Application of Genetic Optimization Algorithm in Financial Portfolio Problem

- PMID: 35875786

- PMCID: PMC9307338

- DOI: 10.1155/2022/5246309

Application of Genetic Optimization Algorithm in Financial Portfolio Problem

Abstract

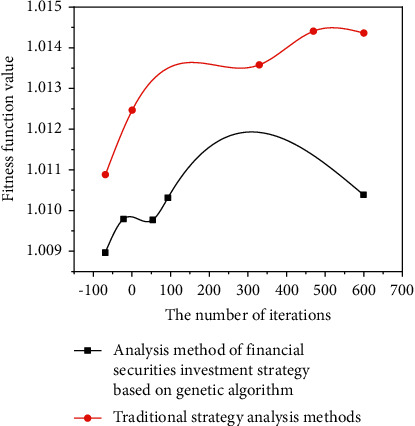

In order to address the application of genetic optimization algorithms to financial investment portfolio issues, the optimal allocation rate must be high and the risk is low. This paper uses quadratic programming algorithms and genetic algorithms as well as quadratic programming algorithms, Matlab planning solutions for genetic algorithms, and genetic algorithm toolboxes to solve Markowitz's mean variance model. The mathematical model for introducing sparse portfolio strategies uses the decomposition method of penalty functions as an algorithm for solving nonconvex sparse optimization strategies to solve financial portfolio problems. The merging speed of the quadratic programming algorithm is fast, and the merging speed depends on the selection of the initial value. The genetic algorithm performs very well in global searches, but local search capabilities are insufficient and the pace of integration into the next stage is slow. To solve this, using a genetic algorithm toolbox is quick and easy. The results of the experiments show that the final solution of the decomposition method of the fine function is consistent with the solution of the integrity of the genetic algorithm. 67% of the total funds will be spent on local car reserves and 33% on wine reserves. When data scales are small, quadratic programming algorithms and genetic algorithms can provide effective portfolio feedback, and the method of breaking down penalty functions to ensure the reliability and effectiveness of algorithm combinations is widely used in sparse financial portfolio issues.

Copyright © 2022 He Li and Naiyu Shi.

Conflict of interest statement

The authors declare that there are no conflicts of interest.

Figures

References

-

- Moshrefi M., Behnamian J. Multi-objective portfolio optimization by analytic hierarchy process and genetic algorithm. Soft Computing . 2019;5(1):61–80.

-

- Michell K., Kristjanpoller W. Strongly-typed genetic programming and fuzzy inference system: an embedded approach to model and generate trading rules. Applied Soft Computing . 2020;90(1) doi: 10.1016/j.asoc.2020.106169.106169 - DOI

-

- Michell K., Kristjanpoller W. Generating trading rules on us stock market using strongly typed genetic programming. Soft Computing . 2020;24(5):3257–3274. doi: 10.1007/s00500-019-04085-1. - DOI

-

- Jung W. The needs of incentives on long-term listed stock’s capital gains tax in planned financial investment gains taxation. Seoul Tax Law Review . 2021;27(1):325–362. doi: 10.16974/stlr.2021.27.1.008. - DOI

MeSH terms

LinkOut - more resources

Full Text Sources