Have the predictability of oil changed during the COVID-19 pandemic: Evidence from international stock markets

- PMID: 36942110

- PMCID: PMC10015825

- DOI: 10.1016/j.irfa.2023.102620

Have the predictability of oil changed during the COVID-19 pandemic: Evidence from international stock markets

Abstract

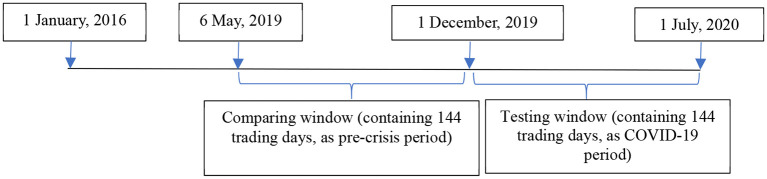

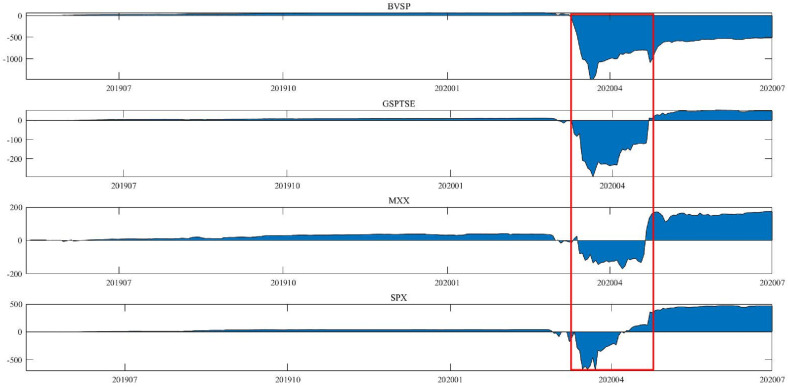

The COVID-19 has undoubtfully brought fierce shocks to the real economic activities, financial market and public lives. Under this special condition, this study explores whether the predictability of crude oil futures information has changed before and during the COVID-19 pandemic for 19 international stock markets. From an in-sample perspective, we find that the crude oil futures RV can significantly affect future stock volatility for each equity index except SSEC. Moreover, the out-of-sample results from statistic and economic perspective reveal that crude oil futures RV is a more efficient predictor during the COVID-19 pandemic compared with the pre-crisis period. Furthermore, we find that the predictability of crude oil futures information is stronger from March to May 2020, when the epidemic is seriously prevailing. The empirical results from alternative evaluation method, recursive window method, alternative realized measures, controlling VIX and the seasonal effect, asymmetric forecasting window and different testing windows are robust and consistent. Our findings could offer novel and significant policy and practical implications.

Keywords: COVID-19 pandemic; Cross-market transmission; Crude oil futures; Realized volatility forecasting; Stock market.

© 2023 Published by Elsevier Inc.

Figures

Similar articles

-

Which popular predictor is more useful to forecast international stock markets during the coronavirus pandemic: VIX vs EPU?Int Rev Financ Anal. 2020 Nov;72:101596. doi: 10.1016/j.irfa.2020.101596. Epub 2020 Sep 28. Int Rev Financ Anal. 2020. PMID: 38620312 Free PMC article.

-

Determining the COVID-19 effects on spillover between oil market and stock exchange: a global perspective analysis.Environ Sci Pollut Res Int. 2022 Sep;29(44):66109-66124. doi: 10.1007/s11356-022-19607-y. Epub 2022 May 1. Environ Sci Pollut Res Int. 2022. PMID: 35501434 Free PMC article.

-

Crude oil market and stock markets during the COVID-19 pandemic: Evidence from the US, Japan, and Germany.Int Rev Financ Anal. 2021 Mar;74:101702. doi: 10.1016/j.irfa.2021.101702. Epub 2021 Feb 6. Int Rev Financ Anal. 2021. PMID: 38620728 Free PMC article.

-

Evaluating the Safe-Haven Abilities of Bitcoin and Gold for Crude Oil Market: Evidence During the COVID-19 Pandemic.Eval Rev. 2023 Jun;47(3):391-432. doi: 10.1177/0193841X221141812. Epub 2022 Dec 1. Eval Rev. 2023. PMID: 36453754 Free PMC article. Review.

-

Time-frequency domain analysis of investor fear and expectations in stock markets of BRIC economies.Heliyon. 2021 Oct 19;7(10):e08211. doi: 10.1016/j.heliyon.2021.e08211. eCollection 2021 Oct. Heliyon. 2021. PMID: 34754971 Free PMC article. Review.

References

-

- Andersen T.G., Bollerslev T. Answering the skeptics: Yes, standard volatility models do provide accurate forecasts. International Economic Review. 1998;39(4):885–905.

-

- Andersen T.G., Bollerslev T., Diebold F.X. Roughing it up: Including jump components in the measurement, modeling, and forecasting of return volatility. The Review of Economics and Statistics. 2007;89:701–720.

-

- Audrino F., Sigrist F., Ballinari D. The impact of sentiment and attention measures on stock market volatility. International Journal of Forecasting. 2020;36(2):334–357.

-

- Baker S.R., Bloom N., Davis S.J., Kost K.J., Sammon M.C., Viratyosin T. National Bureau of Economic Research; 2020. The unprecedented stock market impact of COVID-19 (Vol. No. w26945)

LinkOut - more resources

Full Text Sources