COVID-19 media coverage and ESG leader indices

- PMID: 35221818

- PMCID: PMC8856890

- DOI: 10.1016/j.frl.2021.102170

COVID-19 media coverage and ESG leader indices

Abstract

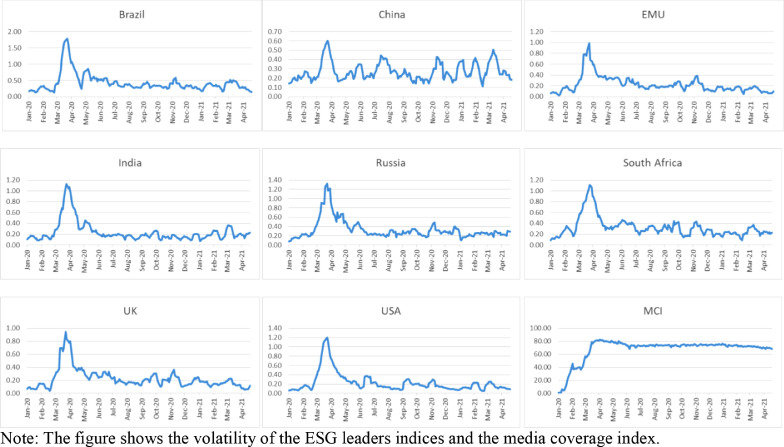

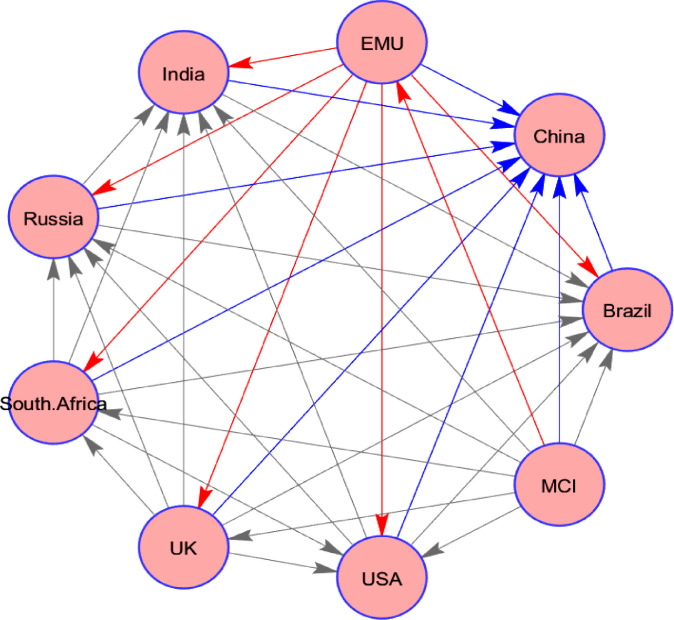

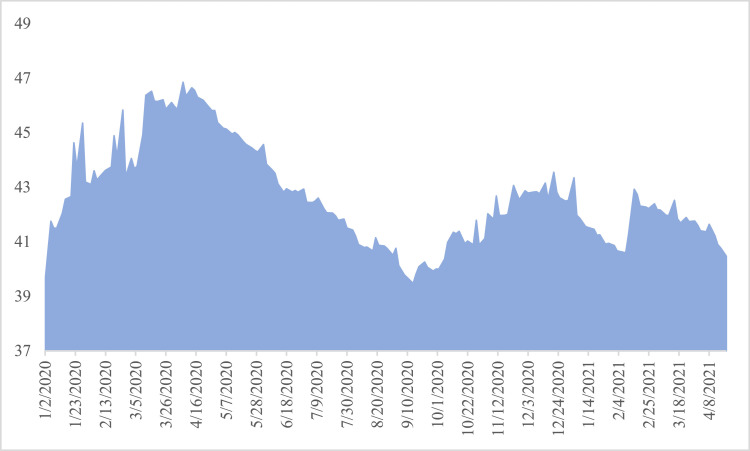

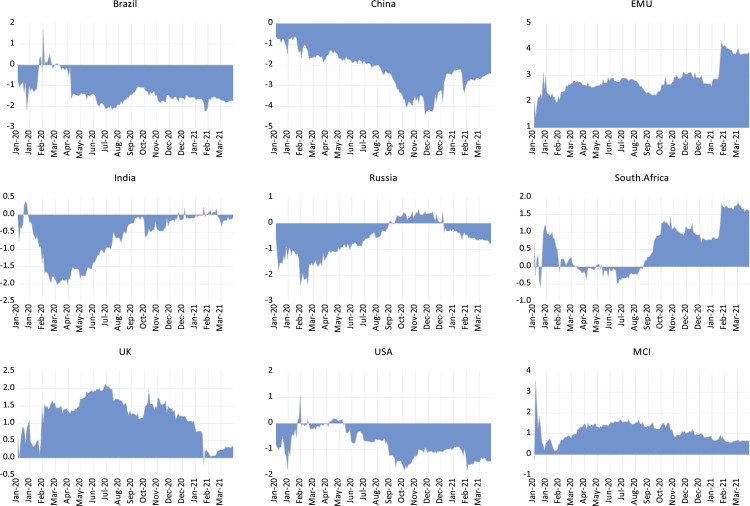

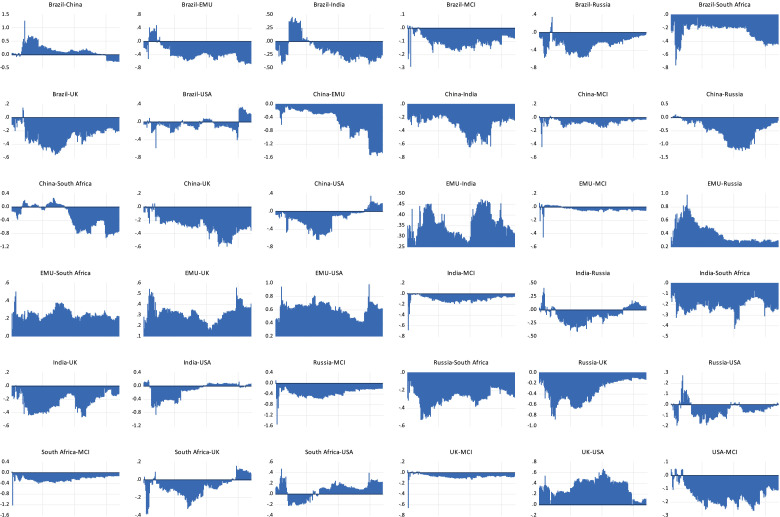

This study examines the dynamic connectedness between COVID-19 media coverage index (MCI) and ESG leader indices. Our findings provide evidence that MCI plays a role in facilitating the transmission of contagion to advanced and emerging equity markets during the pandemic. The connectedness between MCI and ESG leader indices is more pronounced around March and April 2020 at the peak of the pandemic. The US is a net receiver of shocks reaffirming that it was the most affected country during the pandemic. Our results provide implications for investors, portfolio managers, and policymakers in mitigating financial risks during the pandemic.

Keywords: COVID–19; ESG leaders; Financial contagion; Media coverage index; TVP–VAR.

© 2021 Elsevier Inc. All rights reserved.

Figures

Similar articles

-

Dynamic connectedness between stock markets in the presence of the COVID-19 pandemic: does economic policy uncertainty matter?Financ Innov. 2021;7(1):13. doi: 10.1186/s40854-021-00227-3. Epub 2021 Mar 1. Financ Innov. 2021. PMID: 35024274 Free PMC article.

-

How COVID-19 drives connectedness among commodity and financial markets: Evidence from TVP-VAR and causality-in-quantiles techniques.Resour Policy. 2021 Mar;70:101898. doi: 10.1016/j.resourpol.2020.101898. Epub 2020 Oct 20. Resour Policy. 2021. PMID: 34173426 Free PMC article.

-

The static and dynamic connectedness of environmental, social, and governance investments: International evidence.Econ Model. 2020 Dec;93:112-124. doi: 10.1016/j.econmod.2020.08.007. Epub 2020 Aug 12. Econ Model. 2020. PMID: 32834335 Free PMC article.

-

Return connectedness among commodity and financial assets during the COVID-19 pandemic: Evidence from China and the US.Resour Policy. 2021 Oct;73:102166. doi: 10.1016/j.resourpol.2021.102166. Epub 2021 Jun 6. Resour Policy. 2021. PMID: 34539034 Free PMC article.

-

Comparing asymmetric price efficiency in regional ESG markets before and during COVID-19.Econ Model. 2023 Jan;118:106095. doi: 10.1016/j.econmod.2022.106095. Epub 2022 Oct 28. Econ Model. 2023. PMID: 36341042 Free PMC article.

Cited by

-

Machine learning sentiment analysis, COVID-19 news and stock market reactions.Res Int Bus Finance. 2023 Jan;64:101881. doi: 10.1016/j.ribaf.2023.101881. Epub 2023 Jan 16. Res Int Bus Finance. 2023. PMID: 36687319 Free PMC article.

-

Corporate social responsibility budgeting and spending during COVID-19 in Oman: A humanitarian response to the pandemic.Financ Res Lett. 2022 Jun;47:102686. doi: 10.1016/j.frl.2022.102686. Epub 2022 Jan 11. Financ Res Lett. 2022. PMID: 35035308 Free PMC article.

-

Examining the hedge performance of US dollar, VIX, and gold during the coronavirus pandemic: Is US dollar a better hedge asset?PLoS One. 2023 Oct 5;18(10):e0291684. doi: 10.1371/journal.pone.0291684. eCollection 2023. PLoS One. 2023. PMID: 37796831 Free PMC article.

-

Corporate vulnerability in the US and China during COVID-19: A machine learning approach.J Econ Asymmetries. 2023 Jun;27:e00302. doi: 10.1016/j.jeca.2023.e00302. Epub 2023 Apr 10. J Econ Asymmetries. 2023. PMID: 37089460 Free PMC article.

-

The Return and Volatility Connectedness of NFT Segments and Media Coverage: Fresh Evidence Based on News About the COVID-19 Pandemic.Financ Res Lett. 2022 Oct;49:103031. doi: 10.1016/j.frl.2022.103031. Epub 2022 Jun 2. Financ Res Lett. 2022. PMID: 35669177 Free PMC article.

References

-

- Akhtaruzzaman, M., Boubaker, S., Lucey, B. M., & Sensoy, A. (2021b). Is gold a hedge or safe haven asset during COVID19 crisis?. Economic Modelling (Forthcoming).

-

- Antonakakis, N., & Gabauer, D. (2017). Refined measures of dynamic connectedness based on TVP-VAR, retrieved from https://mpra.ub.uni-muenchen.de/id/eprint/78282.

LinkOut - more resources

Full Text Sources

Miscellaneous