Reward Salience and Choice in a Controlling Context: A Lab Experiment

- PMID: 35548550

- PMCID: PMC9083268

- DOI: 10.3389/fpsyg.2022.862152

Reward Salience and Choice in a Controlling Context: A Lab Experiment

Abstract

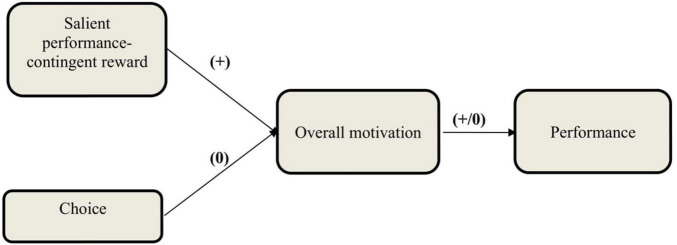

One of the challenges in the motivation literature is examining the simultaneous effect of different motivational mechanisms on overall motivation and performance. The motivational congruence theory addresses this by stipulating that different motivational mechanisms can reinforce each other if they have similar effects on the perceived locus of causality. Reward salience and choice are two motivational mechanisms which their joint effects have been long debated. Built upon the motivational congruence effect, a recent empirical study affirms that a salient reward in a condition characterized by lack of choice and a non-salient reward in a condition characterized by provision of choice both increase overall motivation and performance. In this study, we examine the effect of reward salience and choice on overall motivation and performance in a controlling context, an effect which has not been studied before. A 2 (choice: present, absent) × 3 (reward: salient, non-salient, none) factorial design was conducted to examine research hypotheses. The results show that under controlling conditions, salient reward improves overall motivation and performance compared to non-salient and no-reward conditions.

Keywords: choice; motivation; performance; performance-contingent reward; reward salience.

Copyright © 2022 Hendijani and Steel.

Conflict of interest statement

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Figures

References

-

- Ackerman P. L. (1987). Individual differences in skill learning: an integration of psychometric and information processing perspectives. Psychol. Bull. 102 3–27. 10.1037/0033-2909.102.1.3 - DOI

-

- Amabile T. M., DeJong W., Lepper M. R. (1976). Effects of externally imposed deadlines on subsequent intrinsic motivation. J. Pers. Soc. Psychol. 34 92–98. 10.1037/0022-3514.34.1.92 - DOI

-

- Argyris C. (1957). The individual and organization: some problems of mutual adjustment. Adm. Sci. Q. 2 1–24. 10.2307/2390587 - DOI

-

- Atkinson A. A., Banker R., Kaplan R. S., Young S. M. (2001). Management Accounting, 3rd Edn. Upper Saddle River, NJ: Prentice-Hall.

LinkOut - more resources

Full Text Sources

Miscellaneous