Exploring nonlinear chaotic systems with applications in stochastic processes

- PMID: 39715802

- PMCID: PMC11666588

- DOI: 10.1038/s41598-024-82057-8

Exploring nonlinear chaotic systems with applications in stochastic processes

Abstract

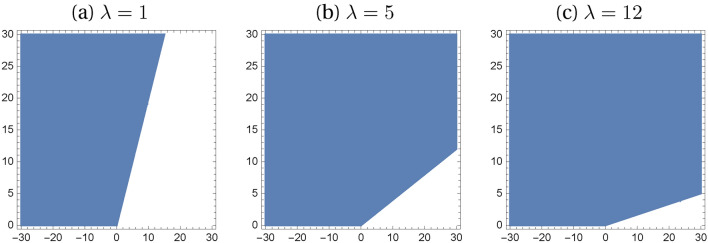

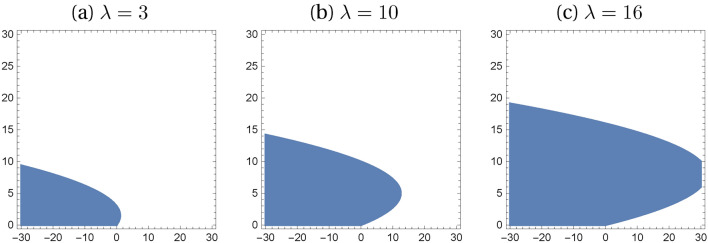

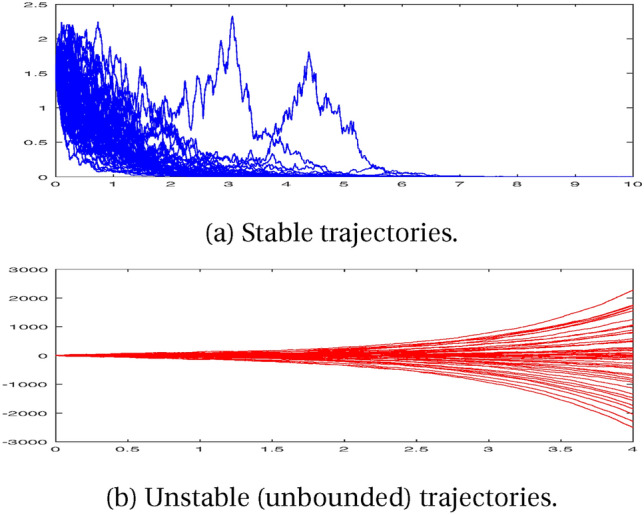

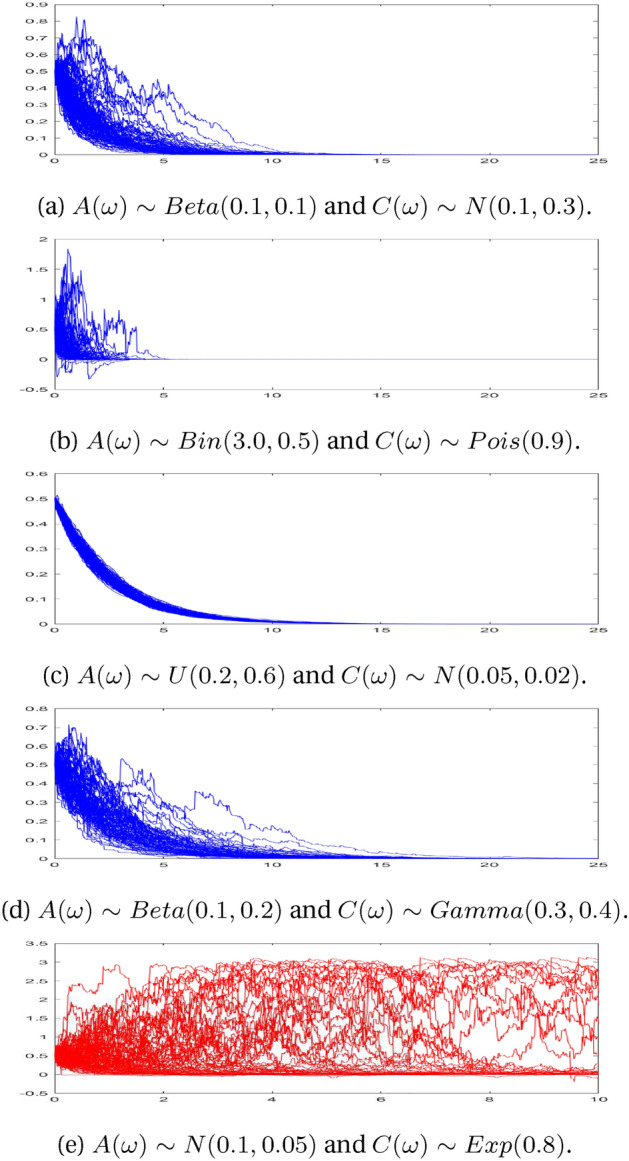

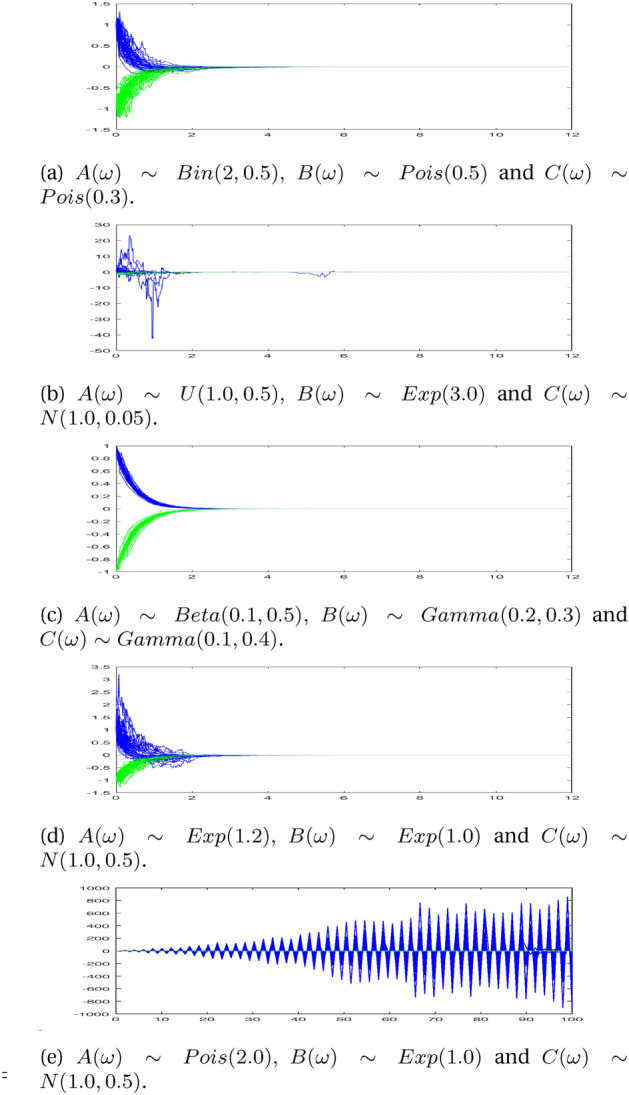

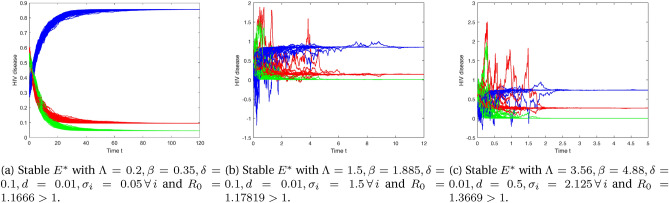

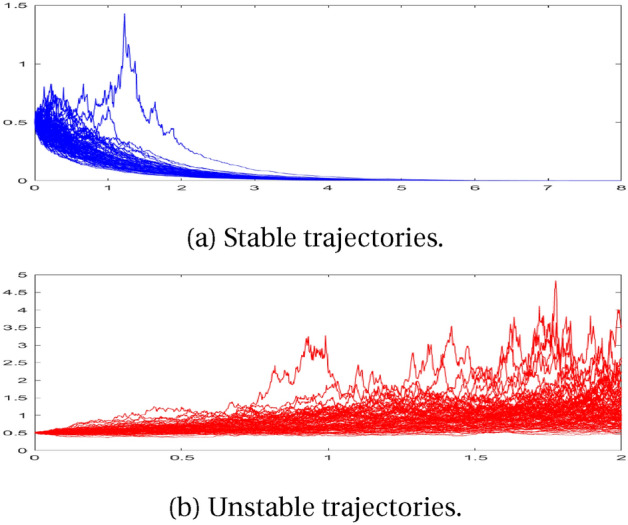

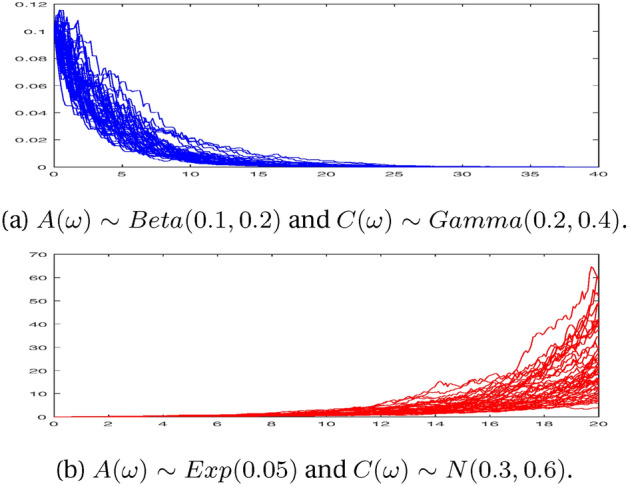

This manuscript explores the stability theory of several stochastic/random models. It delves into analyzing the stability of equilibrium states in systems influenced by standard Brownian motion and exhibit random variable coefficients. By constructing appropriate Lyapunov functions, various types of stability are identified, each associated with distinct stability conditions. The manuscript establishes the necessary criteria for asymptotic mean-square stability, stability in probability, and stochastic global exponential stability for the equilibrium points within these models. Building upon this comprehensive stability investigation, the manuscript delves into two distinct fields. Firstly, it examines the dynamics of HIV/AIDS disease persistence, particularly emphasizing the stochastic global exponential stability of the endemic equilibrium point denoted as [Formula: see text], where the underlying basic reproductive number is greater than one ([Formula: see text]). Secondly, the paper shifts its focus to finance, deriving sufficient conditions for both the stochastic market model and the random Ornstein-Uhlenbeck model. To enhance the validity of the theoretical findings, a series of numerical examples showcasing stability regions, alongside computer simulations that provide practical insights into the discussed concepts are provided.

Keywords: Financial market models; Global Mean-square stability (GMSS); HIV/AIDS stochastic model; Persistence; Stochastic and random systems.

© 2024. The Author(s).

Conflict of interest statement

Declarations. Competing interests: The authors declare no competing interests.

Figures

References

-

- Philip E Protter. Stochastic differential equations. Springer, 2005.

-

- Nsuami, Mozart U. & Witbooi, Peter J. Stochastic dynamics of an hiv/aids epidemic model with treatment. Quaestiones Mathematicae42(5), 605–621 (2019). - DOI

-

- Hans Föllmer & Alexander Schied. Stochastic finance: an introduction in discrete time. Walter de Gruyter, (2011).

-

- Eugene Wong & Bruce Hajek. Stochastic processes in engineering systems. Springer Science & Business Media, (2012).

-

- Soong, T. T. Random Differential Equations in Science and Engineering (Academic Press, New York, 1973).

LinkOut - more resources

Full Text Sources