Time-varying higher moments in Bitcoin

- PMID: 36575661

- PMCID: PMC9780105

- DOI: 10.1007/s42521-022-00072-8

Time-varying higher moments in Bitcoin

Abstract

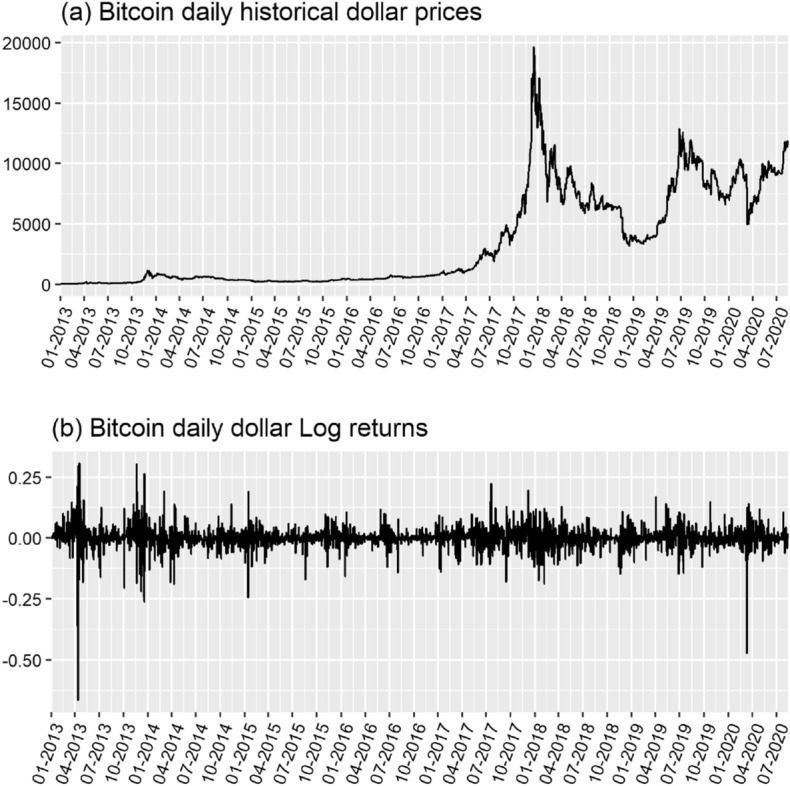

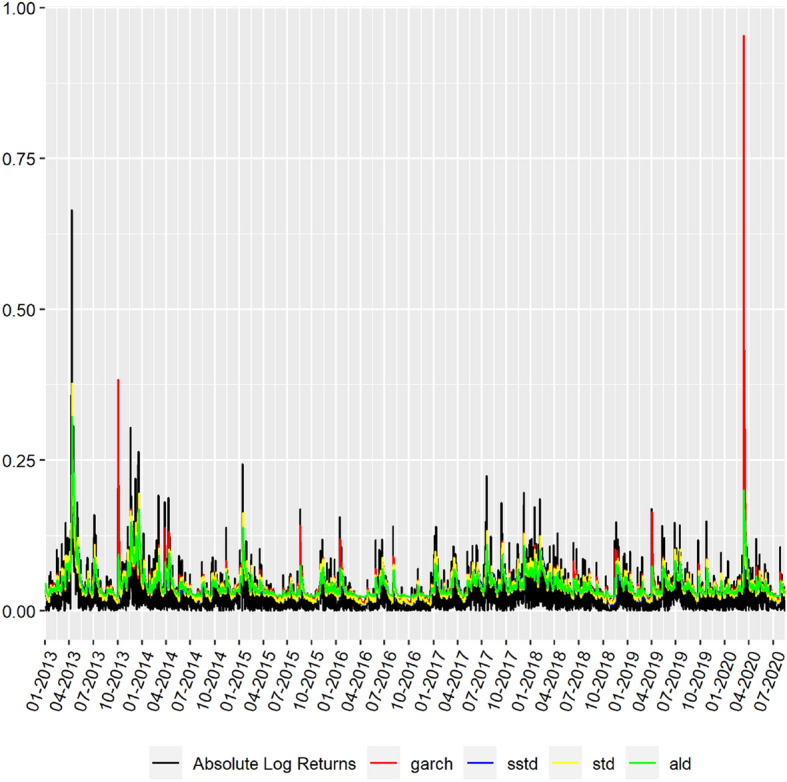

Cryptocurrencies represent a new and important class of investments but are associated with asymmetric distributions and extreme price changes. We use a modeling structure where higher-order moments (scale, skewness and kurtosis) are time-varying, and additionally we used nontraditional innovations distributions to study the return series of the most important cryptocurrency, Bitcoin. Based on the estimation of a series of Generalized Autoregressive Score (GAS) models, we compare predictive performance using a loss function based on Value at Risk performance.

Keywords: Bitcoin; Generalized autoregressive score; Higher-order moments; Risk management.

© The Author(s), under exclusive licence to Springer Nature Switzerland AG 2022, Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

Conflict of interest statement

Conflict of interestThe authors report the absence of any type of conflict of interest.

Figures

References

-

- Abad P, Muela SB, Martin CL. The role of the loss function in Value-at-Risk comparisons. Journal of Risk Model Validation. 2015;9(1):1–19. doi: 10.21314/JRMV.2015.132. - DOI

-

- Aggarwal D. Do bitcoins follow a random walk model? Research in Economics. 2019;73(1):15–22. doi: 10.1016/j.rie.2019.01.002. - DOI

-

- Ardia, D., Boudt, K., & Catania, L. (2016). Value-at-Risk prediction in R with the GAS package. arXiv: Risk Management.

-

- Ardia D, Boudt K, Catania L. Generalized Autoregressive Score models in R: The gas package. Journal of Statistical Software, Articles. 2019;88(6):1–28.

-

- Bariviera AF. The inefficiency of Bitcoin revisited: A dynamic approach. Economics Letters. 2017;161:1–4. doi: 10.1016/j.econlet.2017.09.013. - DOI

LinkOut - more resources

Full Text Sources