The legal feasibility of adopting a sugar-sweetened beverage tax in seven sub-Saharan African countries

- PMID: 33876700

- PMCID: PMC8078924

- DOI: 10.1080/16549716.2021.1884358

The legal feasibility of adopting a sugar-sweetened beverage tax in seven sub-Saharan African countries

Abstract

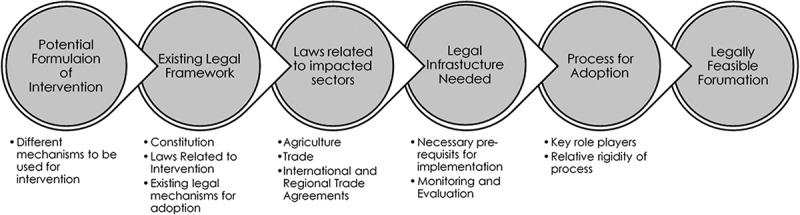

Background: A number of countries have adopted sugar-sweetened beverage taxes to prevent non-communicable diseases but there is variance in the structures and rates of the taxes. As interventions, sugar-sweetened beverage taxes could be cost-effective but must be compliant with existing legal and taxation systems.Objectives: To assess the legal feasibility of introducing or strengthening taxation laws related to sugar-sweetened beverages, for prevention of non-communicable diseases in seven countries: Botswana, Kenya, Namibia, Rwanda, Tanzania, Uganda and Zambia.Methods: We assessed the legal feasibility of adopting four types of sugar-sweetened beverage tax formulations in each of the seven countries, using the novel FELIP framework. We conducted a desk-based review of the legal system related to sugar-sweetened beverage taxation and assessed the barriers to, and facilitators and legal feasibility of, introducing each of the selected formulations by considering the existing laws, laws related to impacted sectors, legal infrastructure, and processes involved in adopting laws.Results: Six countries had legal mandates to prevent non-communicable diseases and protect the health of citizens. As of 2019, all countries had excise tax legislation. Five countries levied excise taxes on all soft drinks, but most did not exclusively target sugar-sweetened beverages, and taxation rates were well below the World Health Organization's recommended 20%. In Uganda and Kenya, agricultural or HIV-related levies offered alternative mechanisms to disincentivise consumption of sugar-sweetened beverages without the introduction of new taxes. Nutrition-labelling laws in all countries made it feasible to adopt taxes linked to the sugar content of beverages, but there were lacunas in existing infrastructure for more sophisticated taxation structures.Conclusion: Sugar-sweetened beverage taxes are legally feasible in all seven countries Existing laws provide a means to implement taxes as a public health intervention.

Keywords: NCD policy; Non-communicable diseases; fiscal policy; legal feasibility; sub-Saharan Africa.

Conflict of interest statement

The authors report no conflicts of interest.

Figures

References

-

- Nyirenda MJ. Non-communicable diseases in sub-Saharan Africa: understanding the drivers of the epidemic to inform intervention strategies. Int Health. 2016;8:157–17. - PubMed

-

- Mufunda J, Chatora R, Ndambakuwa Y, et al. Emerging non-communicable disease epidemic in Africa: preventive measures from the WHO regional office for Africa. Ethn Dis [Internet]. 2006. [cited 2017 October9];16:521–526. Available from: https://www.ethndis.org/priorarchives/ethn-16-02-521.pdf - PubMed

-

- Naghavi M, Forouzanfar MH. Burden of non-communicable diseases in sub-Saharan Africa in 1990 and 2010: Global Burden of Diseases, Injuries, and Risk Factors Study 2010. Lancet [Internet]. 2013. June 17 [cited 2021 January24];381:S95.Available from:] http://www.sciencedirect.com/science/article/pii/S0140673613613495

MeSH terms

LinkOut - more resources

Full Text Sources

Other Literature Sources

Research Materials