Information shocks, market returns and volatility: a comparative analysis of developed equity markets in Asia

- PMID: 36684690

- PMCID: PMC9838341

- DOI: 10.1007/s43546-022-00417-w

Information shocks, market returns and volatility: a comparative analysis of developed equity markets in Asia

Abstract

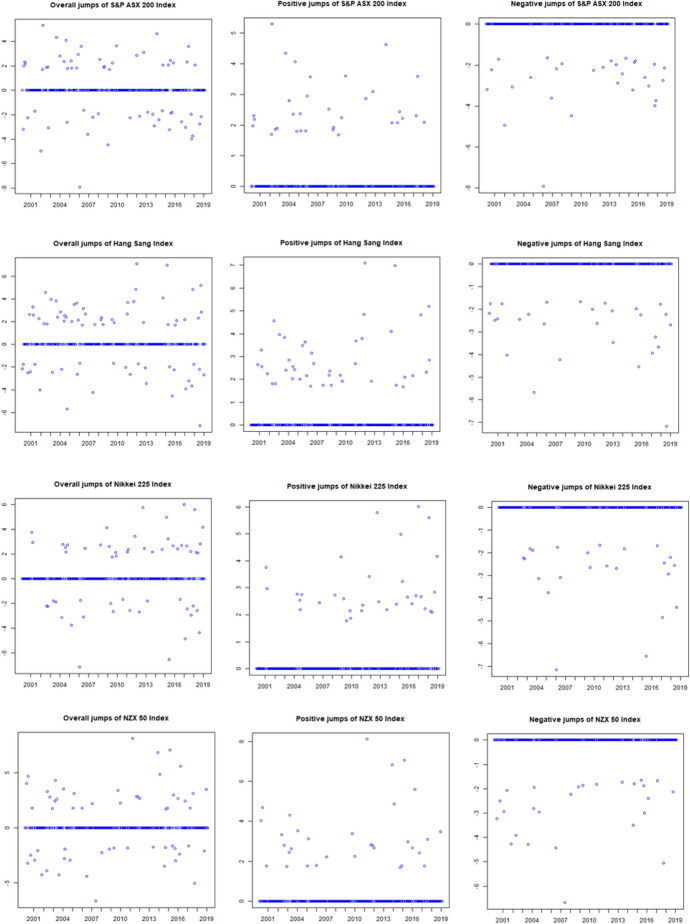

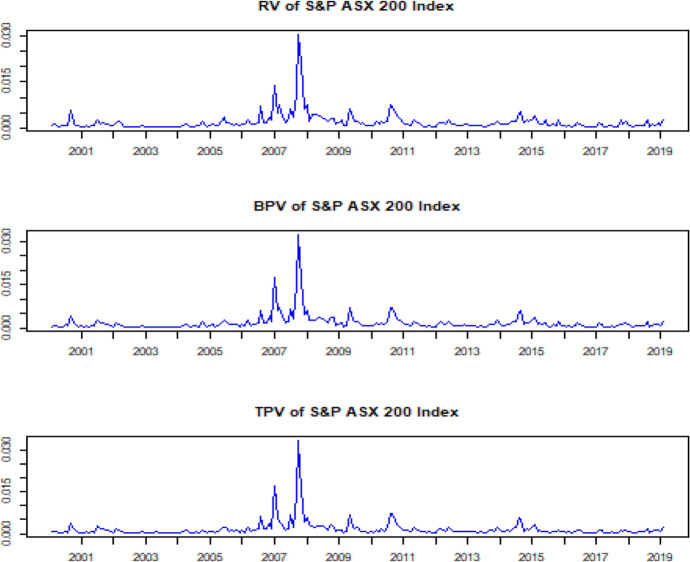

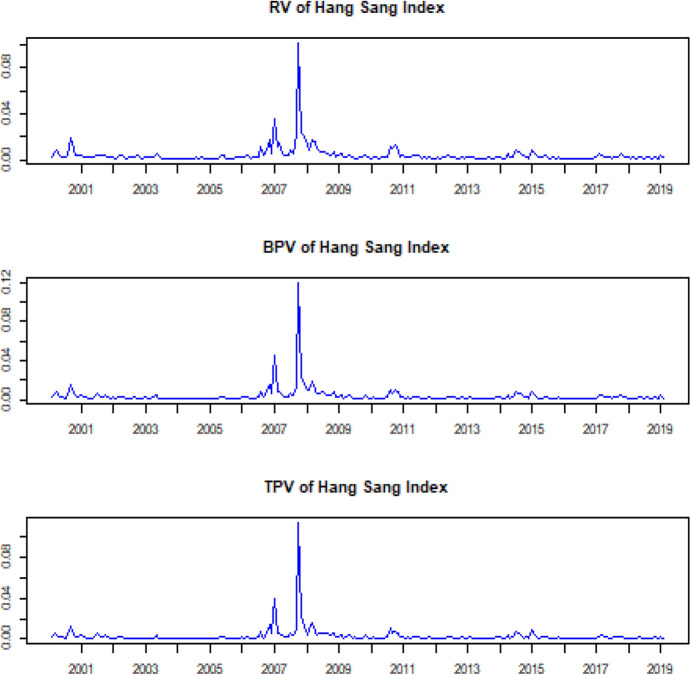

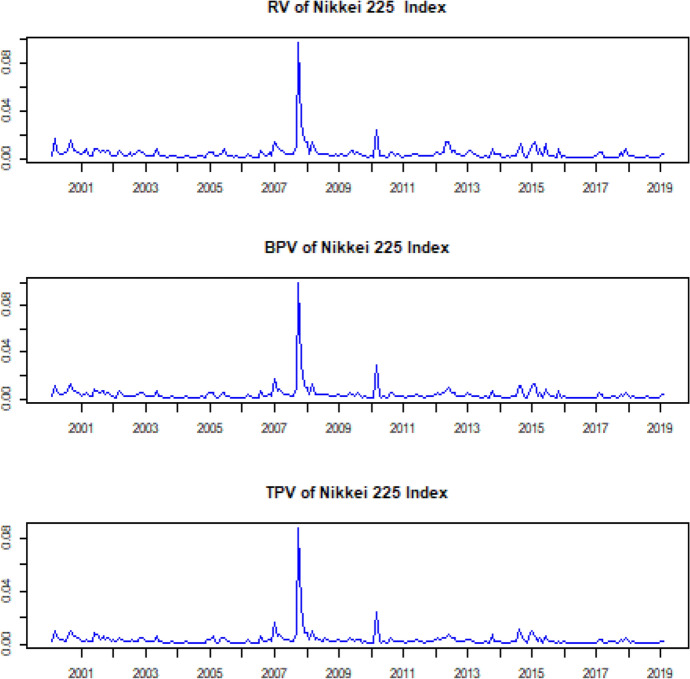

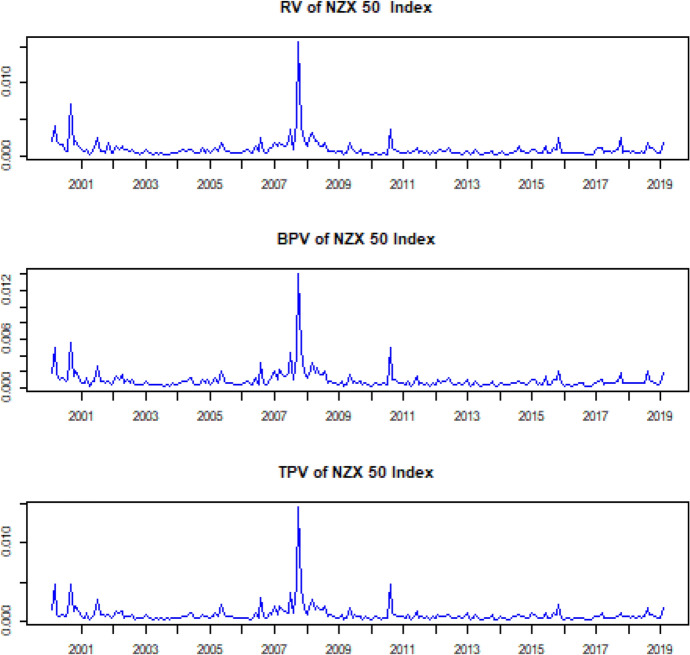

This research explores the function of information shocks in equity returns and integrated volatility of emerging Asian markets using Swap Variance (SwV) approach on the period of 20 years (Feb 2001-Feb 2020). It compares average monthly returns and volatility of shock periods with non-shock periods after separating negative and positive shocks. Findings reveal frequent occurrence of information shocks in all Asian developed equity markets with positive shocks than that of negative shocks. Moreover, highly volatile Asian developed markets earn higher returns during shocks periods, while markets with higher volatility and lower continuous returns are adversely affected during shocks periods. The ratio of total realized volatility and the average ratio of shocks volatility establish that shocks account for a considerable amount of volatility, and integrated volatility is higher during negative shocks phases. The study has implications for all stakeholders of financial markets for rational investment decisions.

Keywords: Bipower variation; Realized volatility; Shock identification; Swap variance; Tripower variation.

© The Author(s), under exclusive licence to Springer Nature Switzerland AG 2023, Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

Conflict of interest statement

Conflict of interestThe authors have no competing interests in the material submitted for publication, either directly or indirectly.

Figures

Similar articles

-

How do equity markets react to COVID-19? Evidence from emerging and developed countries.J Econ Bus. 2021 May-Jun;115:105966. doi: 10.1016/j.jeconbus.2020.105966. Epub 2020 Dec 3. J Econ Bus. 2021. PMID: 33518845 Free PMC article.

-

The predictive power of oil price shocks on realized volatility of oil: A note.Resour Policy. 2020 Dec;69:101856. doi: 10.1016/j.resourpol.2020.101856. Epub 2020 Sep 23. Resour Policy. 2020. PMID: 34173422 Free PMC article.

-

Financial uncertainty and interest rate movements: is Asian bond market volatility different?Ann Oper Res. 2021 Nov 1:1-29. doi: 10.1007/s10479-021-04314-7. Online ahead of print. Ann Oper Res. 2021. PMID: 34744240 Free PMC article.

-

Oil price shocks, stock market returns, and volatility spillovers: a bibliometric analysis and its implications.Environ Sci Pollut Res Int. 2022 Apr;29(16):22809-22828. doi: 10.1007/s11356-021-18314-4. Epub 2022 Jan 19. Environ Sci Pollut Res Int. 2022. PMID: 35048345 Free PMC article. Review.

-

Time-frequency domain analysis of investor fear and expectations in stock markets of BRIC economies.Heliyon. 2021 Oct 19;7(10):e08211. doi: 10.1016/j.heliyon.2021.e08211. eCollection 2021 Oct. Heliyon. 2021. PMID: 34754971 Free PMC article. Review.

Cited by

-

Does US monetary policy uncertainty affect returns of Asian Developed, emerging, and frontier equity markets? Empirical evidence by using the quantile-on-quantile approach.Heliyon. 2024 Jun 13;10(12):e32962. doi: 10.1016/j.heliyon.2024.e32962. eCollection 2024 Jun 30. Heliyon. 2024. PMID: 38948042 Free PMC article.

References

-

- Ahmad KM, Ashraf S, Ahmed S. Is the Indian stock market integrated with the US and Japanese markets? An empirical analysis. South Asia Econ J. 2005;6(2):193–206. doi: 10.1177/139156140500600202. - DOI

-

- Aıt-Sahalia Y. Disentangling diffusion from jumps. J Financ Econ. 2004;74(3):487–528. doi: 10.1016/j.jfineco.2003.09.005. - DOI

-

- Aït-Sahalia Y, Jacod J (2009a) Testing for jumps in a discretely observed process. The Annals of Statistics, 184–222.

-

- Aït-Sahalia Y, Hurd TR. Portfolio choice in markets with contagion. J Financ Economet. 2015;14(1):1–28. doi: 10.1093/jjfinec/nbv024. - DOI

-

- Aït-Sahalia Y, Jacod J. Testing for jumps in a discretely observed process. Ann Stat. 2009;37:184–222. doi: 10.1214/07-AOS568. - DOI

LinkOut - more resources

Full Text Sources