Harmonizing corporate carbon footprints

- PMID: 34686675

- PMCID: PMC8536701

- DOI: 10.1038/s41467-021-26349-x

Harmonizing corporate carbon footprints

Abstract

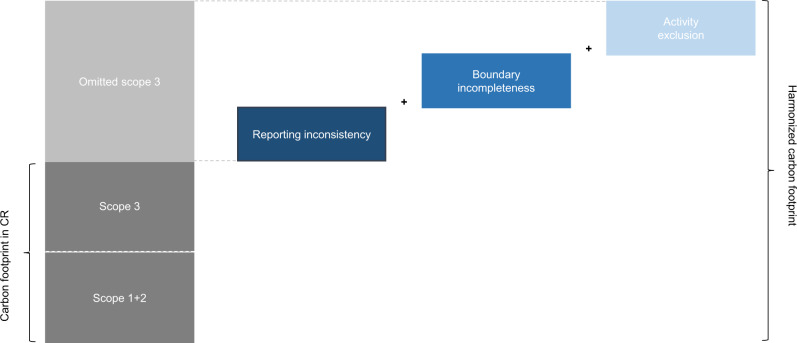

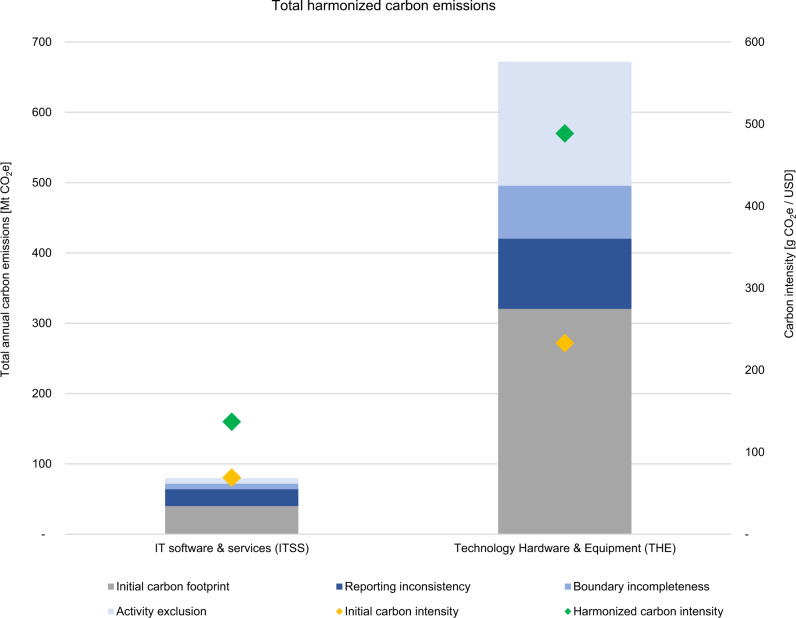

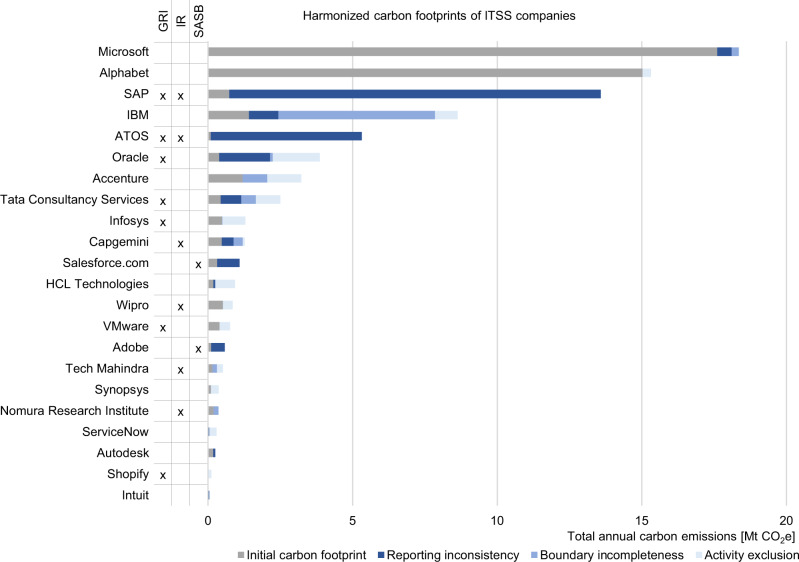

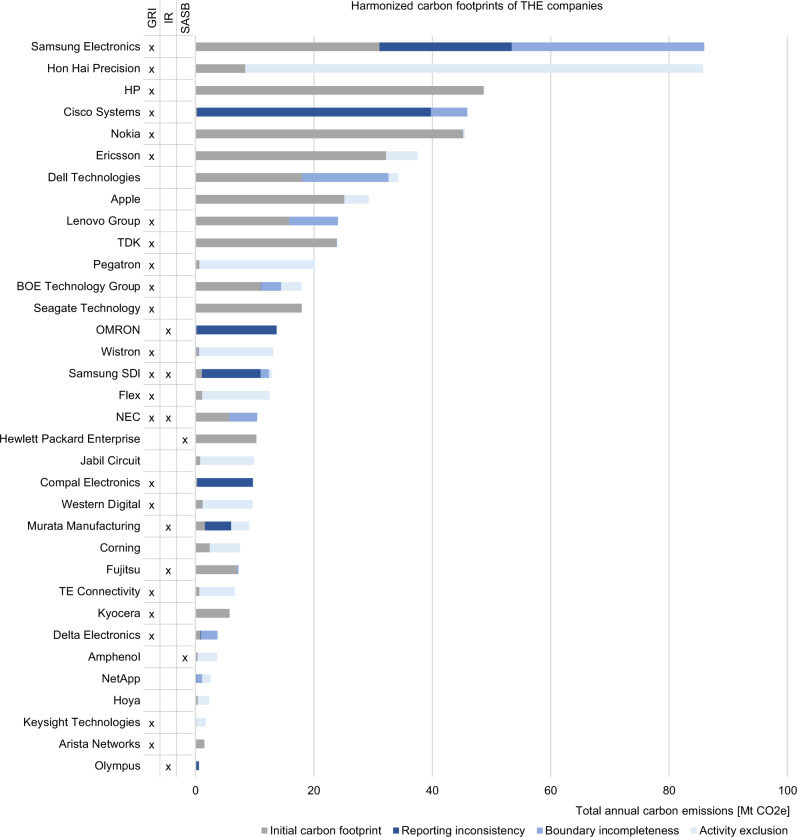

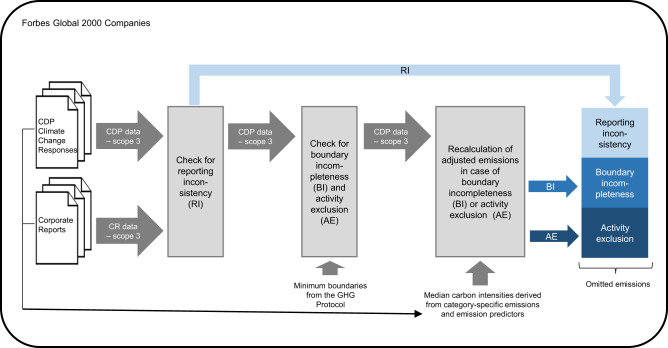

Global greenhouse gas emissions need to reach net-zero around mid-century to limit global warming to 1.5 °C. This decarbonization challenge has, inter alia, increased the political and societal pressure on companies to disclose their carbon footprints. As a response, numerous companies announced roadmaps to become carbon neutral or even negative. The first step on the journey towards carbon neutrality, however, is to quantify corporate emissions accurately. Current carbon accounting and reporting practices remain unsystematic and not comparable, particularly for emissions along the value chain (so-called scope 3). Here we present a framework to harmonize scope 3 emissions by accounting for reporting inconsistency, boundary incompleteness, and activity exclusion. In a case study of the tech sector, we find that corporate reports omit half of the total emissions. The framework we present may help companies, investors, and policy makers to identify and close the gaps in corporate carbon footprints.

© 2021. The Author(s).

Conflict of interest statement

The authors declare no competing interests.

Figures

References

-

- IPCC. Global Warming of 1.5 °C. Available at https://www.ipcc.ch/sr15/ (2018).

-

- Deloitte. Sustainability Disclosure Goes Mainstream. Available at https://www2.deloitte.com/us/en/pages/audit/articles/hu-sustainability-d... (2020).

-

- Amazon. Sustainability: Thinking Big. Available at https://sustainability.aboutamazon.com/ (2019).

-

- Apple. Apple commits to carbon neutrality for supply chain and products by 2030. Available at https://www.apple.com/newsroom/2020/07/apple-commits-to-be-100-percent-c... (2020).

-

- Microsoft. Microsoft Will Be Carbon Negative by 2030. Available at https://www.https://blogs.microsoft.com/blog/2020/01/16/microsoft-will-b... (2020).

LinkOut - more resources

Full Text Sources