Best practices for portfolio optimization by quantum computing, experimented on real quantum devices

- PMID: 37940680

- PMCID: PMC10632408

- DOI: 10.1038/s41598-023-45392-w

Best practices for portfolio optimization by quantum computing, experimented on real quantum devices

Abstract

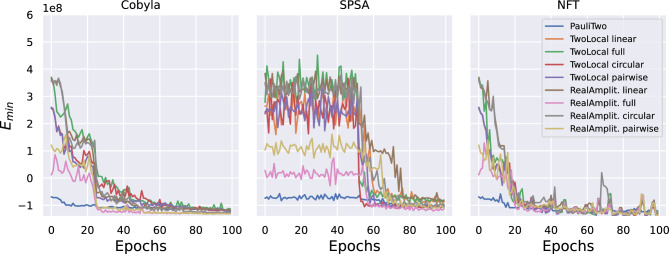

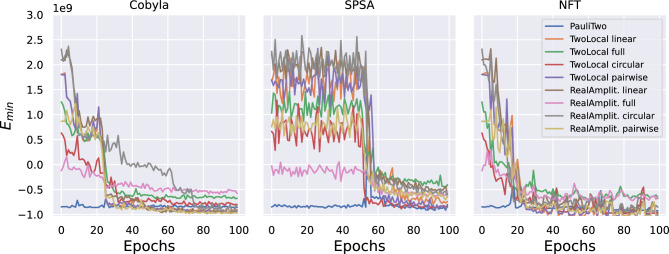

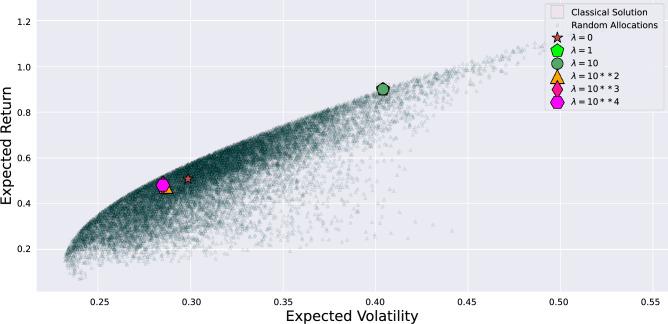

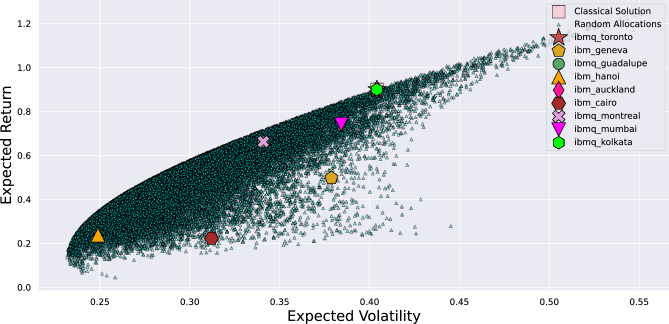

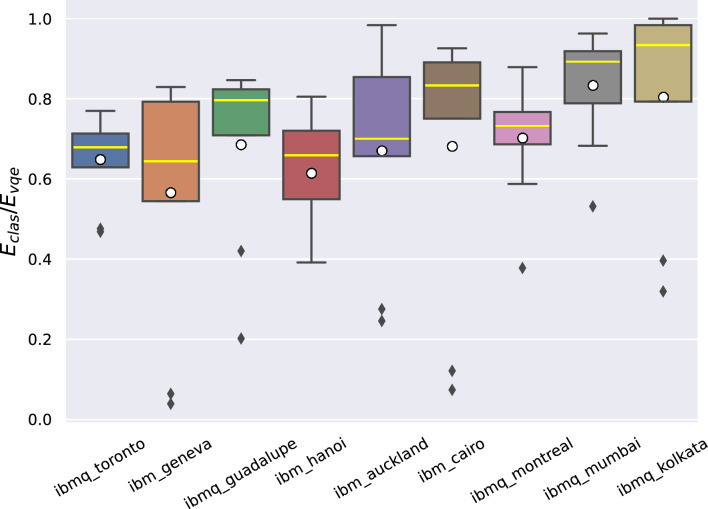

In finance, portfolio optimization aims at finding optimal investments maximizing a trade-off between return and risks, given some constraints. Classical formulations of this quadratic optimization problem have exact or heuristic solutions, but the complexity scales up as the market dimension increases. Recently, researchers are evaluating the possibility of facing the complexity scaling issue by employing quantum computing. In this paper, the problem is solved using the Variational Quantum Eigensolver (VQE), which in principle is very efficient. The main outcome of this work consists of the definition of the best hyperparameters to set, in order to perform Portfolio Optimization by VQE on real quantum computers. In particular, a quite general formulation of the constrained quadratic problem is considered, which is translated into Quadratic Unconstrained Binary Optimization by the binary encoding of variables and by including constraints in the objective function. This is converted into a set of quantum operators (Ising Hamiltonian), whose minimum eigenvalue is found by VQE and corresponds to the optimal solution. In this work, different hyperparameters of the procedure are analyzed, including different ansatzes and optimization methods by means of experiments on both simulators and real quantum computers. Experiments show that there is a strong dependence of solutions quality on the sufficiently sized quantum computer and correct hyperparameters, and with the best choices, the quantum algorithm run on real quantum devices reaches solutions very close to the exact one, with a strong convergence rate towards the classical solution, even without error-mitigation techniques. Moreover, results obtained on different real quantum devices, for a small-sized example, show the relation between the quality of the solution and the dimension of the quantum processor. Evidences allow concluding which are the best ways to solve real Portfolio Optimization problems by VQE on quantum devices, and confirm the possibility to solve them with higher efficiency, with respect to existing methods, as soon as the size of quantum hardware will be sufficiently high.

© 2023. The Author(s).

Conflict of interest statement

The authors declare no competing interests.

Figures

References

-

- Markowitz H. Portfolio selection. J. Financ. 1952;7:77–91.

-

- Marinescu R, Dechter R. And/or Branch-and-Bound Search for Pure 0/1 Integer Linear Programming Problems. In: Beck JC, Smith BM, editors. Integration of AI and OR Techniques in Constraint Programming for Combinatorial Optimization Problems. Springer; 2006. pp. 152–166.

-

- Niu S-F, Wang G-X, Sun X-L. A branch-and-bound algorithm for discrete multi-factor portfolio optimization model. J. Shanghai Univ. 2008;12:26–30. doi: 10.1007/s11741-008-0105-3. - DOI

-

- Pinelis M, Ruppert D. Machine learning portfolio allocation. J. Financ. Data Sci. 2022;8:35–54. doi: 10.1016/j.jfds.2021.12.001. - DOI

-

- Gunjan A, Bhattacharyya S. A brief review of portfolio optimization techniques. Artif. Intell. Rev. 2022 doi: 10.1007/s10462-022-10273-7. - DOI

LinkOut - more resources

Full Text Sources