Scaling Exponents of Time Series Data: A Machine Learning Approach

- PMID: 38136551

- PMCID: PMC10742462

- DOI: 10.3390/e25121671

Scaling Exponents of Time Series Data: A Machine Learning Approach

Abstract

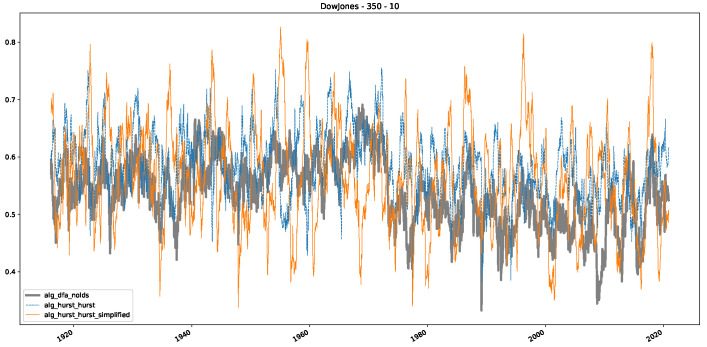

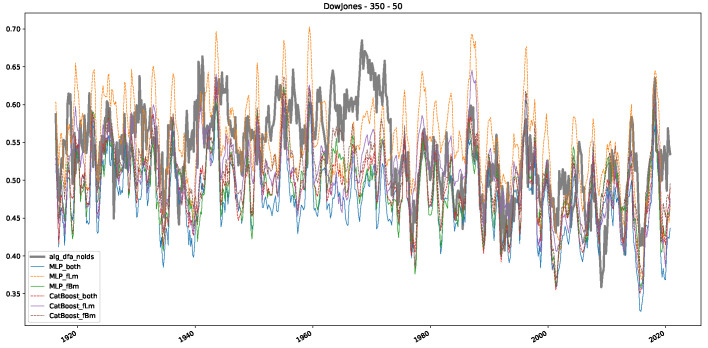

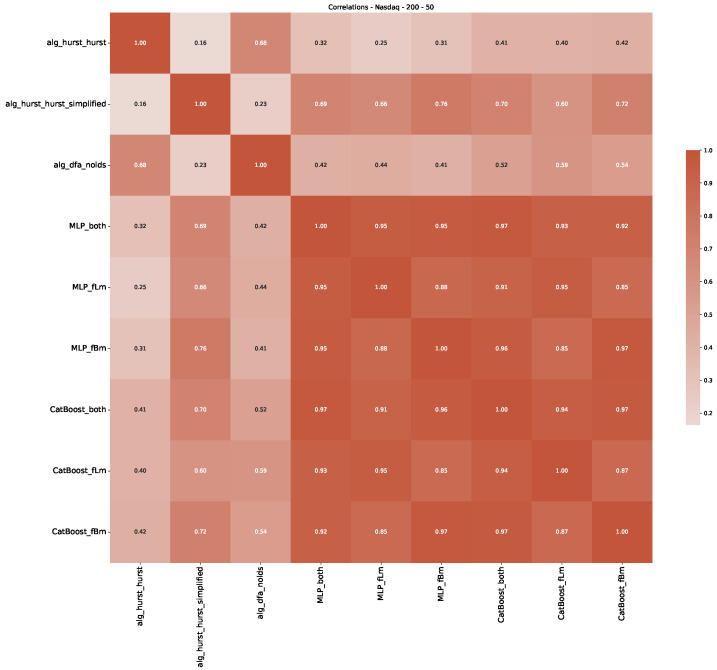

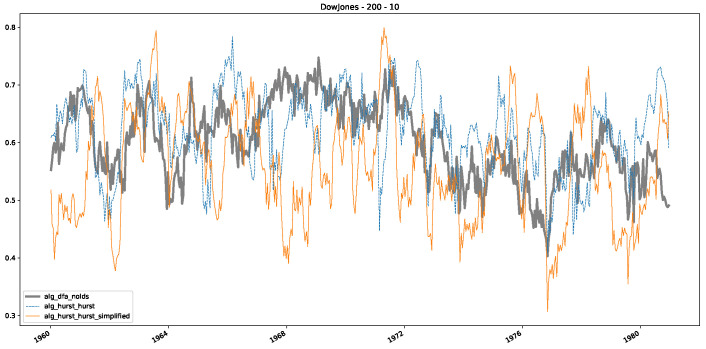

In this study, we present a novel approach to estimating the Hurst exponent of time series data using a variety of machine learning algorithms. The Hurst exponent is a crucial parameter in characterizing long-range dependence in time series, and traditional methods such as Rescaled Range (R/S) analysis and Detrended Fluctuation Analysis (DFA) have been widely used for its estimation. However, these methods have certain limitations, which we sought to address by modifying the R/S approach to distinguish between fractional Lévy and fractional Brownian motion, and by demonstrating the inadequacy of DFA and similar methods for data that resembles fractional Lévy motion. This inspired us to utilize machine learning techniques to improve the estimation process. In an unprecedented step, we train various machine learning models, including LightGBM, MLP, and AdaBoost, on synthetic data generated from random walks, namely fractional Brownian motion and fractional Lévy motion, where the ground truth Hurst exponent is known. This means that we can initialize and create these stochastic processes with a scaling Hurst/scaling exponent, which is then used as the ground truth for training. Furthermore, we perform the continuous estimation of the scaling exponent directly from the time series, without resorting to the calculation of the power spectrum or other sophisticated preprocessing steps, as done in past approaches. Our experiments reveal that the machine learning-based estimators outperform traditional R/S analysis and DFA methods in estimating the Hurst exponent, particularly for data akin to fractional Lévy motion. Validating our approach on real-world financial data, we observe a divergence between the estimated Hurst/scaling exponents and results reported in the literature. Nevertheless, the confirmation provided by known ground truths reinforces the superiority of our approach in terms of accuracy. This work highlights the potential of machine learning algorithms for accurately estimating the Hurst exponent, paving new paths for time series analysis. By marrying traditional finance methods with the capabilities of machine learning, our study provides a novel contribution towards the future of time series data analysis.

Keywords: Hurst exponent; artificial intelligence; complexity; machine learning; regression analysis; scaling exponent.

Conflict of interest statement

The authors declare no conflict of interest.

Figures

References

-

- Mandelbrot B.B., Wallis J.R. Robustness of the rescaled range R/S in the measurement of noncyclic long run statistical dependence. Water Resour. Res. 1969;5:967–988. doi: 10.1029/WR005i005p00967. - DOI

-

- Peters E.E. Fractal Market Analysis: Applying Chaos Theory to Investment and Economics. J. Wiley & Sons; New York, NY, USA: 1994. Wiley Finance Editions.

-

- Turcotte D.L. Fractals and Chaos in Geology and Geophysics. 2nd ed. Cambridge University Press; Cambridge, UK: 1997. - DOI

-

- Hurst H., Black R., Sinaika Y. Long-Term Storage in Reservoirs: An Experimental Study. Constable; London, UK: 1965.

LinkOut - more resources

Full Text Sources

Miscellaneous