Effects of the first wave of COVID-19 pandemic on implied stock market volatility: International evidence using a google trend measure

- PMID: 37325185

- PMCID: PMC10258586

- DOI: 10.1016/j.jeca.2023.e00317

Effects of the first wave of COVID-19 pandemic on implied stock market volatility: International evidence using a google trend measure

Abstract

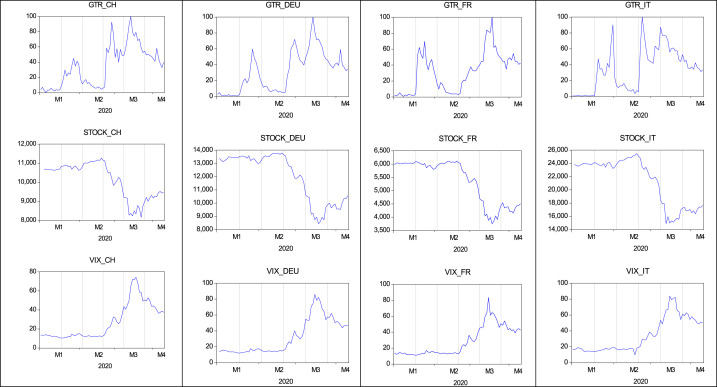

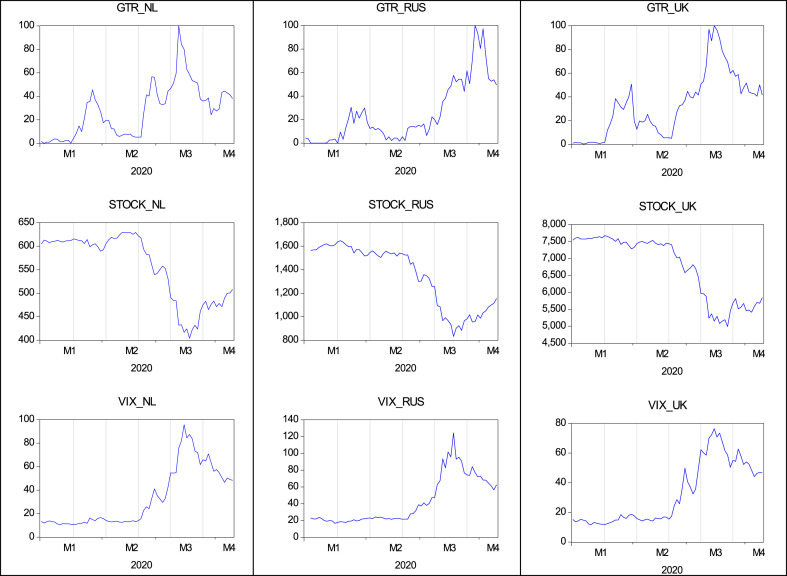

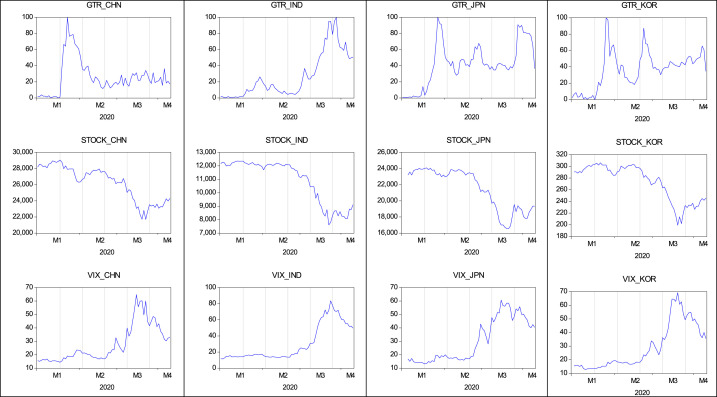

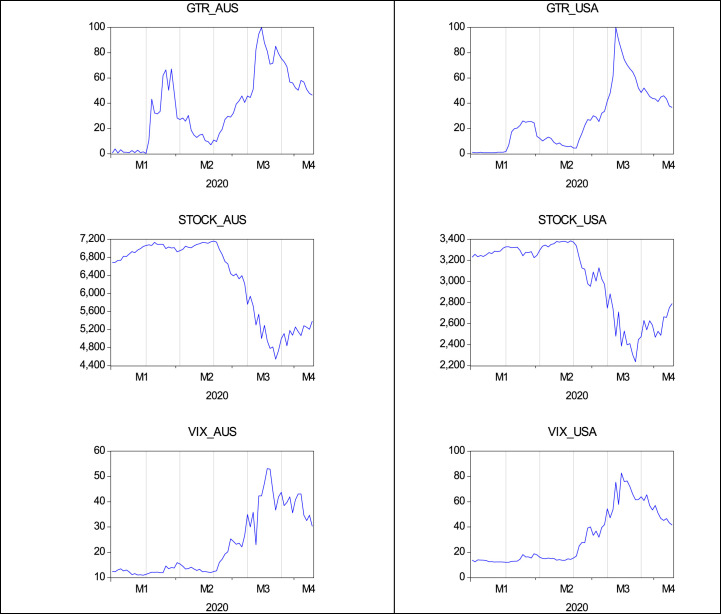

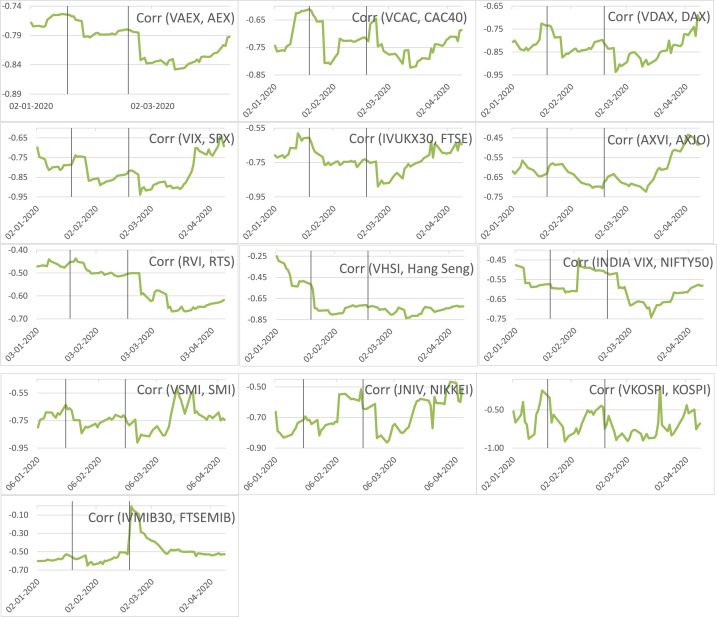

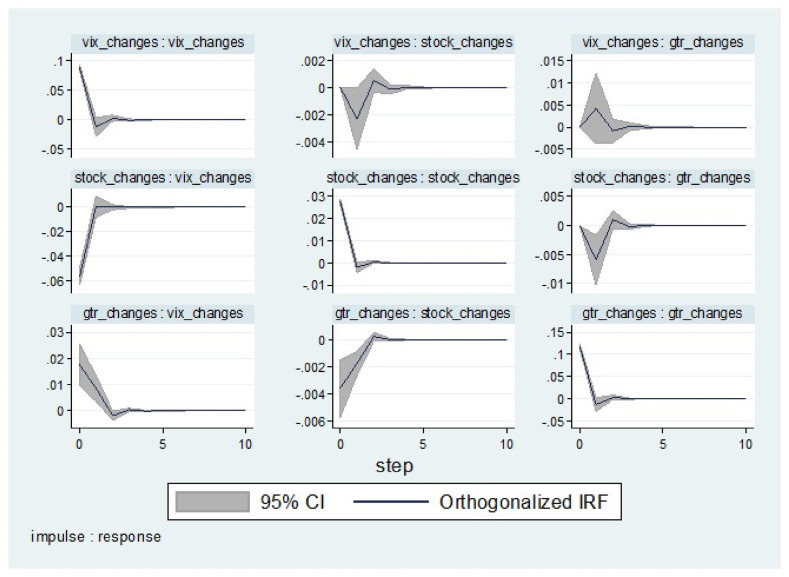

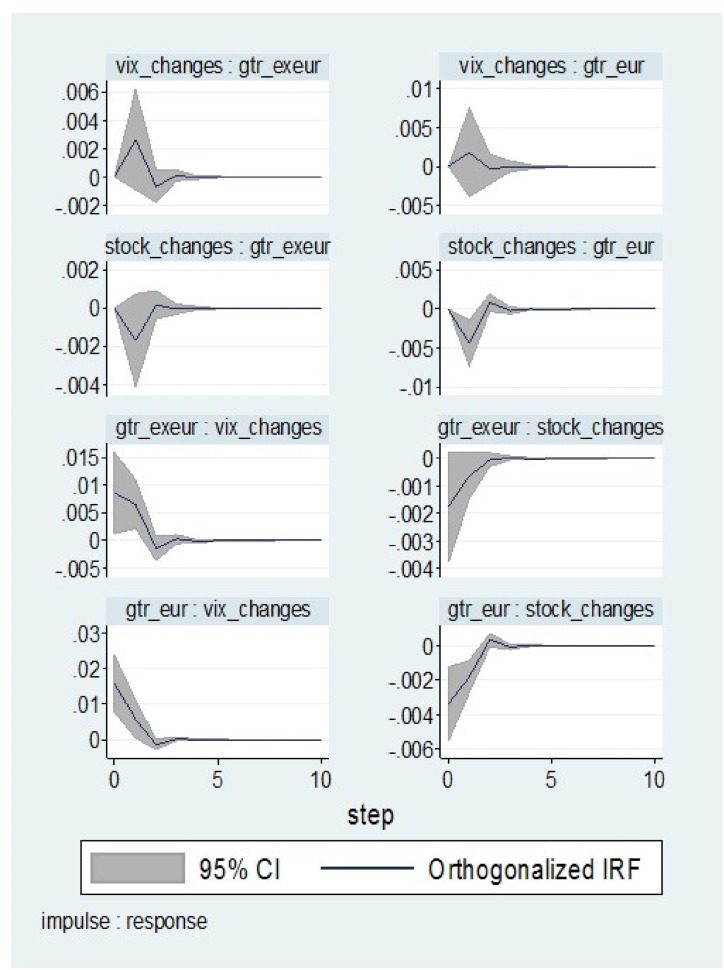

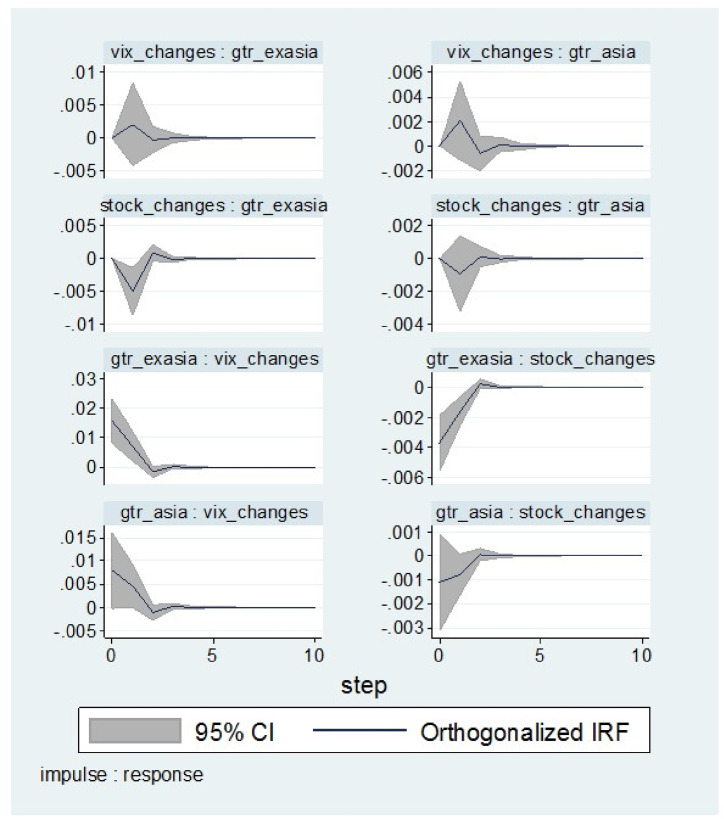

This paper investigates the relationship between investors' attention, as measured by Google search queries, and equity implied volatility during the COVID-19 outbreak. Recent studies show that search investors' behavior data is an extremely abundant repository of predictive data, and investor-limited attention increases when the uncertainty level is high. Our study using data from thirteen countries across the globe during the first wave of the COVID-19 pandemic (January-April 2020) examines whether the search "topic and terms" for the pandemic affect market participants' expectations about future realized volatility. With the panic and uncertainty about COVID-19, our empirical findings show that increased internet searches during the pandemic caused the information to flow into the financial markets at a faster rate and thus resulting in higher implied volatility directly and via the stock return-risk relation. More specifically for the latter, the leverage effect in the VIX becomes stronger as Google search queries intensify. Both the direct and indirect effects on implied volatility, highlight a risk-aversion channel that operates during the pandemic. We also find that these effects are stronger in Europe than in the rest of the world. Moreover, in a panel vector autoregression framework, we show that a positive shock on stock returns may soothe COVID-related Google searches in Europe. Our findings suggest that Google-based attention to COVID-19 leads to elevated risk aversion in stock markets.

Keywords: COVID-19 pandemic; Google trends; Implied volatility; Panel analysis; Stock returns.

© 2023 Elsevier B.V. All rights reserved.

Conflict of interest statement

The authors declare that they have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

Figures

References

-

- Abrigo M.R., Love I. Estimation of panel vector autoregression in Stata. STATA Journal. 2016;16(3):778–804.

-

- Afkhami M., Cormack L., Ghoddusi H. Google search keywords that best predict energy price volatility. Energy Economics. 2017;67:17–27.

-

- Akhtaruzzaman M., Boubaker S., Lucey B.M., Sensoy A. Is gold a hedge or a safe-haven asset in the COVID–19 crisis? Economic Modelling. 2021;102

LinkOut - more resources

Full Text Sources

Miscellaneous