Fisher's hypothesis in time-frequency space: a premier using South Africa as a case study

- PMID: 36320216

- PMCID: PMC9614770

- DOI: 10.1007/s11135-022-01561-z

Fisher's hypothesis in time-frequency space: a premier using South Africa as a case study

Abstract

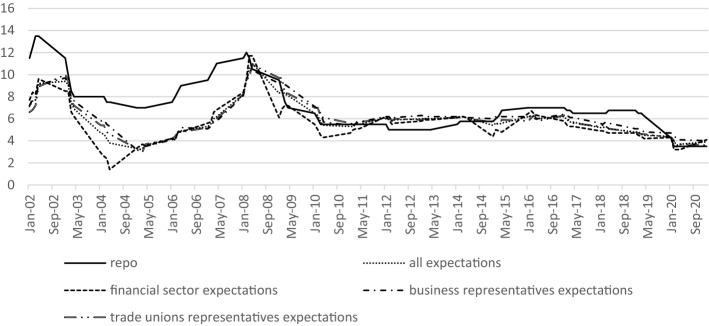

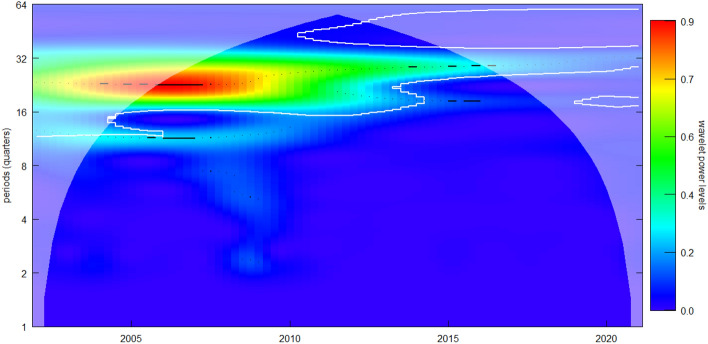

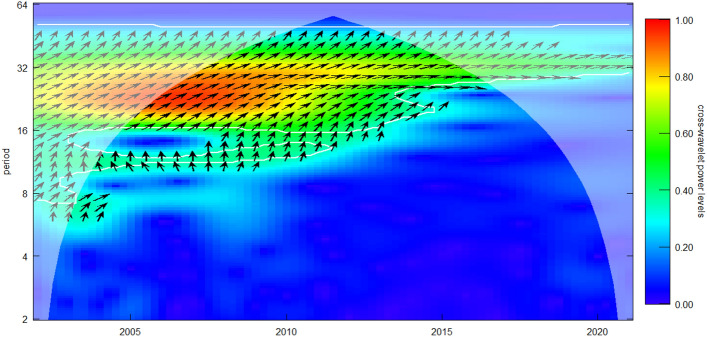

Fisher hypothesis is universally accepted as an integral portion of monetary theory and practice, and yet the empirical evidence confirming a full Fisher effect remains scarce and the relationship has been challenged on several theoretical grounds referred to as 'puzzles'. Our paper suggests the use of continuous wavelet transforms as a unified analytical framework for confronting the different Fisher puzzles in a harmonious way. Taking South Africa as a case study, we focus on the inflation targeting period of 2002:01-2021:02 and use signal-image conversion tools such as wavelet power spectrum, wavelet coherence spectrum and phase-difference dynamics to extract signal features of nominal interest rates and inflation expectations and further explore their dynamic synchronization across a time-frequency plane/domain. Three unique findings emerge from our study. Firstly, across a time domain a full Fisher effect only holds in the pre-financial crisis period. Secondly, across the frequency spectrums, higher frequency oscillations gradually lose relevance to lower frequency oscillations providing evidence of volatility transfer in the Fisher effect. Lastly, the phase-dynamics indicate a consistent positive synchronization throughout the sample period which is line with the traditional Fisher effect. Overall, these findings highlight the success of the South African Reserve Bank in using inflation targeting to steer the expectations of economic agents under the tenures of the last three governors and provide important lessons for other Central banks.

Keywords: Continuous wavelet transforms; Fisher effect; Interest rates, Inflation expectations; Morlet wavelets.

© The Author(s), under exclusive licence to Springer Nature B.V. 2022, Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

Conflict of interest statement

Conflict of interestThe author has nothing to declare.

Figures

References

-

- Aguiar-Conraria L, Soares M. The continuous wavelet transform: moving beyond uni- and bi-variate analysis. J. Econ. Surv. 2014;28(2):344–375. doi: 10.1111/joes.12012. - DOI

-

- Aguiar-Conraria L, Martins M, Soares M. Estimating the Taylor rule in a time-frequency domain. J. Macroecon. 2018;57:122–137. doi: 10.1016/j.jmacro.2018.05.008. - DOI

-

- Aguiar-Conraria L., Soares M.: The continuous wavelet transform: a primer. NIPE Working Paper No. 23, August (2010)

-

- Alagidede I, Panagiotidis T. Can common stocks provide a hedge against inflation? Evidence from African countries. Rev. Financ. Econ. 2010;19(3):91–100. doi: 10.1016/j.rfe.2010.04.002. - DOI

-

- Amano R., Carter T., Mendes R.: A primer on Neo-Fisherian economics. Bank of Canada Staff Analytical Notes 16–14, September (2016)

LinkOut - more resources

Full Text Sources