On the importance of fiscal space: Evidence from short sellers during the COVID-19 pandemic

- PMID: 36119141

- PMCID: PMC9464317

- DOI: 10.1016/j.jbankfin.2022.106652

On the importance of fiscal space: Evidence from short sellers during the COVID-19 pandemic

Abstract

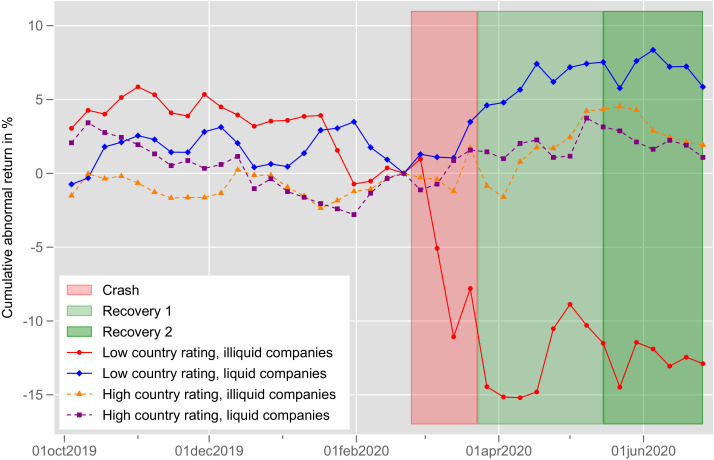

Using the exogenous shock of the COVID-19 pandemic, we study how informed market participants incorporate fiscal space into their trading decisions. At the onset of the pandemic, short-selling activity shifted towards companies with low financial flexibility but only in countries with limited fiscal space. Among such companies, short sellers specifically targeted those that generate their revenues mainly in the domestic market. These short sellers entered their positions before the market crash, thereby generating significant abnormal returns. We find no evidence of either herding behavior prior to the market crash or a long-run performance reversal of short sellers. These findings support the notion that short sellers help to promote price efficiency in times of crisis, where governments with budgetary constraints are unable to provide sufficient stimuli to their economies.

Keywords: COVID-19 pandemic; Fiscal space; Institutional investors; Short selling.

© 2022 The Authors. Published by Elsevier B.V.

Figures

References

-

- Acharya V.V., Steffen S. The risk of being a fallen angel and the corporate dash for cash in the midst of COVID. Rev. Corp. Finance Stud. 2020;9(3):430–471. doi: 10.1093/rcfs/cfaa013. - DOI

-

- Ackermann C., McEnally R., Ravenscraft D. The performance of hedge funds: risk, return, and incentives. J. Financ. 1999;54(3):833–874. doi: 10.1111/0022-1082.00129. - DOI

-

- Akbas F., Armstrong W.J., Sorescu S., Subrahmanyam A. Smart money, dumb money, and capital market anomalies. J. Financ. Econ. 2015;118(2):355–382.

-

- Alessi L., Ossola E., Panzica R. What greenium matters in the stock market? The role of greenhouse gas emissions and environmental disclosures. J. Financ. Stab. 2021;54:100869.

-

- Aizenman, J., Jinjarak, Y., 2010. De facto fiscal space and fiscal stimulus: definition and assessment. Working Paper 16539. NBER. doi:10.3386/w16539

LinkOut - more resources

Full Text Sources