On learning agent-based models from data

- PMID: 37286576

- PMCID: PMC10247821

- DOI: 10.1038/s41598-023-35536-3

On learning agent-based models from data

Abstract

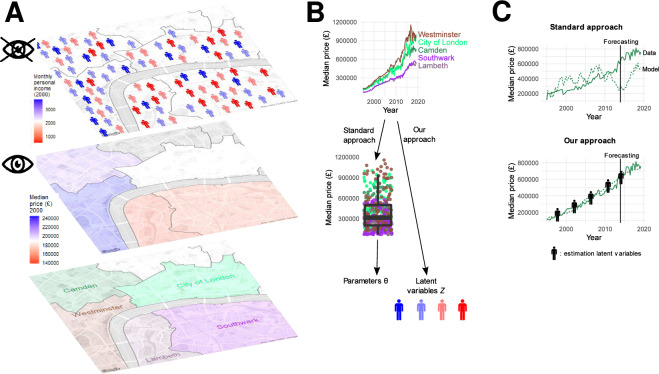

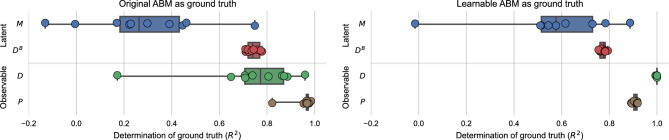

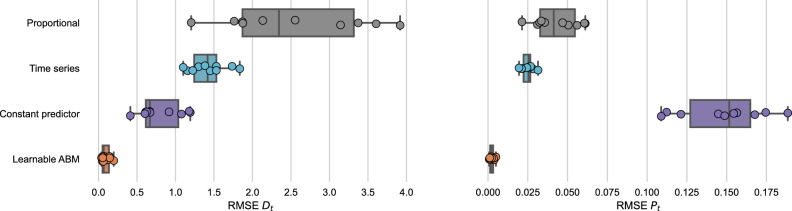

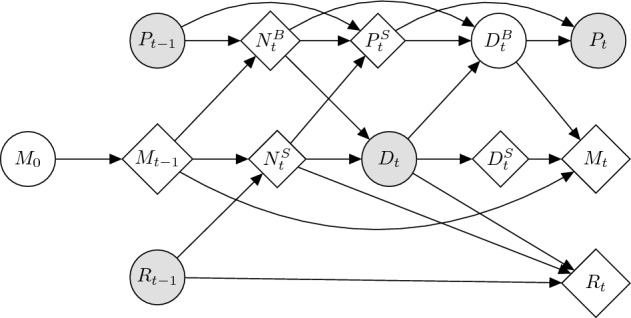

Agent-Based Models (ABMs) are used in several fields to study the evolution of complex systems from micro-level assumptions. However, a significant drawback of ABMs is their inability to estimate agent-specific (or "micro") variables, which hinders their ability to make accurate predictions using micro-level data. In this paper, we propose a protocol to learn the latent micro-variables of an ABM from data. We begin by translating an ABM into a probabilistic model characterized by a computationally tractable likelihood. Next, we use a gradient-based expectation maximization algorithm to maximize the likelihood of the latent variables. We showcase the efficacy of our protocol on an ABM of the housing market, where agents with different incomes bid higher prices to live in high-income neighborhoods. Our protocol produces accurate estimates of the latent variables while preserving the general behavior of the ABM. Moreover, our estimates substantially improve the out-of-sample forecasting capabilities of the ABM compared to simpler heuristics. Our protocol encourages modelers to articulate assumptions, consider the inferential process, and spot potential identification problems, thus making it a useful alternative to black-box data assimilation methods.

© 2023. The Author(s).

Conflict of interest statement

The authors declare no competing interests.

Figures

References

-

- Wilensky, U. & Rand, W. An Introduction to Agent-Based Modeling: Modeling Natural, Social, and Engineered Complex Systems with NetLogo (Mit Press, 2015).

-

- Railsback, S. F. & Grimm, V. Agent-Based and Individual-Based Modeling: A Practical Introduction. (Princeton University Press, 2019).

-

- Axelrod R. The dissemination of culture: A model with local convergence and global polarization. J. Confl. Resol. 1997;41(2):203–226. doi: 10.1177/0022002797041002001. - DOI

-

- Lux T. Estimation of agent-based models using sequential monte Carlo methods. J. Econ. Dyn. Control. 2018;91:391–408. doi: 10.1016/j.jedc.2018.01.021. - DOI

-

- Delli Gatti D, Grazzini J. Rising to the challenge: Bayesian estimation and forecasting techniques for macroeconomic agent based models. J. Econ. Behav. Organ. 2020;178:875–902. doi: 10.1016/j.jebo.2020.07.023. - DOI

LinkOut - more resources

Full Text Sources