Comparison of Income Eligibility for Medicaid vs Marketplace Coverage for Insurance Enrollment Among Low-Income US Adults

- PMID: 35977174

- PMCID: PMC8796906

- DOI: 10.1001/jamahealthforum.2021.0771

Comparison of Income Eligibility for Medicaid vs Marketplace Coverage for Insurance Enrollment Among Low-Income US Adults

Abstract

Importance: The Affordable Care Act created 2 new coverage options for uninsured adults: Medicaid expansion, which in most states provides comprehensive coverage without premiums and deductibles; and private marketplace coverage, which requires a premium contribution and cost-sharing, though with generous federal subsidies at lower incomes. How enrollment rates compare in the marketplace vs Medicaid is an important policy question as states continue to weigh alternative coverage options such as Medicaid buy-in programs, enrolling Medicaid-eligible populations into marketplace plans, or creating a public option.

Objective: To assess the association between income eligibility for Medicaid vs marketplace coverage and insurance enrollment among low-income adults in Colorado.

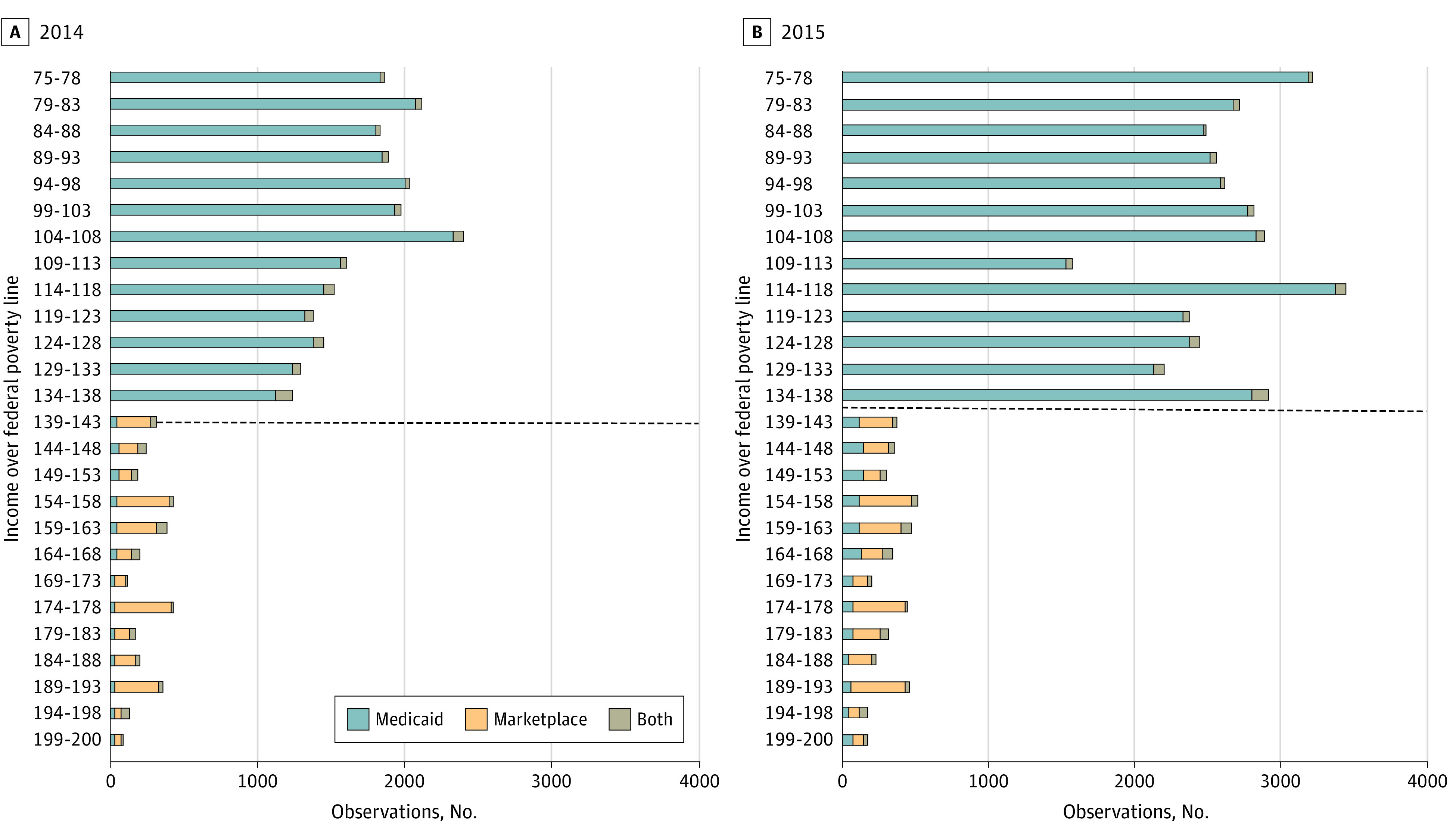

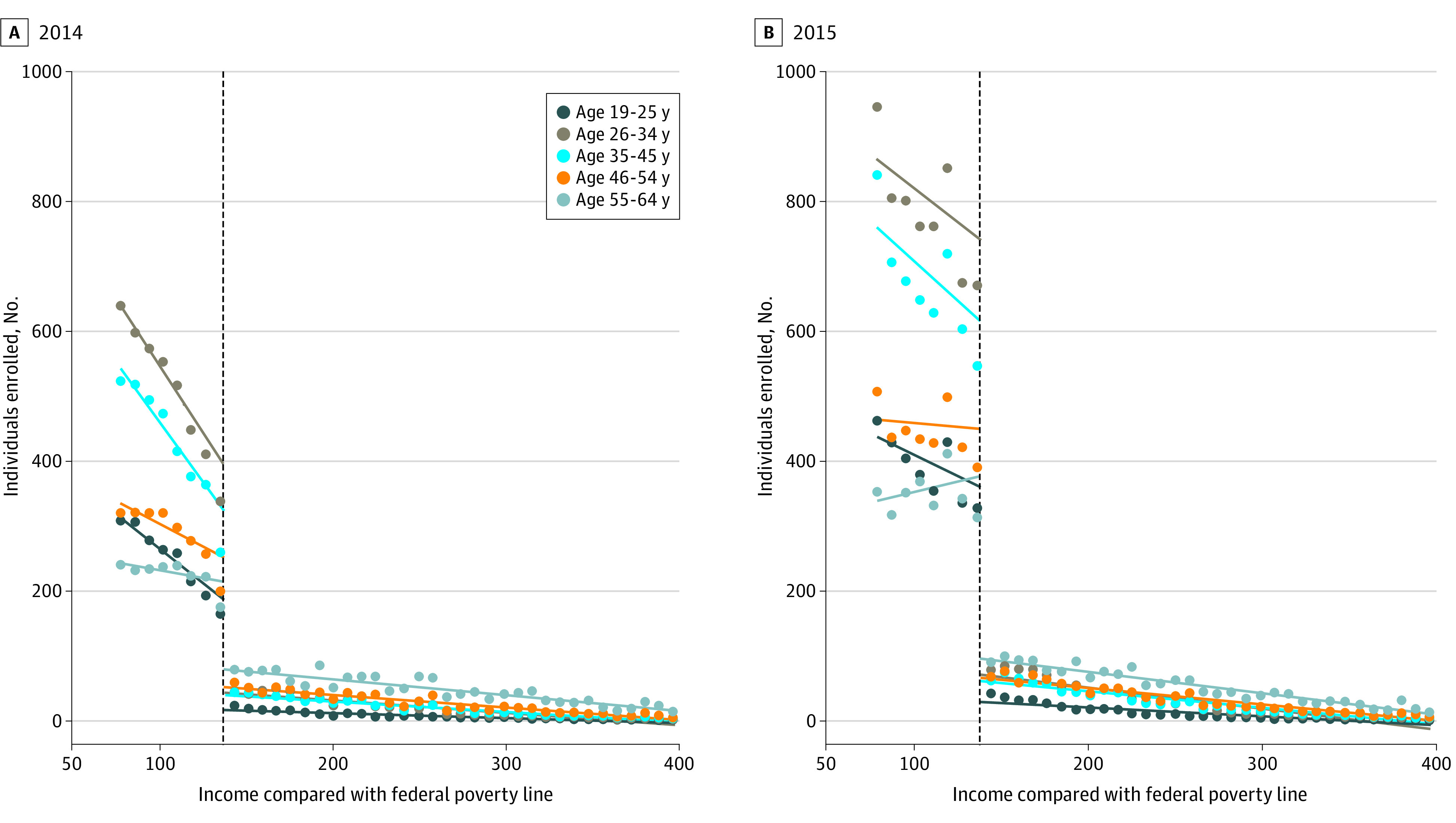

Design setting and participants: Using 2014 and 2015 all-payer claims data from Colorado and detailed income eligibility information, we used a regression discontinuity design to assess the difference in Medicaid and marketplace enrollment just below and just above 138% of the federal poverty level (FPL), the eligibility threshold between the 2 programs. The sample included nonpregnant adults aged 19 to 64 years with incomes between 75% to 400% FPL. We stratified our analysis by age, sex, chronic condition status, and urban vs rural residence. Analysis was conducted from January to October 2020.

Main outcome and measures: The main outcome was total enrollment in either Medicaid or marketplace coverage during marketplace's Open Enrollment period. Income-based health insurance eligibility was assessed as a percentage of FPL at the time of initial application for coverage.

Results: The primary analytical sample included 32 091 enrollees in 2014 and 55 451 in 2015, with incomes ranging from 120% to 156% FPL. Most enrollees were women (59.26% in 2014, 59.20% in 2015), resided in urban areas (70.36% in 2014, 73.08% in 2015), and had no chronic conditions (74.66% in 2014, 76.11% in 2015). For age, in 2014 and 2015, respectively, 13.22% and 13.93% were aged 19 to 25 years, 27.85% and 28.54% were aged 26 to 34 years, 23.58% and 24.34% were aged 35 to 44 years, 18.35% and 17.75% were aged 45 to 54 years, and 17.00% and 15.44% were aged 55 to 64 years. Marketplace enrollment was 81.3% (95% CI, -86.0% to -75.0%) lower than Medicaid enrollment in 2014 and 88.6% (95% CI, -90.8% to -86.0%) lower in 2015 among those close to the 138% FPL eligibility threshold. The drop-off in marketplace enrollment was largest among younger adults, aged 26 to 34 and 35 to 44 years: relative drop off -88.7% (95% CI, -93.3% to -80.8%) and -87.8% (95% CI, -90.8% to -83.9%) in 2014, and relative drop off -91.9% (95% CI, -94.5% to -87.9%) and -93.0% (95% CI, -94.5% to -91.1%) in 2015, respectively.

Conclusions and relevance: In this cross-sectional study using a regression-discontinuity analysis, meaningful gaps in insurance enrollment may have existed for those with incomes just above the eligibility threshold for Medicaid expansion, especially among younger adults. Policies expanding Medicaid income eligibility or zero-dollar premium marketplace plans are likely to be more effective at inducing enrollment than subsidized private plans with premium requirements.

Copyright 2021 Bhanja A et al. JAMA Health Forum.

Conflict of interest statement

Conflict of Interest Disclosures: Dr Sommers is currently on leave from Harvard and serving in the US Department of Health and Human Services; however, this article was conceived and drafted while Dr Sommers was employed at the Harvard School of Public Health, and the findings and views in this article do not reflect the official views or policy of the Department of Health and Human Services.

Figures

References

-

- Tolbert J, Orgera K, Singer N, Damico A. Key facts about the uninsured population. The Henry J Kaiser Family Foundation. 2019.

-

- Simpson M. The Implications of Medicaid Expansion in the Remaining States: 2020 Update. Published September 1, 2020. Accessed November 25, 2020. https://www.urban.org/research/publication/implications-medicaid-expansi...

-

- Dolan R. High-Deductible Health Plans: Health Affairs Brief. Health Affairs. Published February 4, 2016. Accessed November 25, 2020. https://www.healthaffairs.org/do/10.1377/hpb20160204.950878/full/ - DOI

Publication types

MeSH terms

LinkOut - more resources

Full Text Sources

Medical