Are ESG-committed hotels financially resilient to the COVID-19 pandemic? An autoregressive jump intensity trend model

- PMID: 35693760

- PMCID: PMC9167863

- DOI: 10.1016/j.tourman.2022.104581

Are ESG-committed hotels financially resilient to the COVID-19 pandemic? An autoregressive jump intensity trend model

Abstract

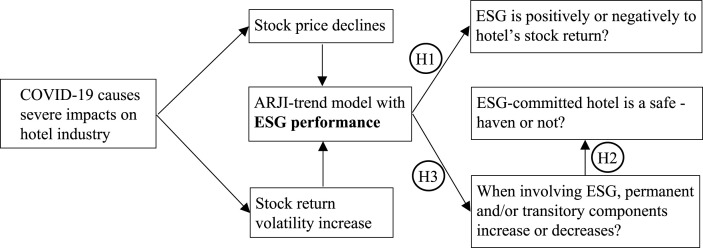

Given that the United Nations views environmental, social, and governance (ESG) as a practical framework for anchoring responsible corporate behavior to achieve its sustainable development goals, this study constructs an autoregressive jump intensity trend (ARJI-trend) model to determine if ESG can improve future resilience and create crisis-resilient value for chained-brand hotel corporations from the effects of COVID-19. The findings indicate that the ARJI-trend model indeed captures both the permanent and transitory components of the hotel corporation's ESG performance related to stock return dynamics. When ESG rating is taken into account, the following conclusions emerge: 1) the transitory component of time-varying return variance decreases but the permanent component does not; 2) the hotel corporation portfolios with a lower transitory component experiences a higher return, implying that the hotel corporations with a higher ESG rating appear to be more defensiveness; and 3) with proper asset reallocation, a portfolio centered on strong ESG-conscious hotel corporations is a safe-haven asset during market turmoil.

Keywords: Autoregressive jump intensity trend model; COVID-19; ESG; Environmental-social-governance; Hotel industry; Risk management.

© 2022 Elsevier Ltd. All rights reserved.

Conflict of interest statement

The author(s) declared no potential conflicts of interest with respect to the research.

Figures

References

-

- Adrian T., Rosenberg J. Stock returns and volatility: Pricing the short‐run and long-run components of market risk. The Journal of Finance. 2008;63(6):2997–3030.

-

- Andersen T.G., Bollerslev T., Diebold F.X. Roughing it up: Including jump components in the measurement, modeling, and forecasting of return volatility. The Review of Economics and Statistics. 2007;89(4):701–720.

-

- Bai J., Perron P. Estimating and testing linear models with multiple structural changes. Econometrica. 1998;66(1):47–78.

-

- Bai J., Perron P. Computation and analysis of multiple structural change models. Journal of Applied Econometrics. 2003;18(1):1–22.

-

- Bégin J.F., Dorion C., Gauthier G. Idiosyncratic jump risk matters: Evidence from equity returns and options. Review of Financial Studies. 2020;33(1):155–211.

LinkOut - more resources

Full Text Sources