Compounding COVID-19 and climate risks: The interplay of banks' lending and government's policy in the shock recovery

- PMID: 37256115

- PMCID: PMC10208724

- DOI: 10.1016/j.jbankfin.2021.106306

Compounding COVID-19 and climate risks: The interplay of banks' lending and government's policy in the shock recovery

Abstract

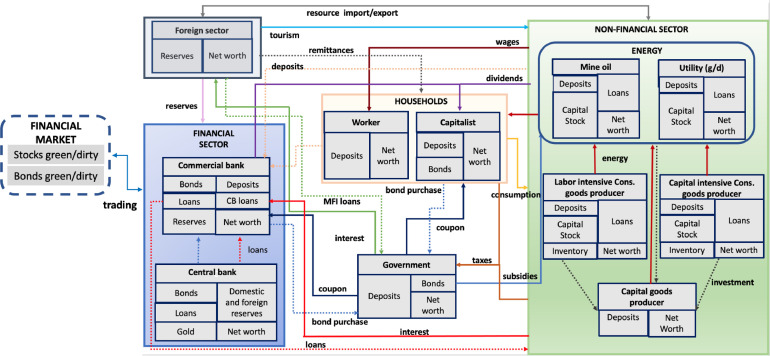

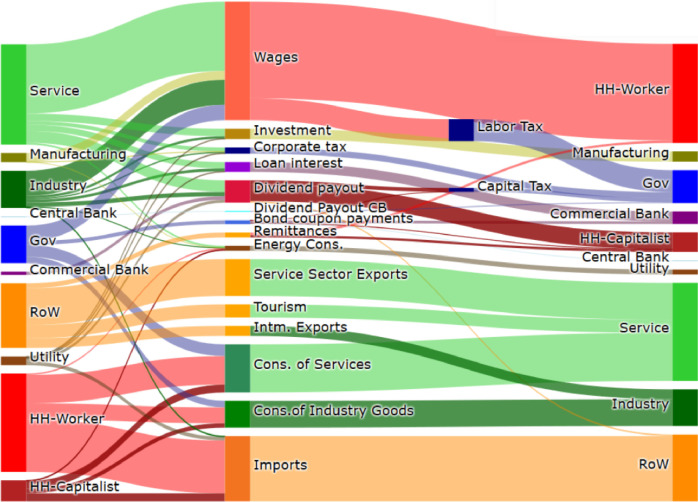

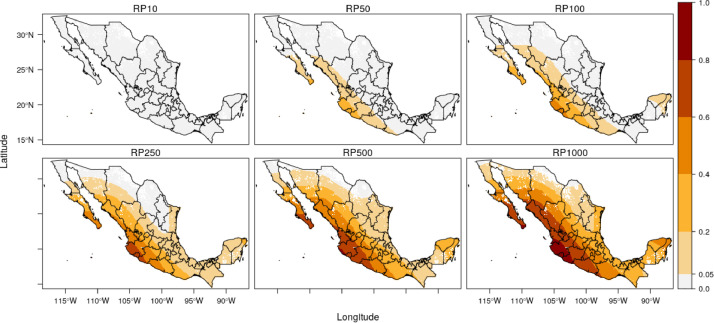

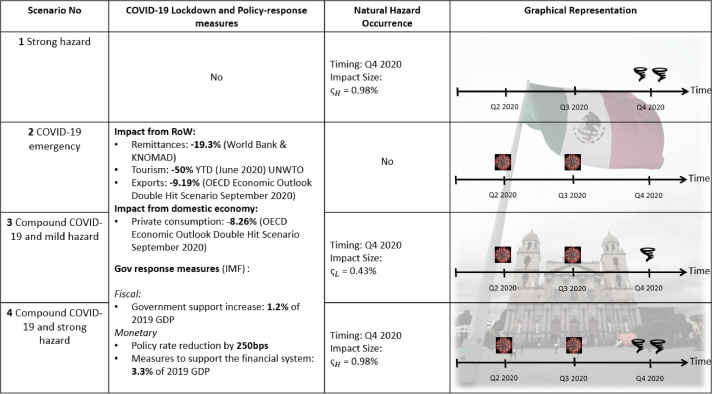

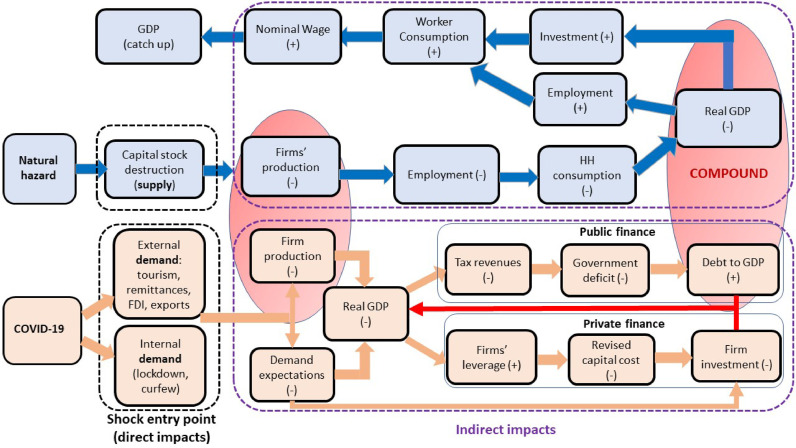

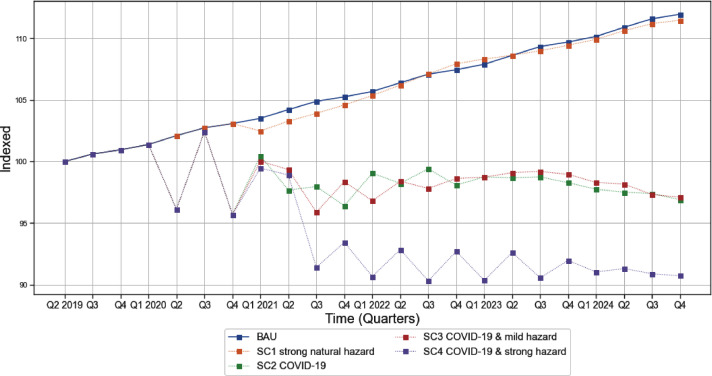

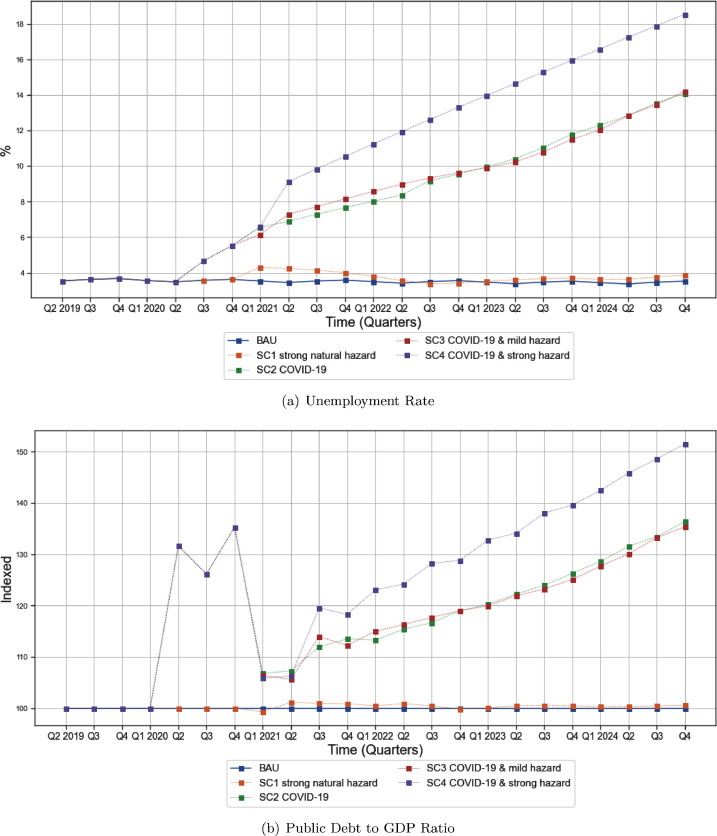

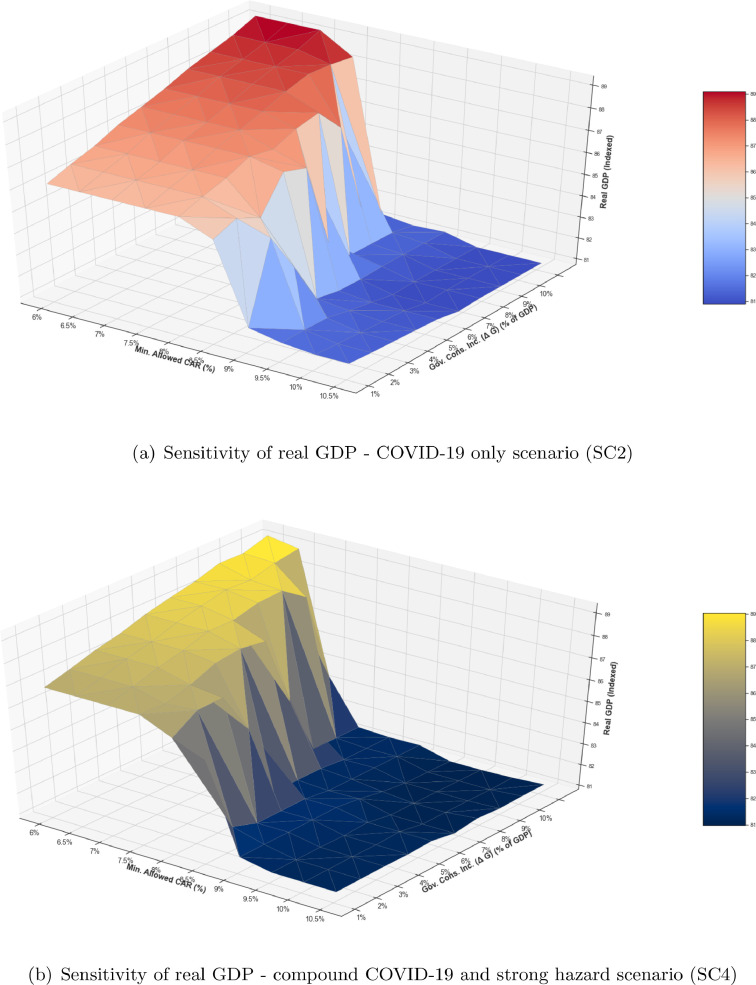

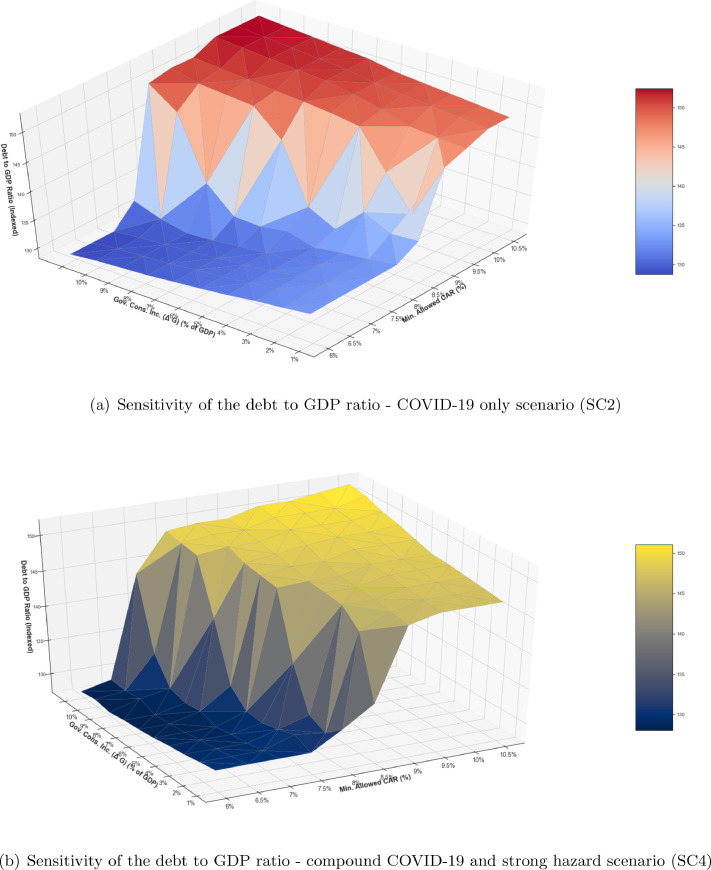

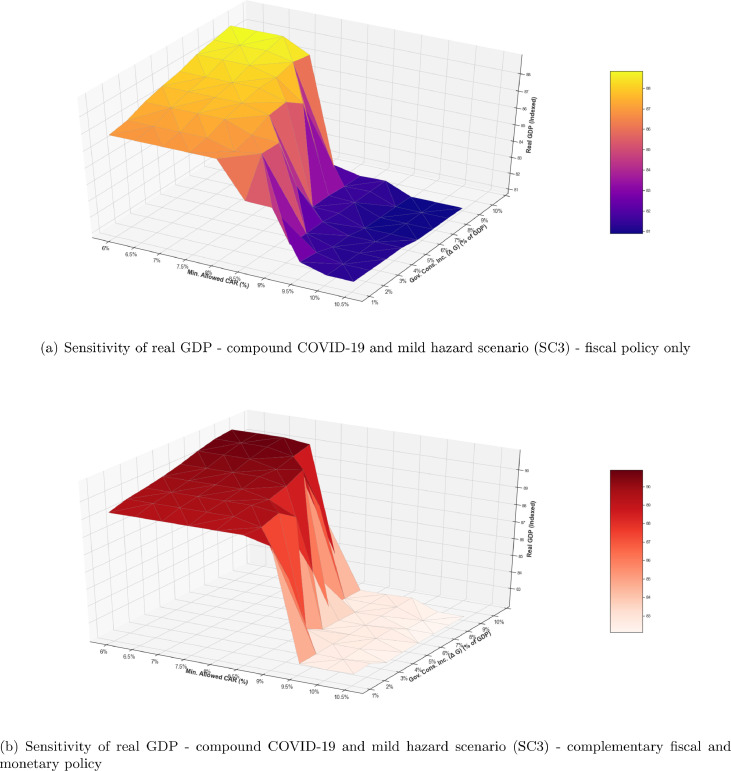

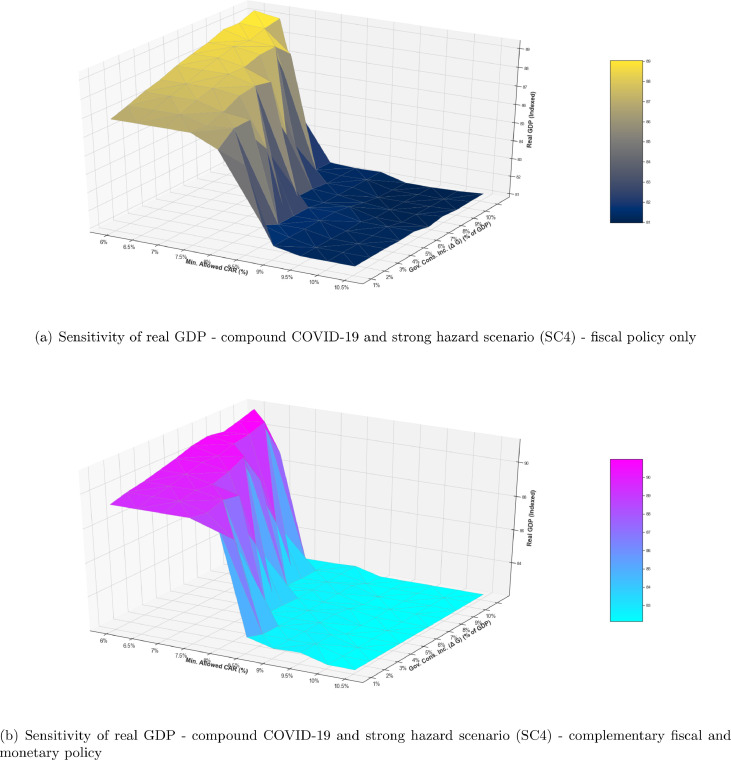

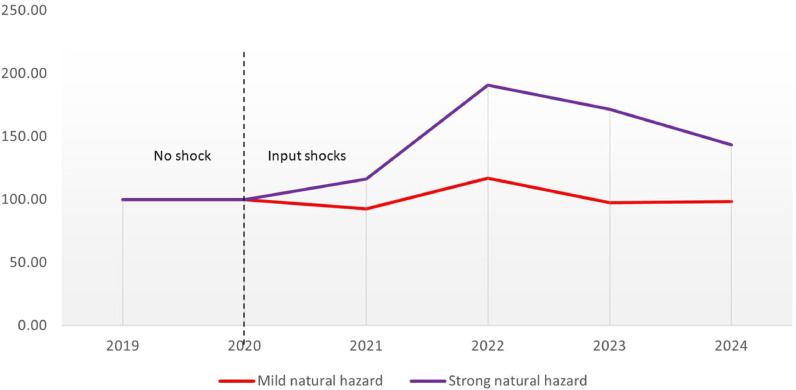

We assess the individual and compounding impacts of COVID-19 and climate physical risks in the economy and finance, using the EIRIN Stock-Flow Consistent model. We study the interplay between banks' lending decisions and government's policy effectiveness in the economic recovery process. We calibrate EIRIN on Mexico, being a country highly exposed to COVID-19 and hurricanes risks. By embedding financial actors and the credit market, and by endogenising investors' expectations, EIRIN analyses the finance-economy feedbacks, providing an accurate assessment of risks and policy co-benefits. We quantify the impacts of compounding COVID-19 and hurricanes on GDP through time using a compound risk indicator. We find that procyclical lending and credit market constraints amplify the initial shocks by limiting firms' recovery investments, thus mining the effectiveness of higher government spending. When COVID-19 and hurricanes compound, non-linear dynamics that amplify losses emerge, negatively affecting the economic recovery, banks' financial stability and public debt sustainability.

Keywords: COVID-19; Climate change; Compound risk; Credit market constraints; Government policies; Macrofinancial impacts; Procyclical bank lending; Stock-flow consistent model.

© 2021 The Authors. Published by Elsevier B.V.

Figures

References

-

- Adrian, T., Natalucci, F., 2020. COVID-19 Crisis Poses Threat to Financial Stability. https://blogs.imf.org/2020/04/14/covid-19-crisis-poses-threat-to-financi....

-

- Andries A.M., Ongena S., Srincean N. The COVID-19 pandemic and sovereign bond risk. Swiss Finance Inst. Res. Pap. Ser. 2020:20–42. doi: 10.2139/ssrn.3605155. - DOI

-

- Atlas of Economic Complexity, 2020. Export and Import Basket - Mexico. https://atlas.cid.harvard.edu/countries/138.

-

- Battiston S., Billio M., Monasterolo I. In: A New World Post COVID-19 Lessons for Business, the Finance Industry and Policy Makers. Billio M., Varotto S., editors. E-book; 2020. Pandemics, climate and public finance: how to strengthen socio-economic resilience across policy domains. - DOI

LinkOut - more resources

Full Text Sources