Would A National Sugar-Sweetened Beverage Tax In The United States Be Well Targeted?

- PMID: 35505903

- PMCID: PMC9060537

- DOI: 10.1111/ajae.12190

Would A National Sugar-Sweetened Beverage Tax In The United States Be Well Targeted?

Abstract

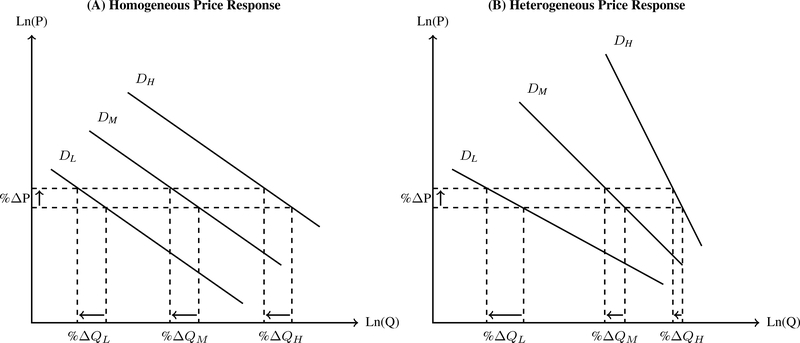

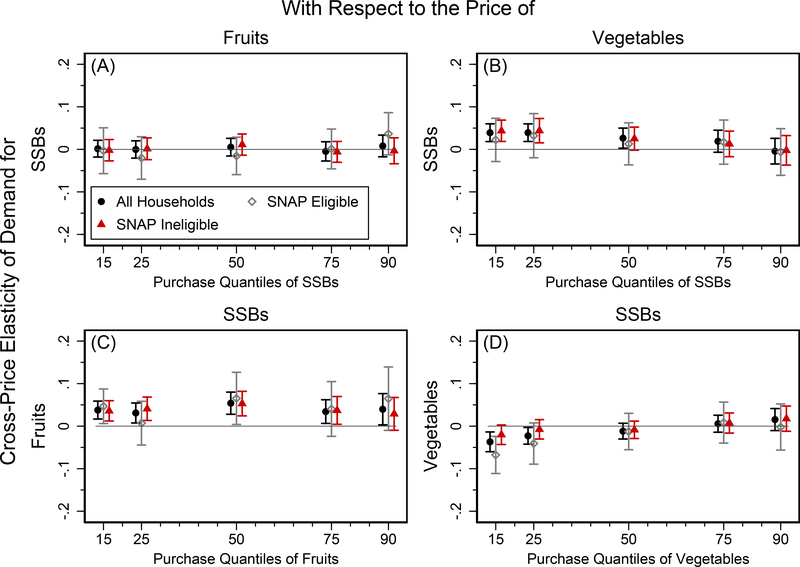

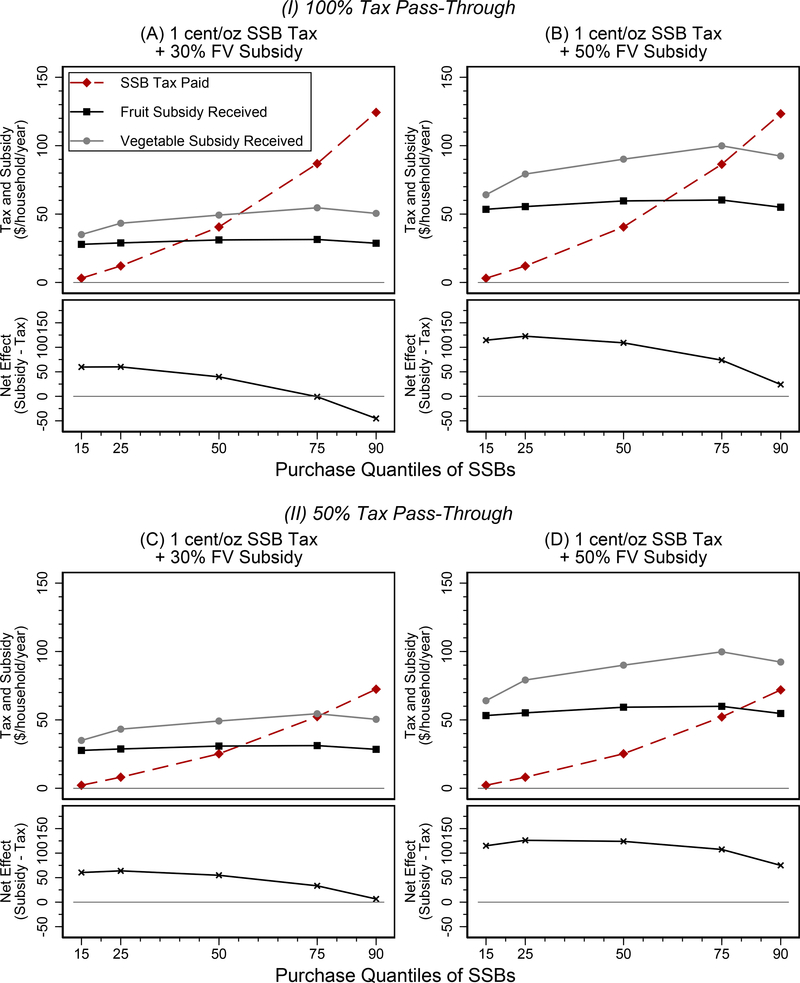

Sugar-sweetened beverage (SSB) taxes have been proposed to discourage excessive sugar consumption, but it is unclear how high- vs. low-SSB purchasers respond to such taxes. We first examine heterogeneity in the purchase and financial effects of a national SSB tax across different types of households buying varying amounts of SSBs. We find high-SSB purchasers are less responsive to SSB price changes than low purchasers but make larger absolute reductions in SSB purchases in response to the tax, given their notably greater purchase levels prior to the tax. Nonetheless, the economic burden of the tax falls more heavily on high-SSB purchasers who are more likely comprised of lower-income households. We then investigate whether the income regressivity of the tax will be mitigated if low-income households are targeted by fruit and vegetable (FV) subsidies. We show that depending on the tax pass-through and subsidy rates, FV subsidies can fully offset high-SSB purchasers' tax burdens, and subsidy transfers are distributed relatively uniformly across the SSB purchase distribution of low-income households. Therefore, FV subsidy transfers would be financially more beneficial to low- and moderate-SSB purchasers because they bear smaller shares of the tax burden than high-SSB purchasers.

Keywords: C21; C33; D12; SSB tax; fruit and vegetable subsidies; heterogeneity; panel data; price elasticity; quantile regression.

Figures

References

-

- Abrevaya J 2013. “The Projection Approach for Unbalanced Panel Data.” The Econometrics Journal 16:161–178.

-

- Abrevaya J, and Dahl CM. 2008. “The Effects of Birth Inputs on Birthweight: Evidence from Quantile Estimation on Panel Data.” Journal of Business & Economic Statistics 26:379–397.

-

- Allcott H, Lockwood BB, and Taubinsky D. 2019a. “Regressive Sin Taxes, with An Application to the Optimal Soda Tax.” The Quarterly Journal of Economics 134:1557–1626.

-

- —. 2019b. “Should We Tax Sugar-Sweetened Beverages? An Overview of Theory and Evidence.” Journal of Economic Perspectives 33(3):202–27.

Grants and funding

LinkOut - more resources

Full Text Sources