The predictive power of stock market's expectations volatility: A financial synchronization phenomenon

- PMID: 34014976

- PMCID: PMC8136682

- DOI: 10.1371/journal.pone.0250846

The predictive power of stock market's expectations volatility: A financial synchronization phenomenon

Abstract

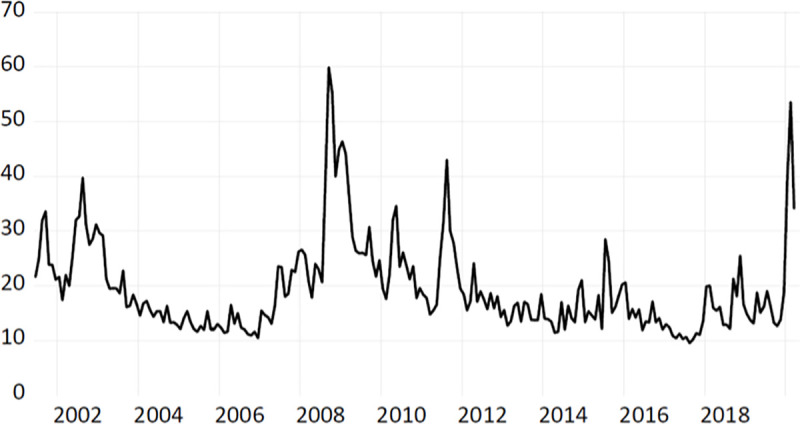

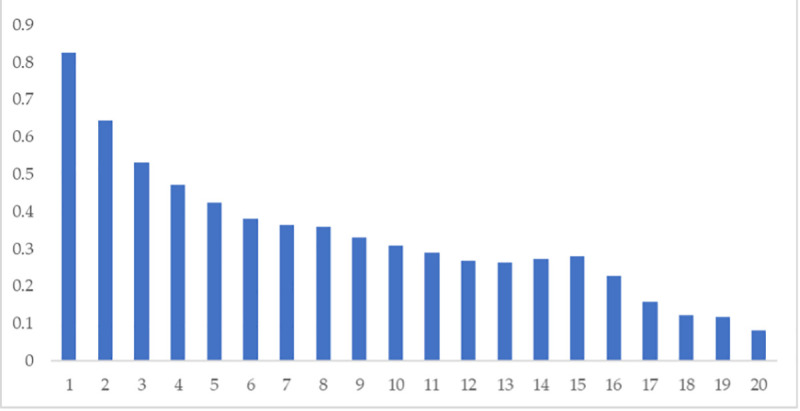

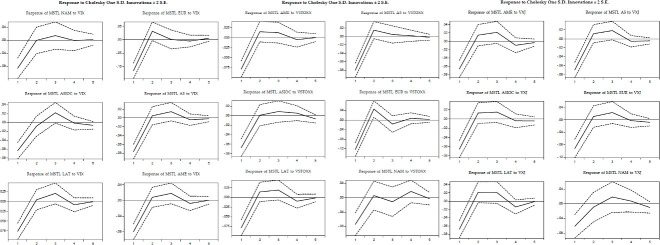

We explore the use of implied volatility indices as a tool for estimate changes in the synchronization of stock markets. Specifically, we assess the implied stock market's volatility indices' predictive power on synchronizing global equity indices returns. We built the correlation network of 26 stock indices and implemented in-sample and out-of-sample tests to evaluate the predictive power of VIX, VSTOXX, and VXJ implied volatility indices. To measure markets' synchronization, we use the Minimum Spanning Tree length and the length of the Planar Maximally Filtered Graph. Our results indicate a high predictive power of all the volatility indices, both individually and together, though the VIX predominates over the evaluated options. We find that an increase in the markets' volatility expectations, captured by the implied volatility indices, is a good Granger predictor of an increase in the synchronization of returns in the following month. Estimating, monitoring, and predicting returns' synchronization is essential for investment decision-making, especially for diversification strategies and regulating financial systems.

Conflict of interest statement

The authors have declared that no competing interests exist.

Figures

Similar articles

-

Relationship between uncertainty in the oil and stock markets before and after the shale gas revolution: Evidence from the OVX, VIX, and VKOSPI volatility indices.PLoS One. 2020 May 5;15(5):e0232508. doi: 10.1371/journal.pone.0232508. eCollection 2020. PLoS One. 2020. PMID: 32369536 Free PMC article. Review.

-

Which popular predictor is more useful to forecast international stock markets during the coronavirus pandemic: VIX vs EPU?Int Rev Financ Anal. 2020 Nov;72:101596. doi: 10.1016/j.irfa.2020.101596. Epub 2020 Sep 28. Int Rev Financ Anal. 2020. PMID: 38620312 Free PMC article.

-

Do implied volatilities of stock and commodity markets affect conventional & shariah indices differently? An evidence by OVX, GVZ and VIX.Heliyon. 2023 Oct 17;9(11):e21094. doi: 10.1016/j.heliyon.2023.e21094. eCollection 2023 Nov. Heliyon. 2023. PMID: 38027772 Free PMC article.

-

The predictive power of Bitcoin prices for the realized volatility of US stock sector returns.Financ Innov. 2023;9(1):62. doi: 10.1186/s40854-023-00464-8. Epub 2023 Mar 6. Financ Innov. 2023. PMID: 36911098 Free PMC article.

-

Time-frequency domain analysis of investor fear and expectations in stock markets of BRIC economies.Heliyon. 2021 Oct 19;7(10):e08211. doi: 10.1016/j.heliyon.2021.e08211. eCollection 2021 Oct. Heliyon. 2021. PMID: 34754971 Free PMC article. Review.

Cited by

-

Forecasting Commodity Market Synchronization with Commodity Currencies: A Network-Based Approach.Entropy (Basel). 2023 Mar 25;25(4):562. doi: 10.3390/e25040562. Entropy (Basel). 2023. PMID: 37190350 Free PMC article.

-

Equity Market Description under High and Low Volatility Regimes Using Maximum Entropy Pairwise Distribution.Entropy (Basel). 2021 Oct 5;23(10):1307. doi: 10.3390/e23101307. Entropy (Basel). 2021. PMID: 34682031 Free PMC article.

References

-

- Jach A. International stock market comovement in time and scale outlined with a thick pen. Journal of Empirical Finance. 2017;43: 115–129. 10.1016/j.jempfin.2017.06.004 - DOI

-

- Magner NS, Lavin JF, Valle MA, Hardy N. The Volatility Forecasting Power of Financial Network Analysis. Silva TC, editor. Complexity. 2020;2020: 1–17. 10.1155/2020/7051402 - DOI

Publication types

MeSH terms

LinkOut - more resources

Full Text Sources

Other Literature Sources