusive licensee American Association for the Advancement of Science. No claim to original U.S. Government Works. Distributed under a Creative Commons Attribution NonCommercial License 4.0 (CC BY-NC).

Figures

References

-

- World Health Organization, ICD-10 Classification of Mental and Behavioural Disorders (Author, Geneva, Switzerland, 1992).

-

- Patros C. H. G., Alderson M., Kasper L. J., Tarle S. J., Lea S. E., Hudec K. L., Choice-impulsivity in children and adolescents with attention-deficit/hyperactivity disorder (ADHD): A meta-analytic review. Clin. Psychol. Rev. 43, 162–174 (2016). - PubMed

-

- Beauchaine T. P., Zisner A., Sauder C. L., Trait impulsivity and the externalizing spectrum. Annu. Rev. Clin. Psychol. 13, 343–368 (2017). - PubMed

-

- Loe I. M., Feldman H. M., Academic and educational outcomes of children with ADHD. J. Pediatr. Psychol. 32, 643–654 (2007). - PubMed

-

- Barkley R. A., Fischer M., Smallish L., Fletcher K., Young adult outcome of hyperactive children: Adaptive functioning in major life activities. J. Am. Acad. Child Adolesc. Psychiatry 45, 192–202 (2006). - PubMed

Publication types

MeSH terms

Grants and funding

LinkOut - more resources

Full Text Sources

Medical