Taxing capital and labor when both factors are imperfectly mobile internationally

- PMID: 33785985

- PMCID: PMC7993084

- DOI: 10.1007/s10797-021-09663-4

Taxing capital and labor when both factors are imperfectly mobile internationally

Abstract

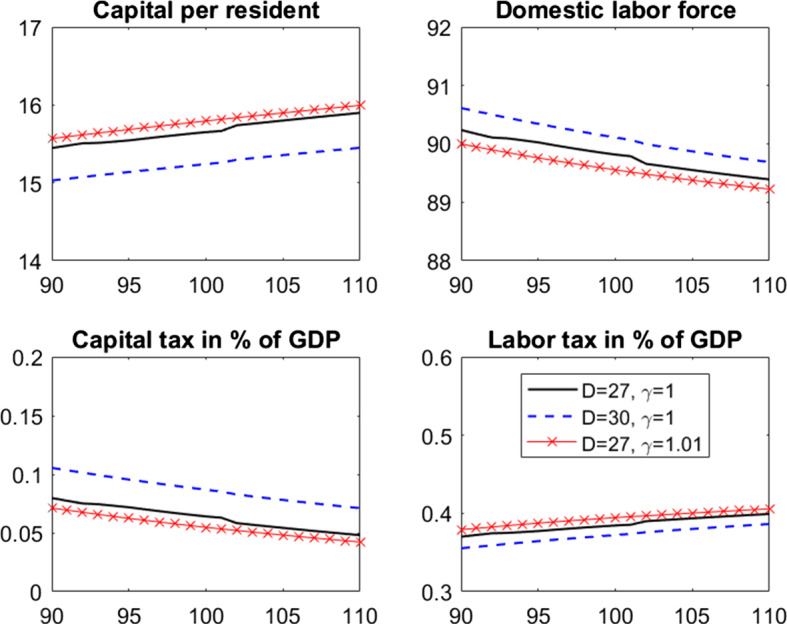

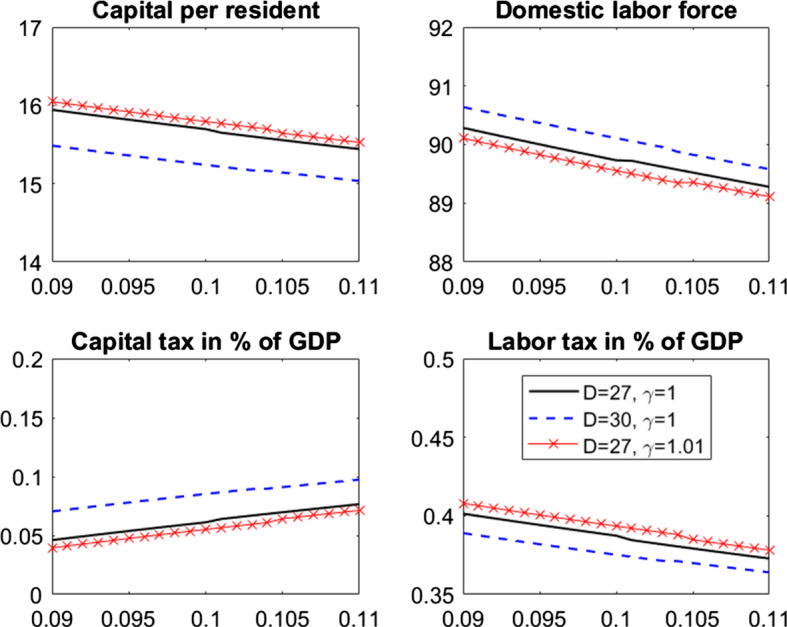

We revisit the standard theoretical model of tax competition to consider imperfect mobility of both capital and labor. We show that the mobility of one factor affects the taxation of both factors and that the "race-to-the-bottom" narrative (with burden shifting) applies essentially to capital-exporting countries. We validate our predictions using a panel of 29 OECD countries over the period of 1997-2017. The quantitative contribution of rising capital mobility to the decline of corporate income tax rates over our sample period is nonetheless less than that of population ageing.

Keywords: Globalization; Imperfect factor mobility; Tax competition.

© The Author(s), under exclusive licence to Springer Science+Business Media, LLC, part of Springer Nature 2021.

Figures

References

-

- Adam A, Kammas P. Tax policies in a globalized world: Is it politics after all? Public Choice. 2007;133:321–341. doi: 10.1007/s11127-007-9190-9. - DOI

-

- Adam A, Kammas P, Lagou A. The effect of globalization on capital taxation: What have we learned after 20 years of empirical studies? Journal of Macroeconomics. 2013;35:199–209. doi: 10.1016/j.jmacro.2012.09.003. - DOI

-

- Baldwin R. The great convergence, information technology and the new globalization. Harvard University Press; 2016.

-

- Baldwin R, Forslid R, Martin P, Ottaviano G, Robert-Nicoud F. Economic geography and public policy. Princeton University Press; 2003.

-

- Bilicka K, Devereux MP. CBT corporate tax ranking 2012. Saïd Business School; 2012.

LinkOut - more resources

Full Text Sources

Other Literature Sources