International market exposure to sovereign ESG

- PMID: 39564478

- PMCID: PMC11575848

- DOI: 10.1080/20430795.2022.2148817

International market exposure to sovereign ESG

Abstract

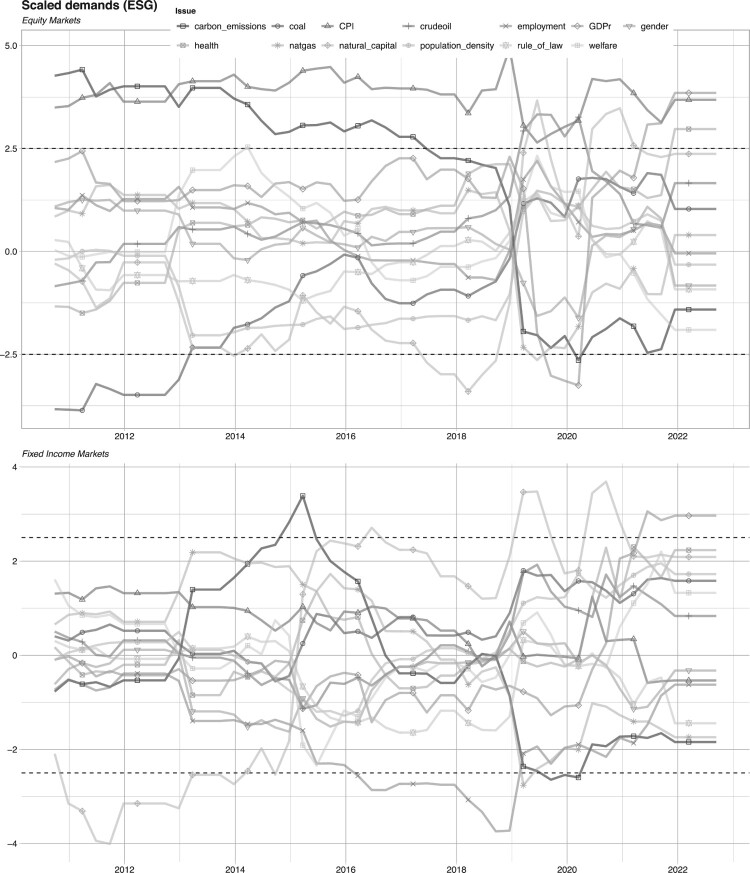

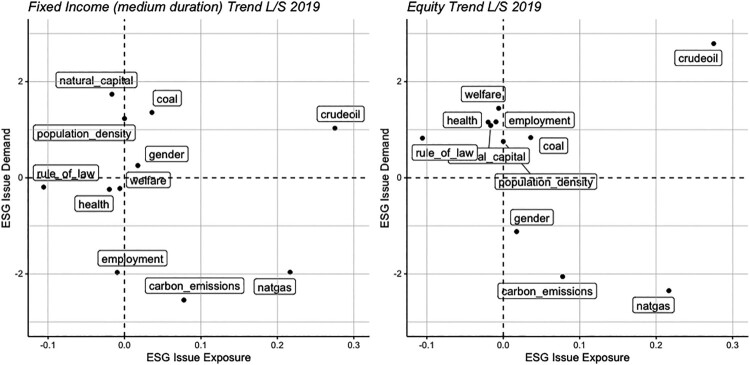

We quantify equity and bond market sensitivity to sovereign ESG scores and their variations which, theoretically, is equivalent to evaluating the demand for ESG at the global scale. We do so by estimating a longitudinal model, at the issue level, that captures exposures to sovereign ESG factors for both equity and fixed income indices. In spite of the surging interest in ESG investing, our results do not support a strong impact of ESG factors on the returns of international markets, implying that the demand for ESG at the country level is not a significant driver of prices. Nevertheless, we document a strong association between GDP growth and ESG scores at the country level.

Keywords: Factor demand; G11; H11; Q59; longitudinal models; sovereign ESG; sustainable investing.

© 2022 The Author(s). Published by Informa UK Limited, trading as Taylor & Francis Group.

Conflict of interest statement

No potential conflict of interest was reported by the author(s).

Figures

References

-

- Abhayawansa, S., and Tyagi S.. 2021. “Sustainable Investing: The Black Box of Environmental, Social, and Governance (ESG) Ratings.” Journal of Wealth Management 24 (1): 49–54.

-

- Angelova, D., Bosello F., Bigano A., and Giove S.. 2021. “Sovereign Rating Methodologies, ESG and Climate Change Risk: An Overview.” SSRN Working Paper 3841948.

-

- Avci, S. B., and Esen G.. 2021. “Country-Level Sustainability and Cross-Border Banking Flows.” SSRN Working Paper 3795642.

-

- Avramov, D., Cheng S., Lioui A., and Tarelli A.. 2022. “Sustainable Investing with ESG Rating Uncertainty.” Journal of Financial Economics 145 (2): 642–664.

-

- Balduzzi, P., and Moneta F.. 2017. “Economic Risk Premia in the Fixed-Income Markets: The Intraday Evidence.” Journal of Financial and Quantitative Analysis 52 (5): 1927–1950.

LinkOut - more resources

Full Text Sources