Understanding how ESG-focused airlines reduce the impact of the COVID-19 pandemic on stock returns

- PMID: 35599747

- PMCID: PMC9108034

- DOI: 10.1016/j.jairtraman.2022.102229

Understanding how ESG-focused airlines reduce the impact of the COVID-19 pandemic on stock returns

Abstract

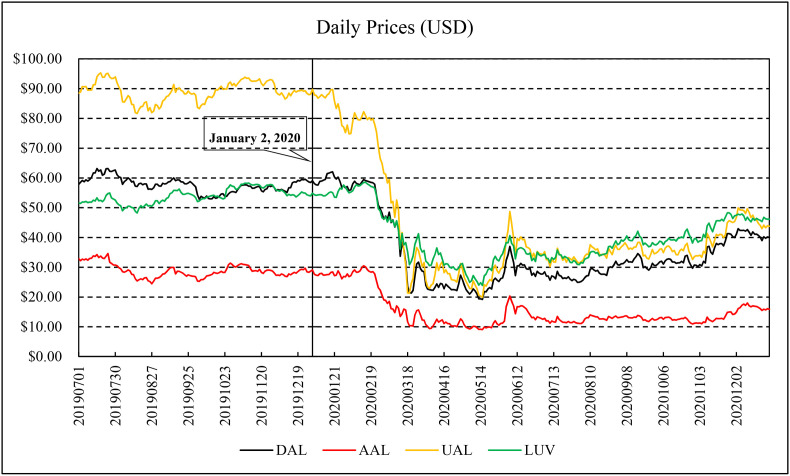

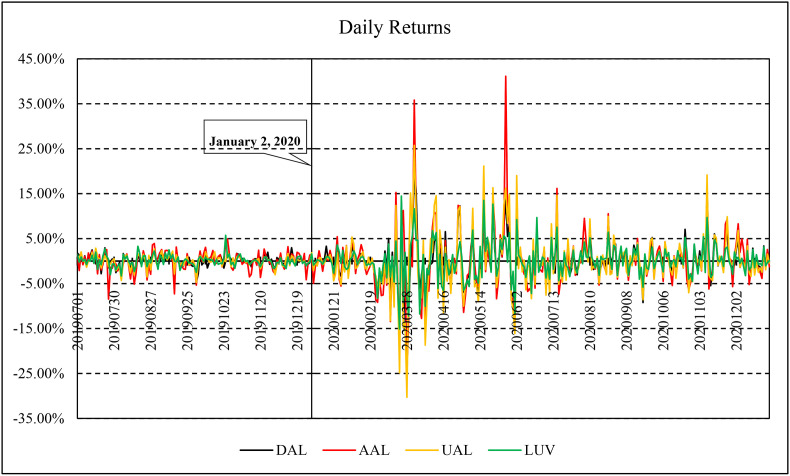

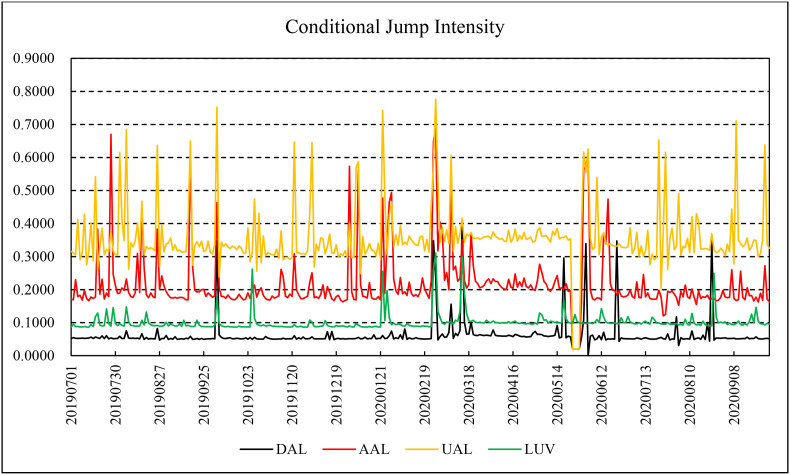

Incorporating environmental-social-governance (ESG) into a company's operations is an innovation strategy for contemporary businesses and a countermeasure for airline companies under COVID-19's influence. This research employs an autoregressive jump intensity trend (ARJI-trend) model to analyze the effects of COVID-19 and ESG ratings on the stock performance of the U.S. airline industry. We find that the ARJI-trend model captures the short- and long-run impacts of COVID-19 and ESG on stock return dynamics. Moreover, short-run stock return volatility converges to the original equilibrium level faster when a company has a higher ESG score, implying that promoting ESG does offer a defense mechanism to airline companies and that ESG performance is suitable for integration into business operational goals. The results lay the groundwork for understanding how an ESG focus might help airline companies to suffer less of an economic/financial impact during crises such as the COVID-19 pandemic.

Keywords: Autoregressive jump intensity trend model; COVID-19; ESG; Environmental-social-governance; Risk management.

© 2022 Elsevier Ltd. All rights reserved.

Figures

References

-

- Adrian T., Rosenberg J. Stock returns and volatility: pricing the short-run and long-run components of market risk. J. Finance. 2008;63(6):2997–3030.

-

- Andersen T.G. Return volatility and trading volume: an information flow interpretation of stochastic volatility. J. Finance. 1996;51:169–204.

-

- Andersen T.G., Bollerslev T., Diebold F.X. Roughing it up: including jump components in the measurement, modeling, and forecasting of return volatility. Rev. Econ. Stat. 2007;89(4):701–720.

-

- Bai J., Perron P. Estimating and testing linear models with multiple structural changes. Econometrica. 1998;66(1):47–78.

-

- Bai J., Perron P. Computation and analysis of multiple structural change models. J. Appl. Econom. 2003;18(1):1–22.

LinkOut - more resources

Full Text Sources