Sparse and risk diversification portfolio selection

- PMID: 35936868

- PMCID: PMC9340743

- DOI: 10.1007/s11590-022-01914-5

Sparse and risk diversification portfolio selection

Abstract

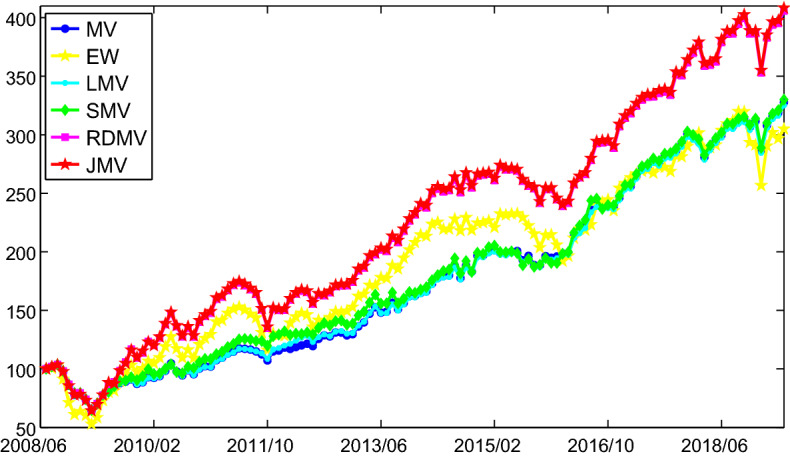

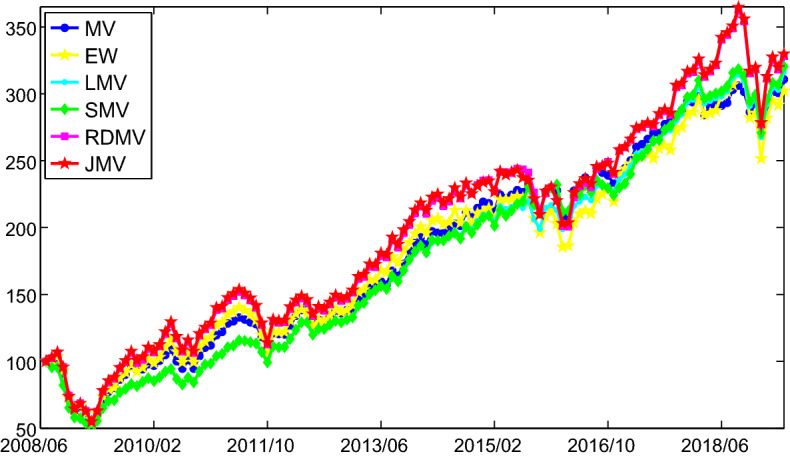

Portfolio risk management has become more important since some unpredictable factors, such as the 2008 financial crisis and the recent COVID-19 crisis. Although the risk can be actively managed by risk diversification, the high transaction cost and managerial concerns ensue by over diversifying portfolio risk. In this paper, we jointly integrate risk diversification and sparse asset selection into mean-variance portfolio framework, and propose an optimal portfolio selection model labeled as JMV. The weighted piecewise quadratic approximation is considered as a penalty promoting sparsity for the asset selection. The variance associated with the marginal risk regard as another penalty term to diversify the risk. By exposing the feature of JMV, we prove that the KKT point of JMV is the local minimizer if the regularization parameter satisfies a mild condition. To solve this model, we introduce the accelerated proximal gradient (APG) algorithm [Wen in SIAM J. Optim 27:124-145, 2017], which is one of the most efficient first-order large-scale algorithm. Meanwhile, the APG algorithm is linearly convergent to a local minimizer of the JMV model. Furthermore, empirical analysis consistently demonstrate the theoretical results and the superiority of the JMV model.

Keywords: Accelerated proximal algorithm; Linear convergence; Non-convex regularization; Sparse portfolio selection.

© The Author(s), under exclusive licence to Springer-Verlag GmbH Germany, part of Springer Nature 2022, Springer Nature or its licensor holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

Figures

Similar articles

-

Application of Genetic Optimization Algorithm in Financial Portfolio Problem.Comput Intell Neurosci. 2022 Jul 15;2022:5246309. doi: 10.1155/2022/5246309. eCollection 2022. Comput Intell Neurosci. 2022. PMID: 35875786 Free PMC article.

-

Cardinality Constrained Portfolio Optimization via Alternating Direction Method of Multipliers.IEEE Trans Neural Netw Learn Syst. 2024 Feb;35(2):2901-2909. doi: 10.1109/TNNLS.2022.3192065. Epub 2024 Feb 5. IEEE Trans Neural Netw Learn Syst. 2024. PMID: 35895648

-

Discriminative Feature Selection via Employing Smooth and Robust Hinge Loss.IEEE Trans Neural Netw Learn Syst. 2019 Mar;30(3):788-802. doi: 10.1109/TNNLS.2018.2852297. Epub 2018 Jul 26. IEEE Trans Neural Netw Learn Syst. 2019. PMID: 30047911

-

Convex compressive beamforming with nonconvex sparse regularization.J Acoust Soc Am. 2021 Feb;149(2):1125. doi: 10.1121/10.0003373. J Acoust Soc Am. 2021. PMID: 33639805

-

Big Data Challenges of High-Dimensional Continuous-Time Mean-Variance Portfolio Selection and a Remedy.Risk Anal. 2017 Aug;37(8):1532-1549. doi: 10.1111/risa.12801. Epub 2017 Mar 30. Risk Anal. 2017. PMID: 28370082

References

-

- Beck A, Teboulle M. A fast iterative shrinkage-thresholding algorithm for linear inverse problems. SIAM J. Imaging Sci. 2009;2:183–202. doi: 10.1137/080716542. - DOI

-

- Candès EJ, Wakin MB, Boyd SP. Enhancing sparsity by reweighted minimization. J. Fourier Anal. Appl. 2008;14(5):877–905. doi: 10.1007/s00041-008-9045-x. - DOI

-

- Chartrand R. Exact reconstruction of sparse signals via nonconvex minimization. IEEE Signal Process Lett. 2007;14(10):707–710. doi: 10.1109/LSP.2007.898300. - DOI

-

- Chartrand R, Staneva V. Restricted isometry properties and nonconvex compressive sensing. Inverse Probl. 2008;24(3):20–35. doi: 10.1088/0266-5611/24/3/035020. - DOI

Publication types

LinkOut - more resources

Full Text Sources