Which popular predictor is more useful to forecast international stock markets during the coronavirus pandemic: VIX vs EPU?

- PMID: 38620312

- PMCID: PMC7521353

- DOI: 10.1016/j.irfa.2020.101596

Which popular predictor is more useful to forecast international stock markets during the coronavirus pandemic: VIX vs EPU?

Abstract

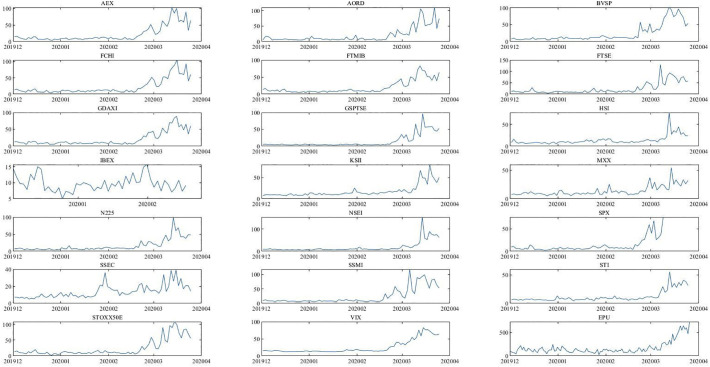

This study mainly investigates which predictors (VIX or EPU index) are useful to forecast future volatility for 19 equity indices based on HAR framework during coronavirus pandemic. Out-of-sample analysis shows that the HAR-RV-VIX model exhibits superior forecasting performance for 12 stock markets, while EPU index just can improve forecast accuracy for 5 equity indices, implying that VIX index is more useful for most stock markets' future volatility during coronavirus crisis. The results are robust in recursive window method, alternative realized measures and sub-sample analysis; moreover, VIX index still contains the strongest predictive ability by considering kitchen sink model and mean combination forecast. Furthermore, we further discuss the predictive effect of VIX and EPU index before the coronavirus crisis. Our article provides policy makers, researchers and investors with new insights into exploiting the predictive ability of VIX and EPU index for international stock markets during coronavirus pandemic.

Keywords: COVID-19; EPU; HAR framework; International stock market; VIX.

© 2020 Elsevier Inc. All rights reserved.

Conflict of interest statement

The authors declare that they have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

Similar articles

-

Have the predictability of oil changed during the COVID-19 pandemic: Evidence from international stock markets.Int Rev Financ Anal. 2023 May;87:102620. doi: 10.1016/j.irfa.2023.102620. Epub 2023 Mar 15. Int Rev Financ Anal. 2023. PMID: 36942110 Free PMC article.

-

Jumps and stock market variance during the COVID-19 pandemic: Evidence from international stock markets.Financ Res Lett. 2022 Aug;48:102896. doi: 10.1016/j.frl.2022.102896. Epub 2022 Apr 21. Financ Res Lett. 2022. PMID: 35469270 Free PMC article.

-

The role of the IDEMV in predicting European stock market volatility during the COVID-19 pandemic.Financ Res Lett. 2020 Oct;36:101749. doi: 10.1016/j.frl.2020.101749. Epub 2020 Sep 3. Financ Res Lett. 2020. PMID: 32908465 Free PMC article.

-

Time-frequency domain analysis of investor fear and expectations in stock markets of BRIC economies.Heliyon. 2021 Oct 19;7(10):e08211. doi: 10.1016/j.heliyon.2021.e08211. eCollection 2021 Oct. Heliyon. 2021. PMID: 34754971 Free PMC article. Review.

-

Relationship between uncertainty in the oil and stock markets before and after the shale gas revolution: Evidence from the OVX, VIX, and VKOSPI volatility indices.PLoS One. 2020 May 5;15(5):e0232508. doi: 10.1371/journal.pone.0232508. eCollection 2020. PLoS One. 2020. PMID: 32369536 Free PMC article. Review.

Cited by

-

Assessing systemic risk in financial markets using dynamic topic networks.Sci Rep. 2022 Feb 17;12(1):2668. doi: 10.1038/s41598-022-06399-x. Sci Rep. 2022. PMID: 35177679 Free PMC article.

-

Emerging stock market volatility and economic fundamentals: the importance of US uncertainty spillovers, financial and health crises.Ann Oper Res. 2022;313(2):1077-1116. doi: 10.1007/s10479-021-04042-y. Epub 2021 Apr 21. Ann Oper Res. 2022. PMID: 33903782 Free PMC article.

-

Epidemics, Public Sentiment, and Infectious Disease Equity Market Volatility.Front Public Health. 2021 May 14;9:686870. doi: 10.3389/fpubh.2021.686870. eCollection 2021. Front Public Health. 2021. PMID: 34055733 Free PMC article.

-

Frequency spillovers between green bonds, global factors and stock market before and during COVID-19 crisis.Econ Anal Policy. 2023 Mar;77:558-580. doi: 10.1016/j.eap.2022.12.010. Epub 2022 Dec 19. Econ Anal Policy. 2023. PMID: 36570097 Free PMC article.

-

Determinants of Tourism Stocks During the COVID-19: Evidence From the Deep Learning Models.Front Public Health. 2021 Apr 9;9:675801. doi: 10.3389/fpubh.2021.675801. eCollection 2021. Front Public Health. 2021. PMID: 33898386 Free PMC article.

References

-

- Aganin A. Forecast comparison of volatility models on Russian stock market. Applied Econometrics. 2017;48:63–84.

-

- Andersen T.G., Bollerslev T. Answering the skeptics: Yes, standard volatility models do provide accurate forecasts. International Economic Review. 1998;39(4):885–905.

-

- Baker S., Bloom N., Davis S.J., Kost K., Sammon M., Viratyosin T. The unprecedented stock market reaction to COVID-19. Covid Economics: Vetted and Real-Time Papers. 2020;1(3)

-

- Baker S.R., Bloom N., Davis S.J. Measuring economic policy uncertainty. The Quarterly Journal of Economics. 2016;131(4):1593–1636.

-

- Balcilar M., Gupta R., Kim W.J., Kyei C. The role of economic policy uncertainties in predicting stock returns and their volatility for Hong Kong, Malaysia and South Korea. International Review of Economics and Finance. 2019;59:150–163.

LinkOut - more resources

Full Text Sources

Miscellaneous