The relationship between global stock and precious metals under Covid-19 and happiness perspectives

- PMID: 35308300

- PMCID: PMC8919855

- DOI: 10.1016/j.resourpol.2022.102634

The relationship between global stock and precious metals under Covid-19 and happiness perspectives

Abstract

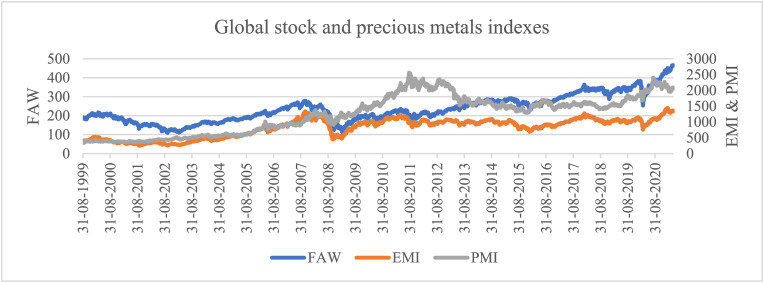

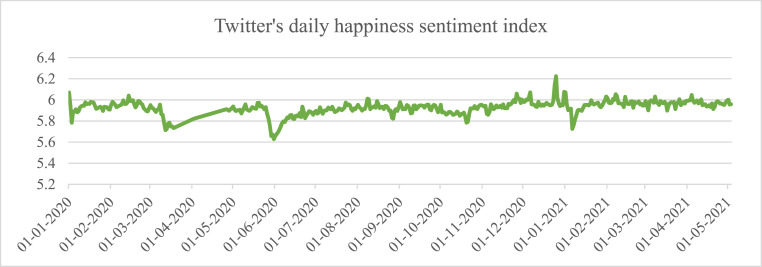

In this paper, we examine the relationship between global stock markets, as respectively represented by the FTSE All-World Series and the MSCI Emerging Markets indexes, and the S&P GSCI Precious Metals index from 01 September 1999 to 03 May 2021. We employ the conditional correlation multivariate generalized autoregressive conditional heteroskedasticity (MGARCH) to investigate this stock-precious metals nexus in terms of return and volatility spillovers. The study assesses impacts of the Covid-19 pandemic on the stock-precious metals nexus and further examine this relationship by supplementing the Twitter's Daily Happiness Sentiment index to the methodological framework for the period from 01 January 2020 to 03 May 2021. We find that precious metals positively influence stock markets before the Covid-19 outbreak and firmly play a valuable role due to their hedge and safe haven characteristics. In contrast, the bivariate GARCH framework does not provide statistically significant evidence on the stock-precious metals nexus during the Covid-19 pandemic. Meanwhile, the tri-variate GARCH approach with stock markets, precious metals, and happiness sentiment indexes reveals sufficiently complicated interactions between these return series. Prominently, past change in the happiness index negatively affects the stock returns but positively drives the performance of precious metals. These findings indirectly demonstrate the stock-precious metals nexus under impacts of the Covid-19 pandemic and reflect the demand of precious metals during crisis periods. Accordingly, we suggest a reasonable method of adjusting the proxies when no interaction effect is significantly found during unprecedented outbreaks.

Keywords: Covid-19; Emerging stock index; Global happiness; Global stock index; Precious metals index.

© 2022 Elsevier Ltd. All rights reserved.

Figures

References

-

- Alharthi M., Alamoudi H., Shaikh A.A., Bhutto M.H. Your ride has arrived”–Exploring the nexus between subjective well-being, socio-cultural beliefs, COVID-19, and the sharing economy. Telematics Inf. 2021;63:101663.

-

- Ali S., Bouri E., Czudaj R.L., Hussain Shahzad S.J. Revisiting the valuable roles of commodities for international stock markets. Resour. Pol. 2020;66:101603.

-

- Arouri M.E., Jouini J., Nguyen D.K. Volatility spillovers between oil prices and stock sector returns: implications for portfolio management. J. Int. Money Finance. 2011;30(7):1387–1405.

LinkOut - more resources

Full Text Sources

Miscellaneous